Machine Learning By Andew Ng - Week 2

Multivariate Linear Regression

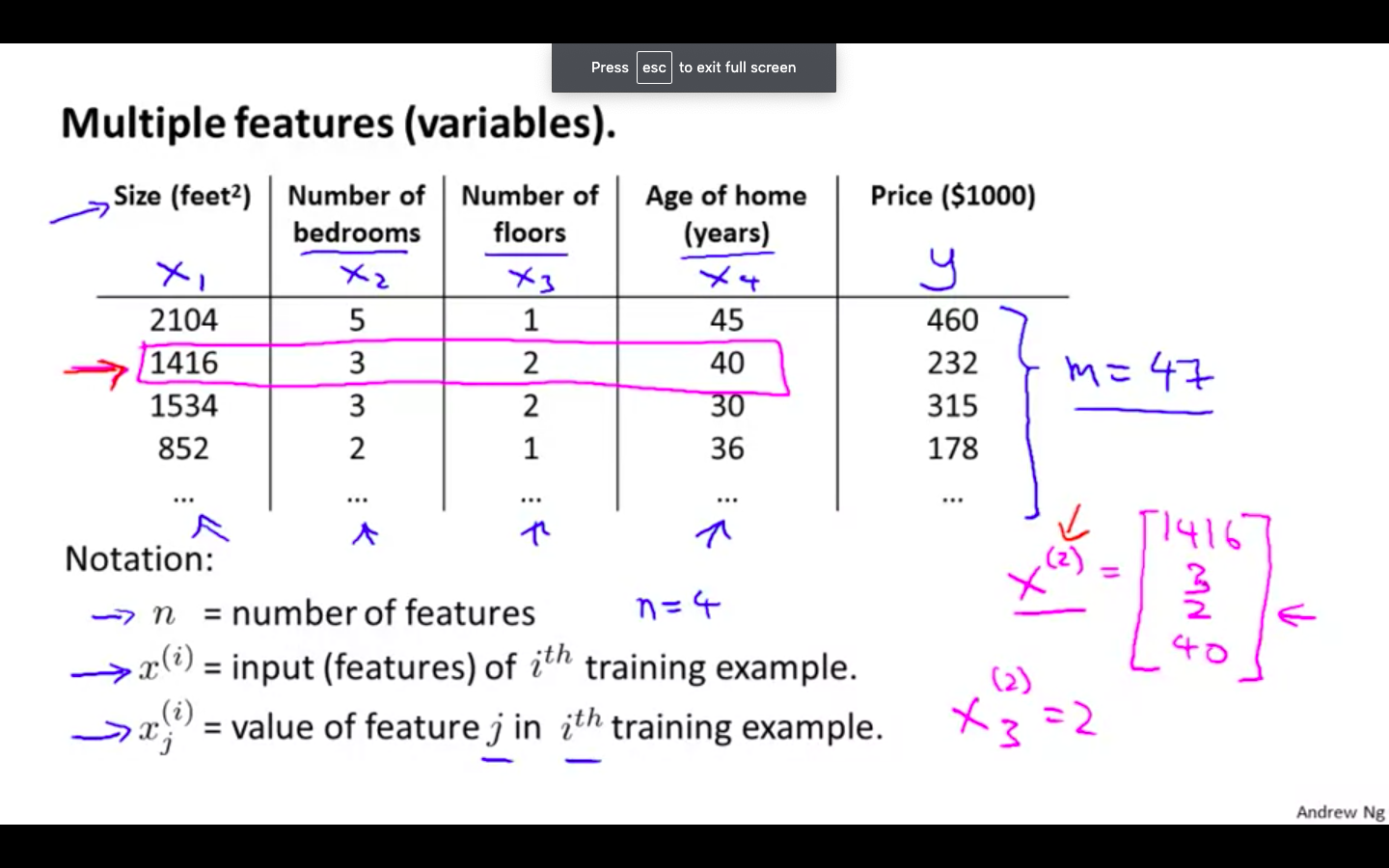

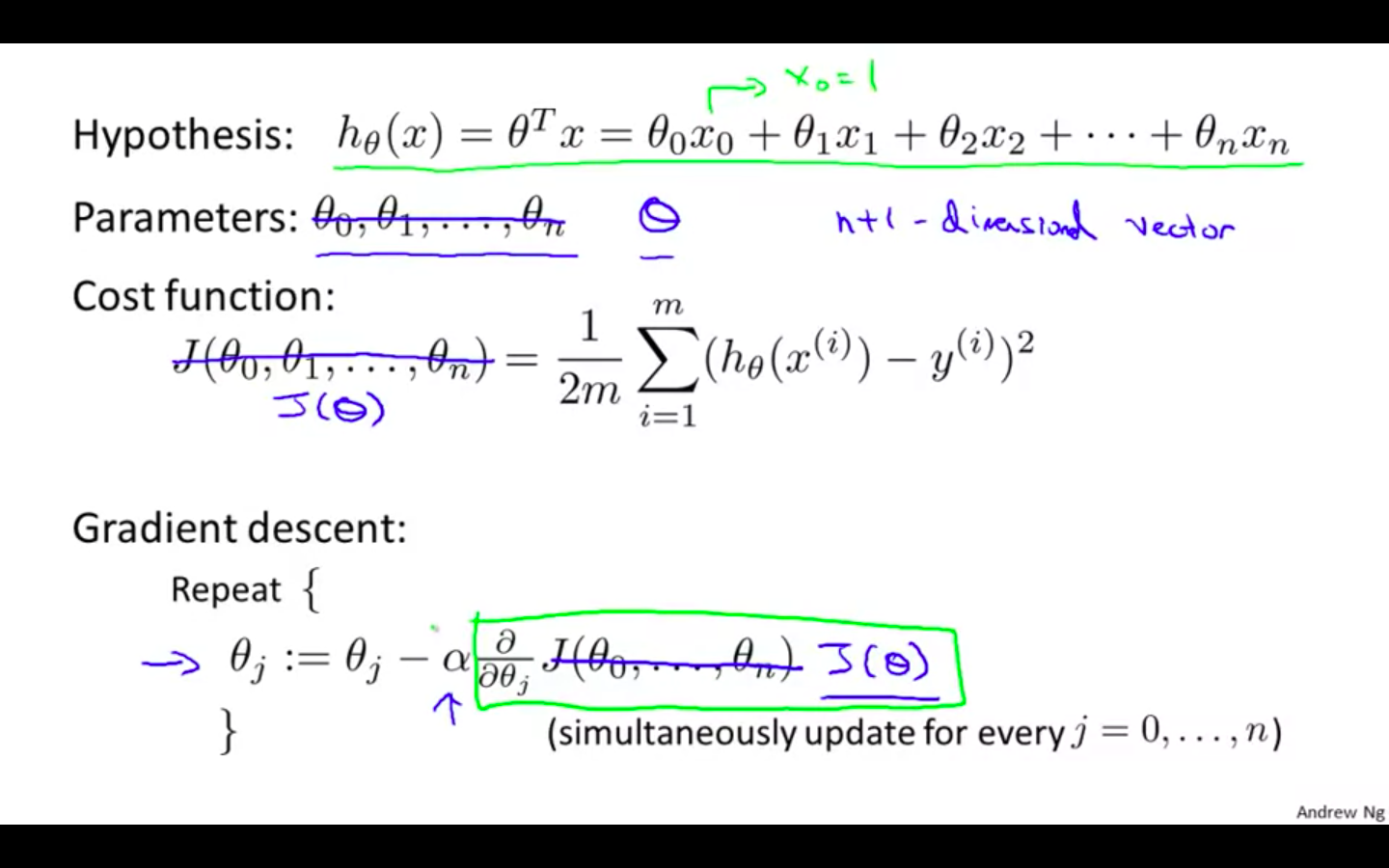

Multiple Features

-

Linear regression with multiple variables is also known as “multivariate linear regression”.

-

There can be ‘n’ number of features.

- For the example of predicting the price of a house, features can be no. of bedrooms, no. of floors, age of home, size.

-

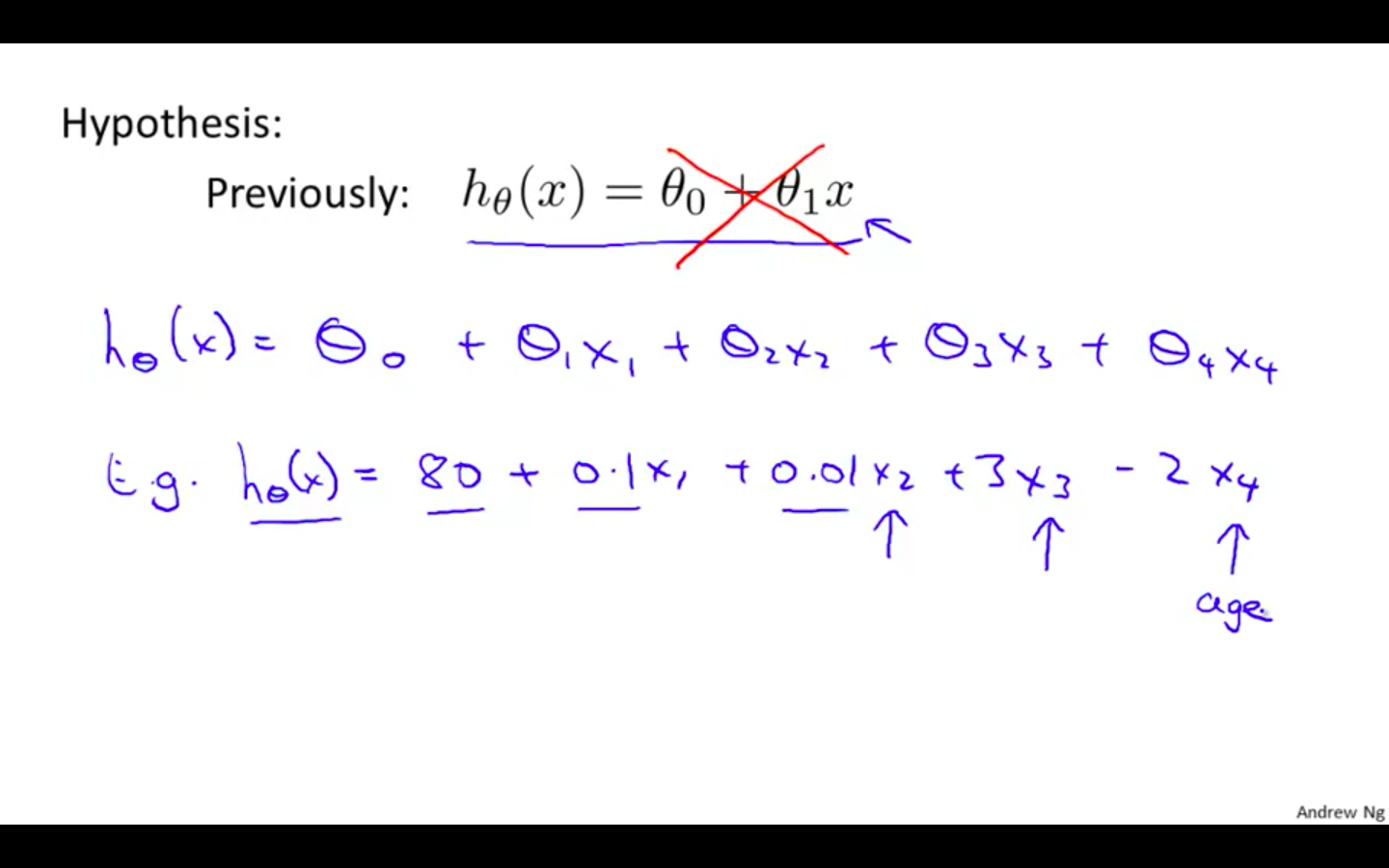

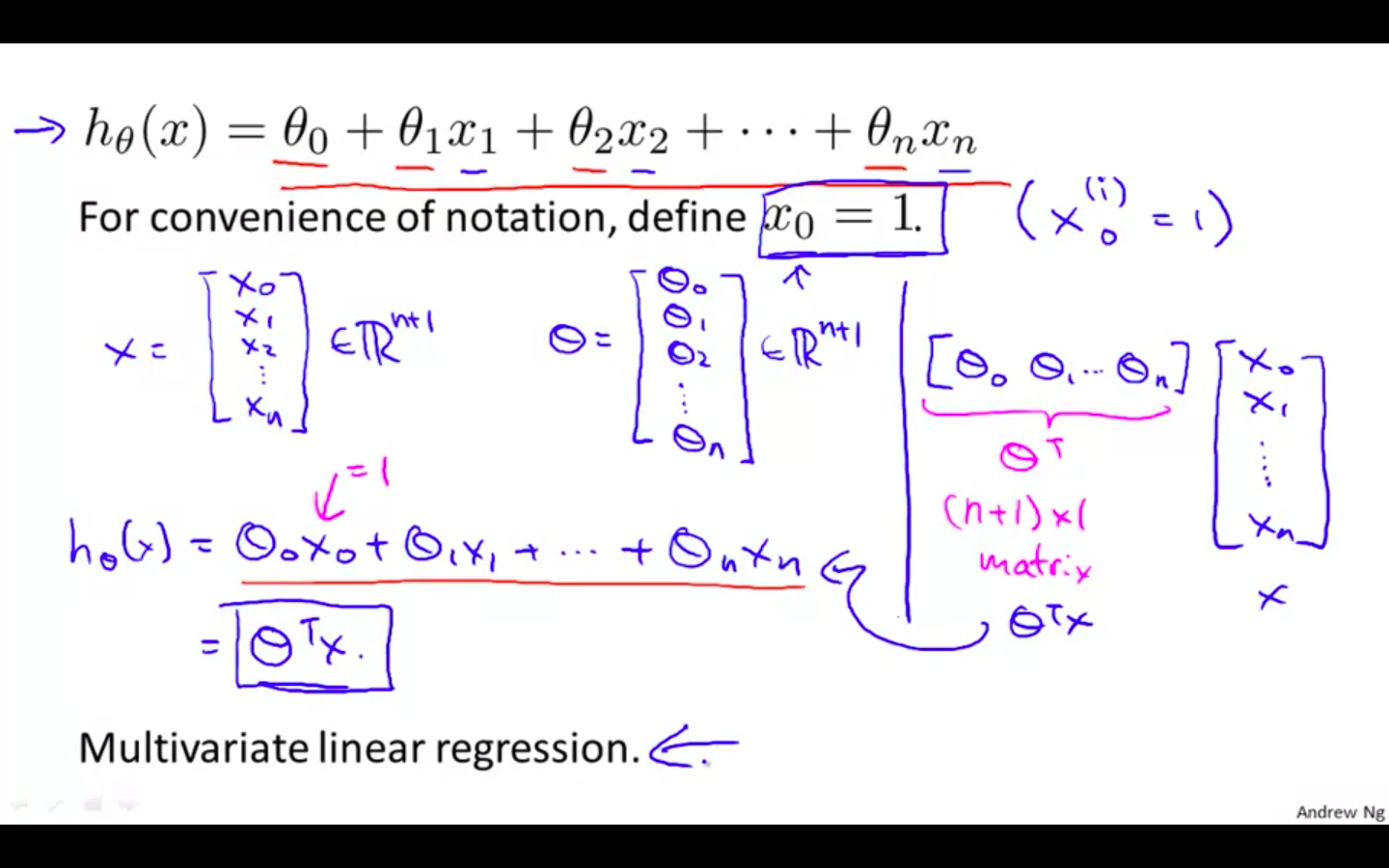

Hypothesis

- Number of parameters with their effect on the price of the house

-

Taking x-zero as 1 for the convenience of notation

-

This is called as the Multivariate Linear Regression.

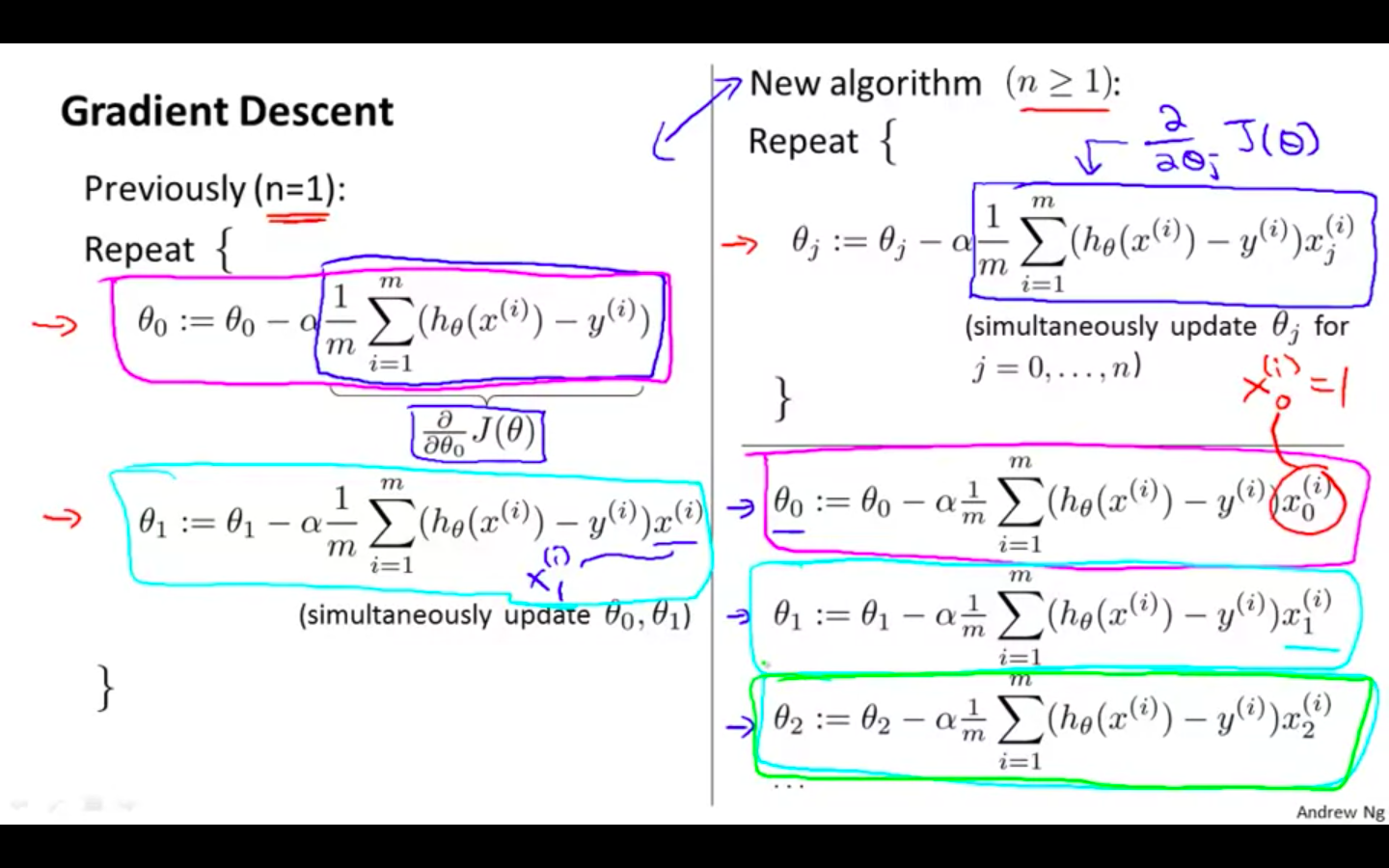

Gradient Descent for Multiple Variables

-

Concept

-

Comparison between Gradient Descent with one variable and Gradient Descent with multiple variable

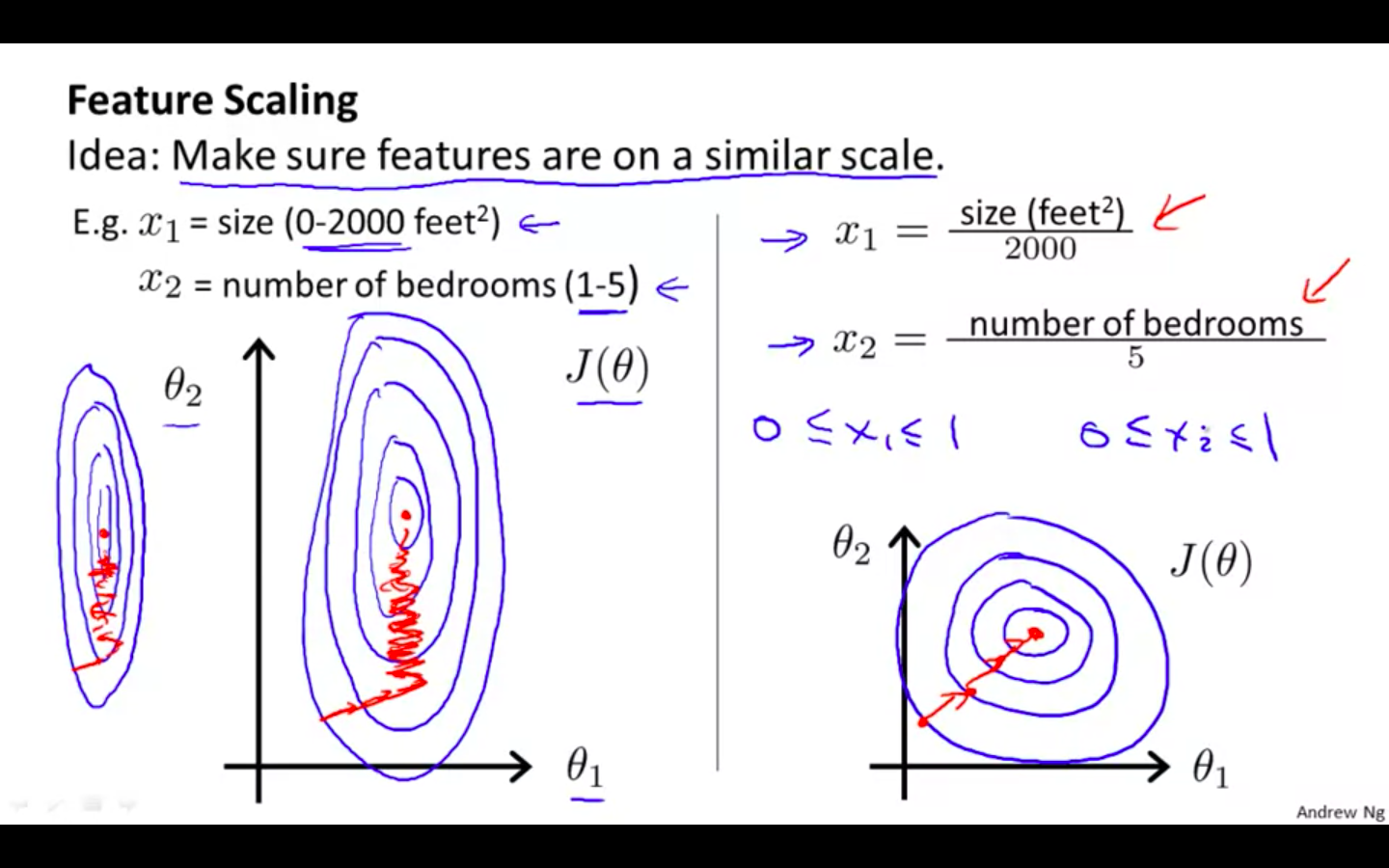

Gradient Descent In Practice I - Feature Scaling

-

Features Scaling

-

Idea: Make sure features are on a similar scale

-

This is because θ will descend quickly on small ranges and slowly on large ranges, and so will oscillate inefficiently down to the optimum when the variables are very uneven.

-

If they are not on a similar scalar then the contours will be very elliptical

- Gradient Descent will take more iteration to converge. i.e more time and power

-

If the features are on the similar scale, contours would be spaced and gradient descent would take less iteration to converge

-

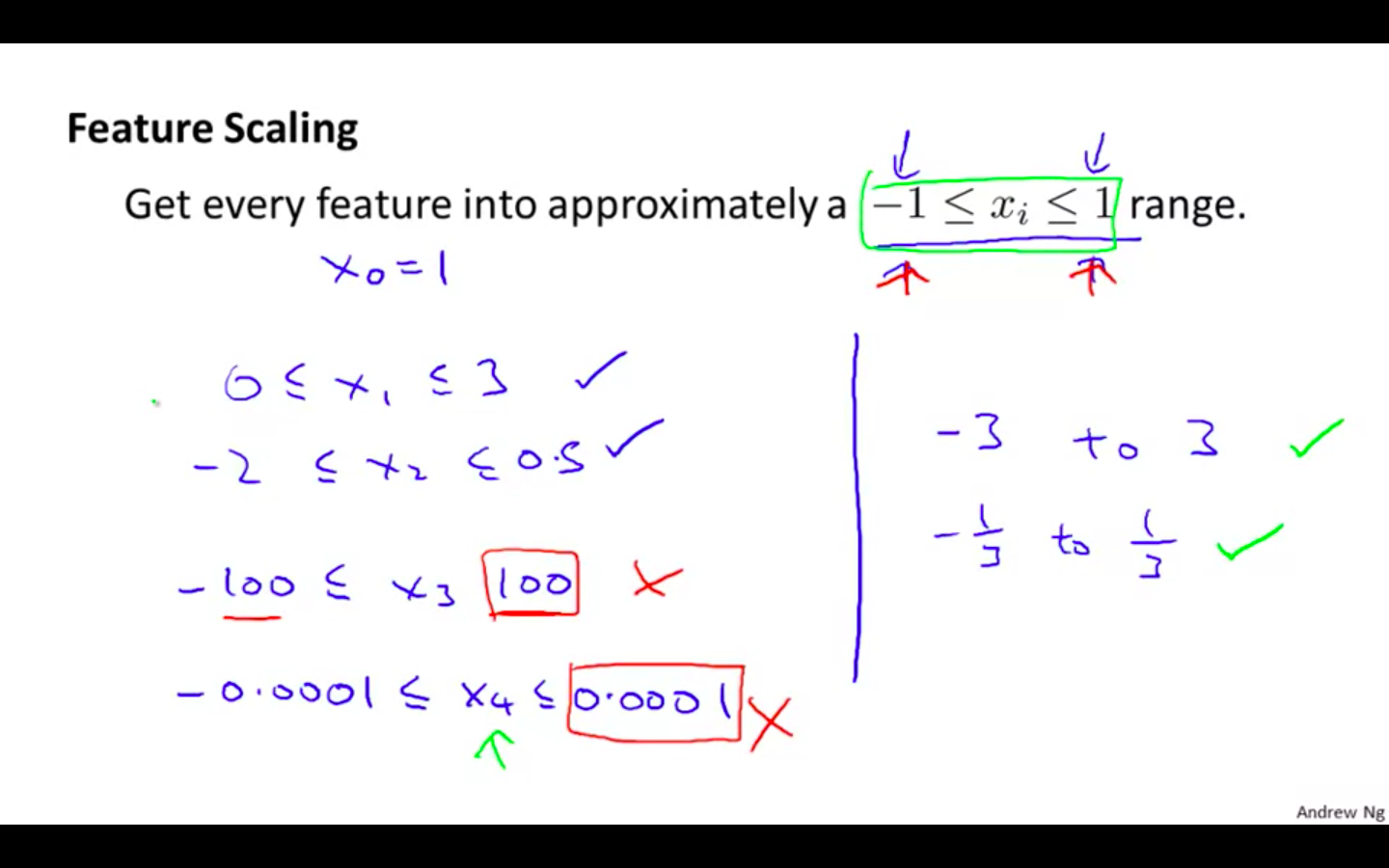

Feature should range between -1 ≤ x ≤ 1

-

+3, -3 = max

-

1/3, -1/3 = min

-

-

-

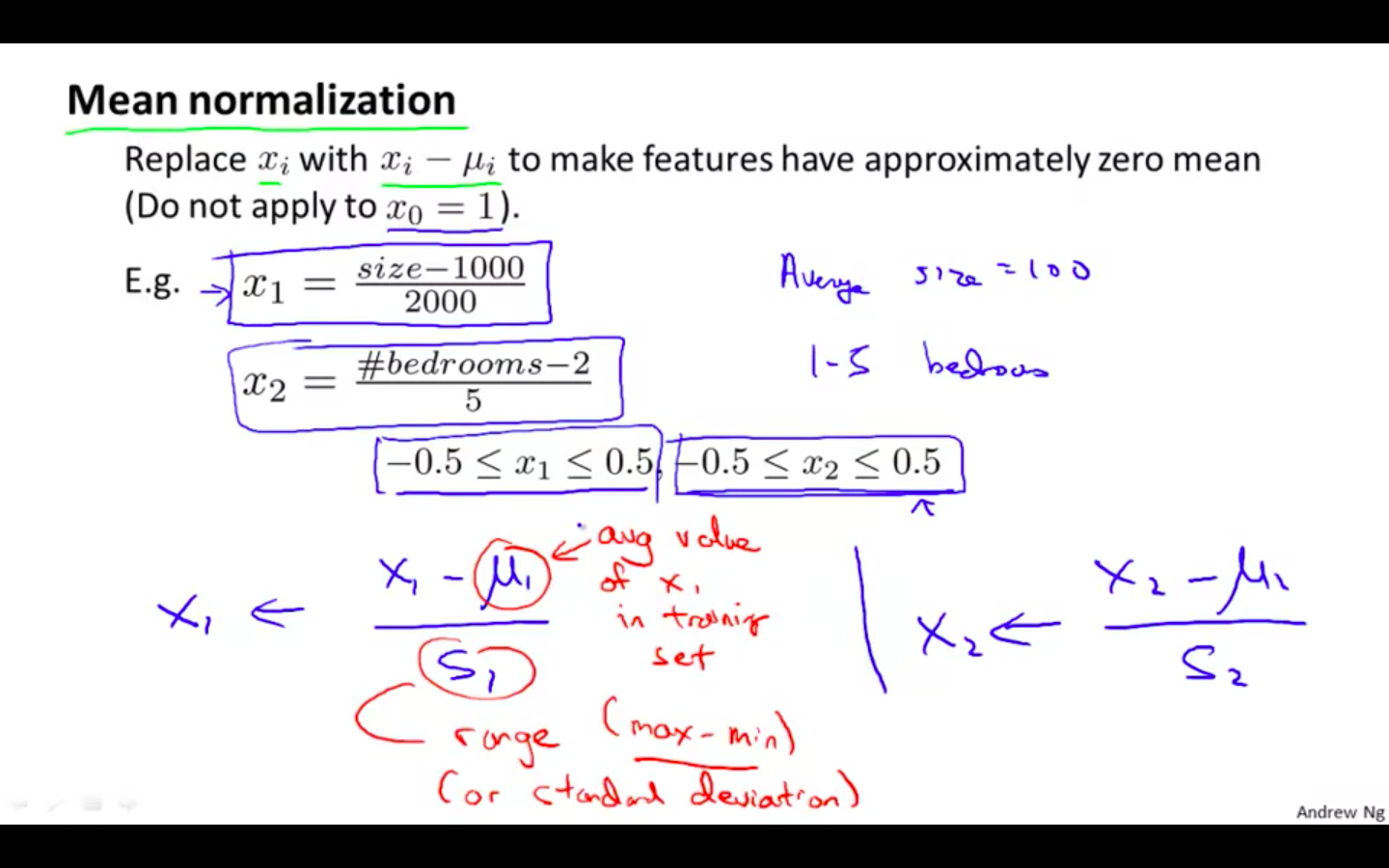

Mean Normalisation

-

Replace x with x - average value in the training set

-

Do not apply to x-zero = 1

-

This results in approximately zero mean.

-

x = x - average value on training set / s - range ( max - min )

-

Gradient Descent In Practice II - Learning Rate

-

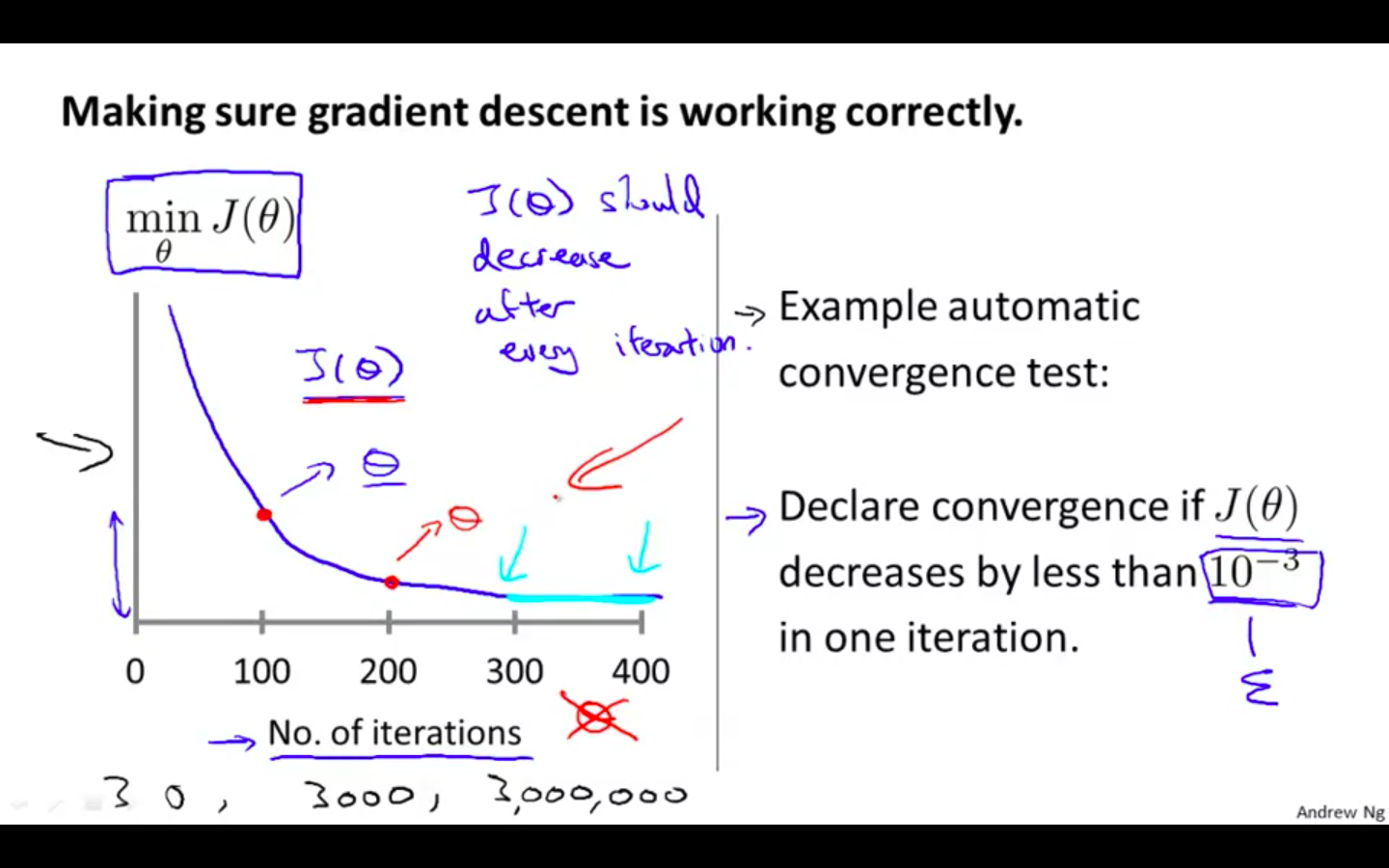

“Debugging”: How to make sure gradient descent is working correctly

-

Plot the graph, on x-axis is the iteration and on y-axis value of cost function

-

Automatic convergence test can be implemented

- Declare convergence if J(θ) decreases by less than E in one iteration, where E is some small value such as 10^-3

-

-

How to choose learning rate alpha

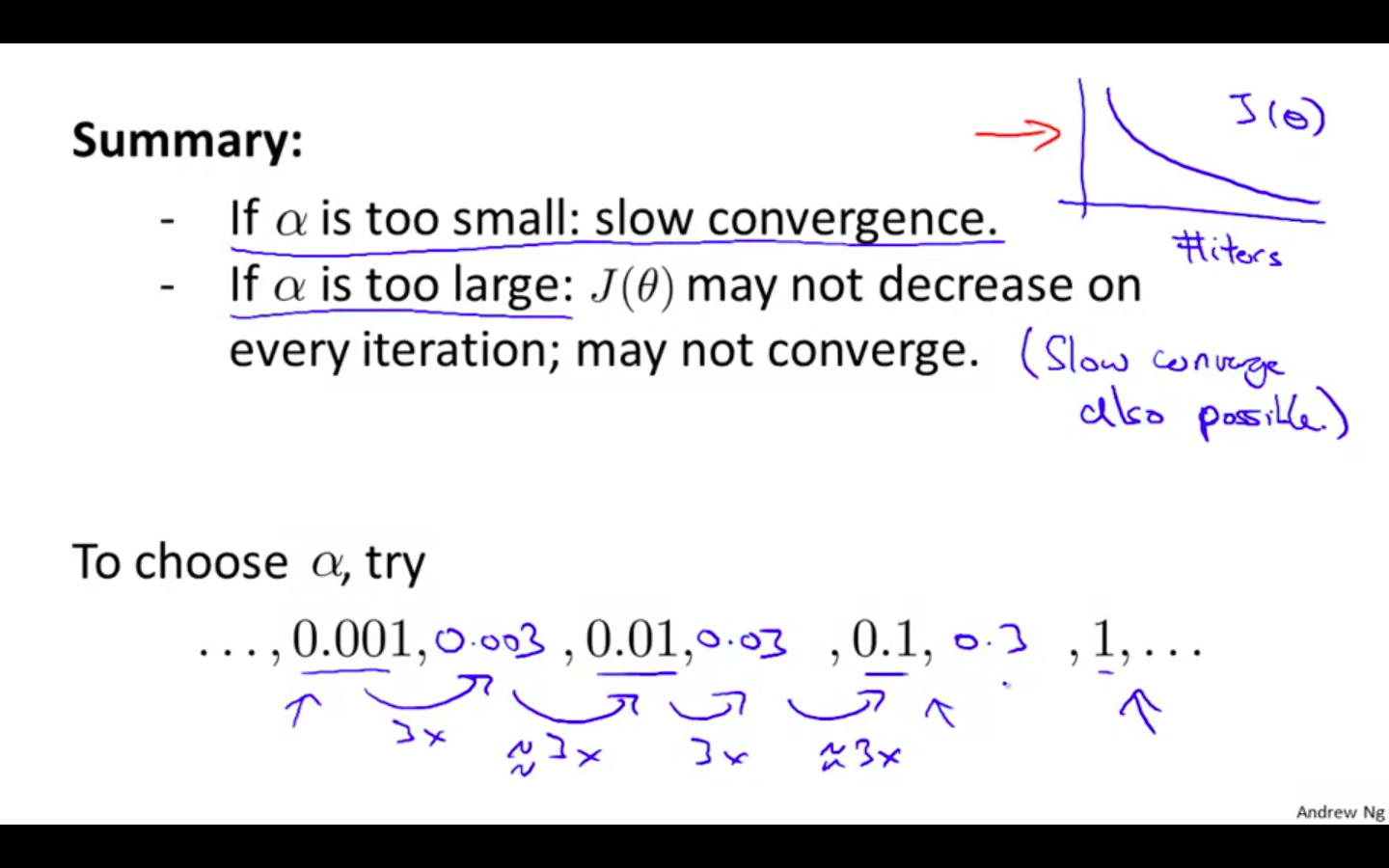

- It has been proven that if learning rate α is sufficiently small, then J(θ) will decrease on every iteration.

-

Summary

-

Try with some range of values

-

alpha is too small : slow convergence

-

alpha is too large : may not decrease on every iteration, may not even converge

-

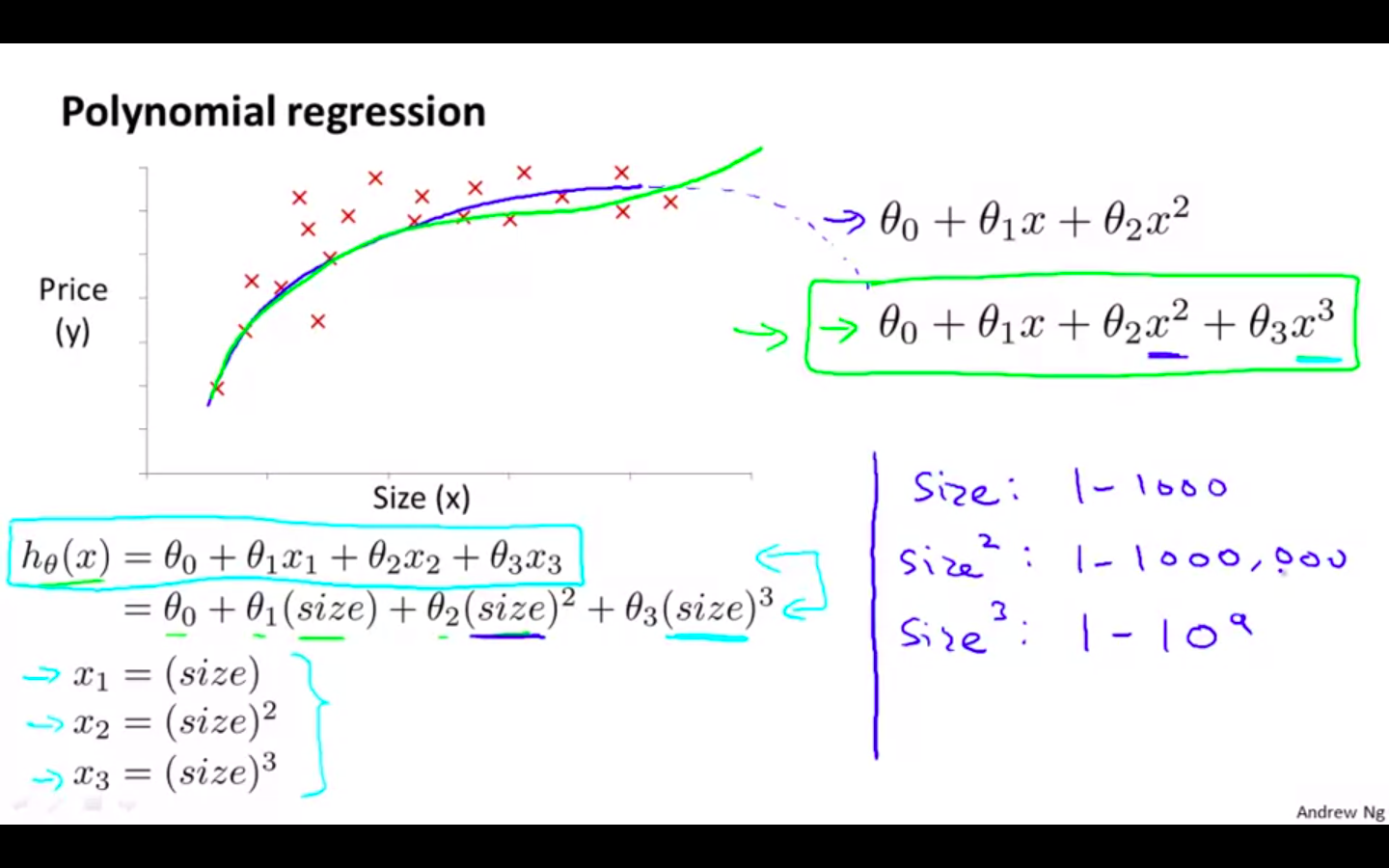

Features and Polynomial Regression

-

We can improve our features and the form of our hypothesis function in a couple different ways.

-

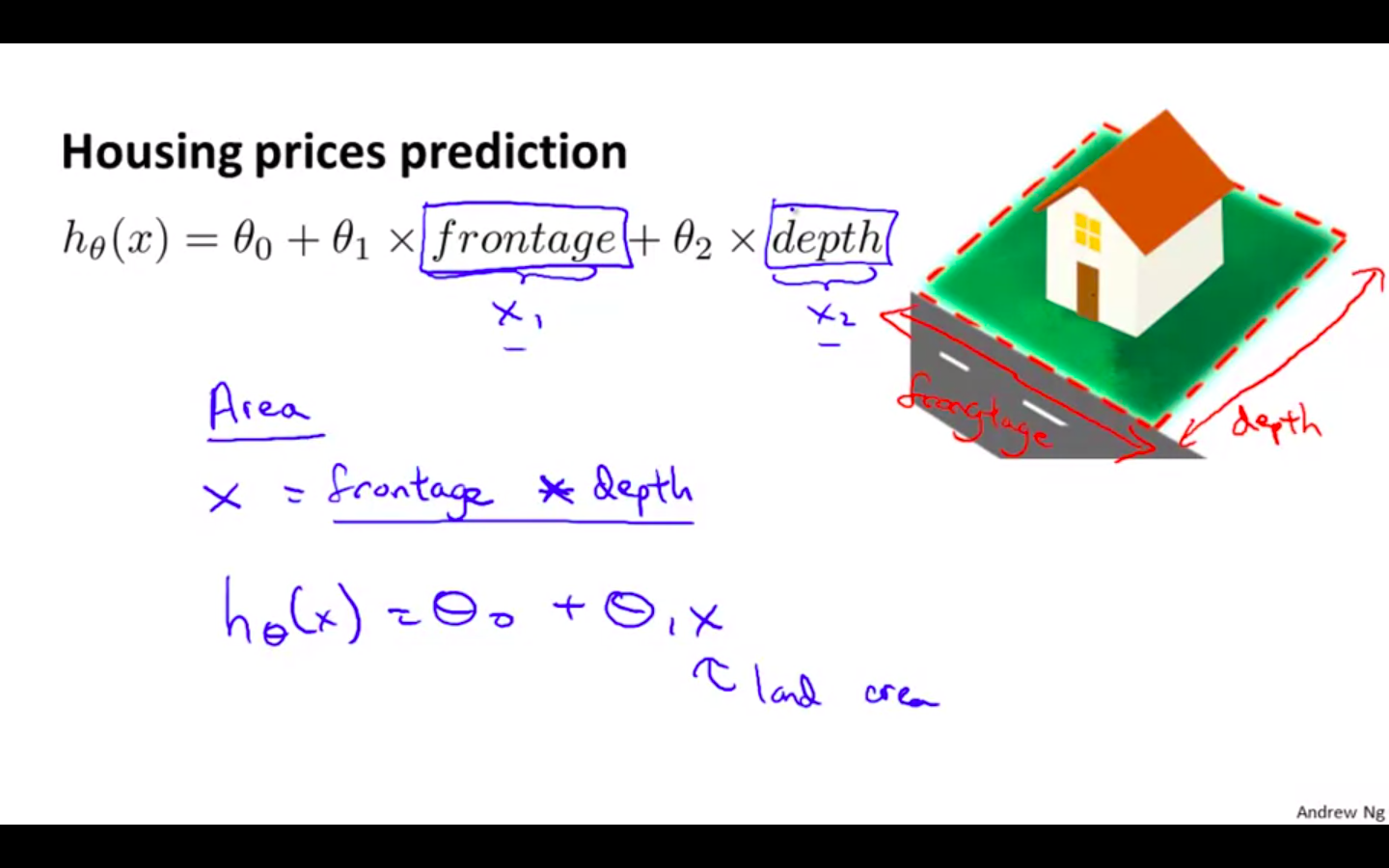

We can combine multiple features into one. For example, we can combine x-1 and x-2 into a new feature x-3 by taking x-1 * x-2.

-

Polynomial Regression

-

Our hypothesis function need not be linear (a straight line) if that does not fit the data well.

-

We can change the behaviour or curve of our hypothesis function by making it a quadratic, cubic or square root function (or any other form).

-

Quadratic function comes down eventually which is not applicable in this example. Prices can’t go down with increase in size of the house.

-

-

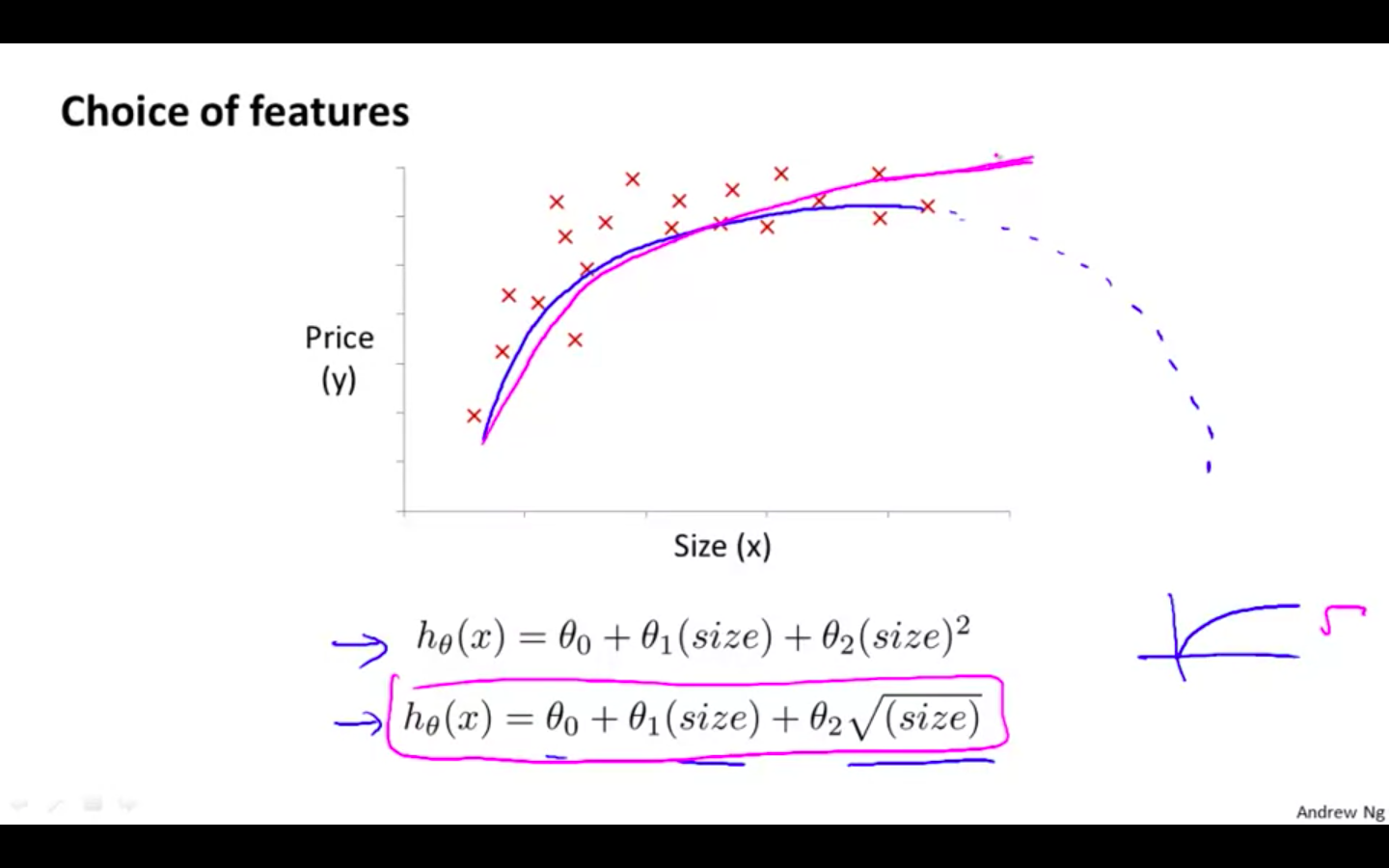

Choice Of Features

- One important thing to keep in mind is, if you choose your features this way then feature scaling becomes very important.

Computing Parameters Analytically

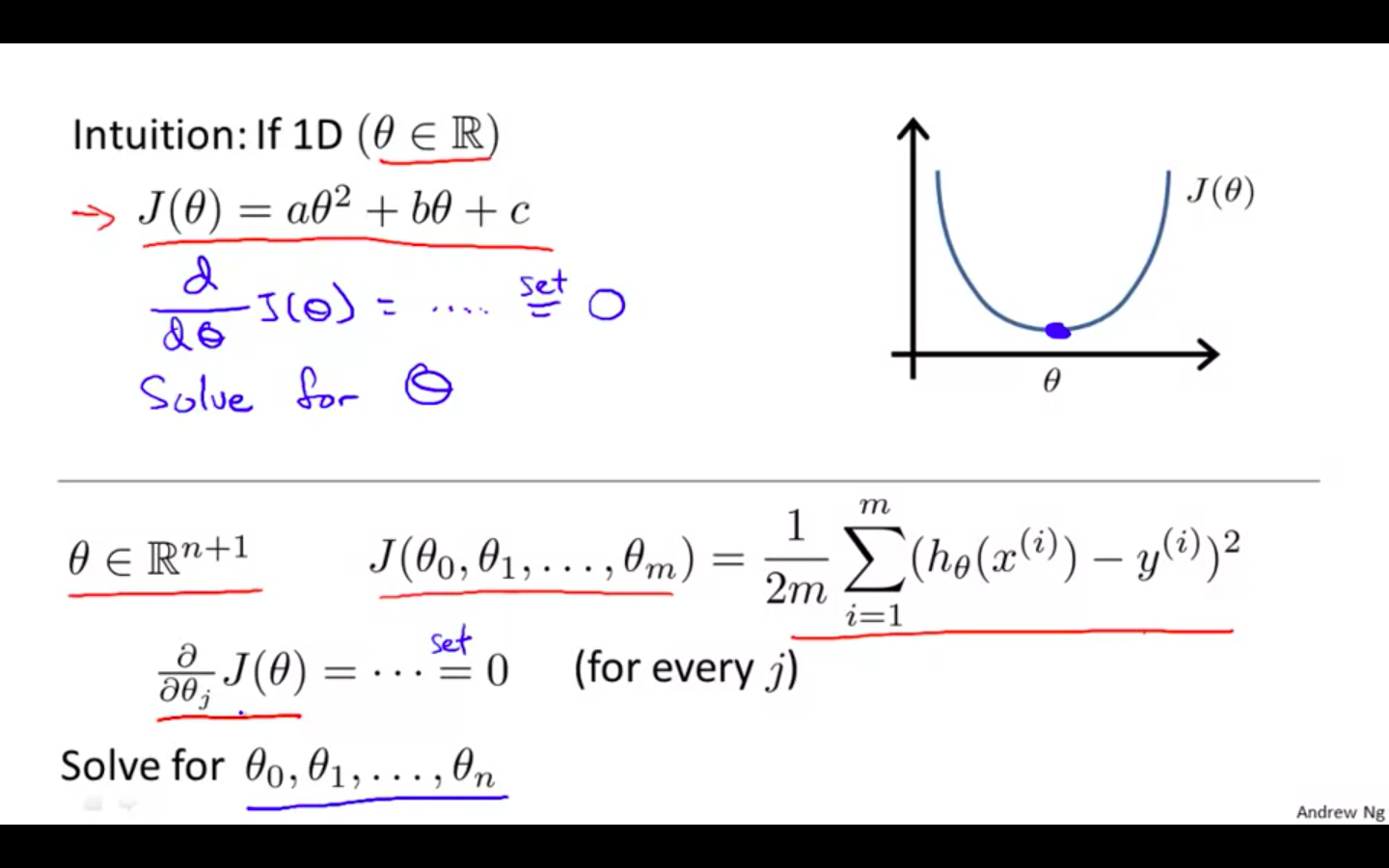

Normal Equation

-

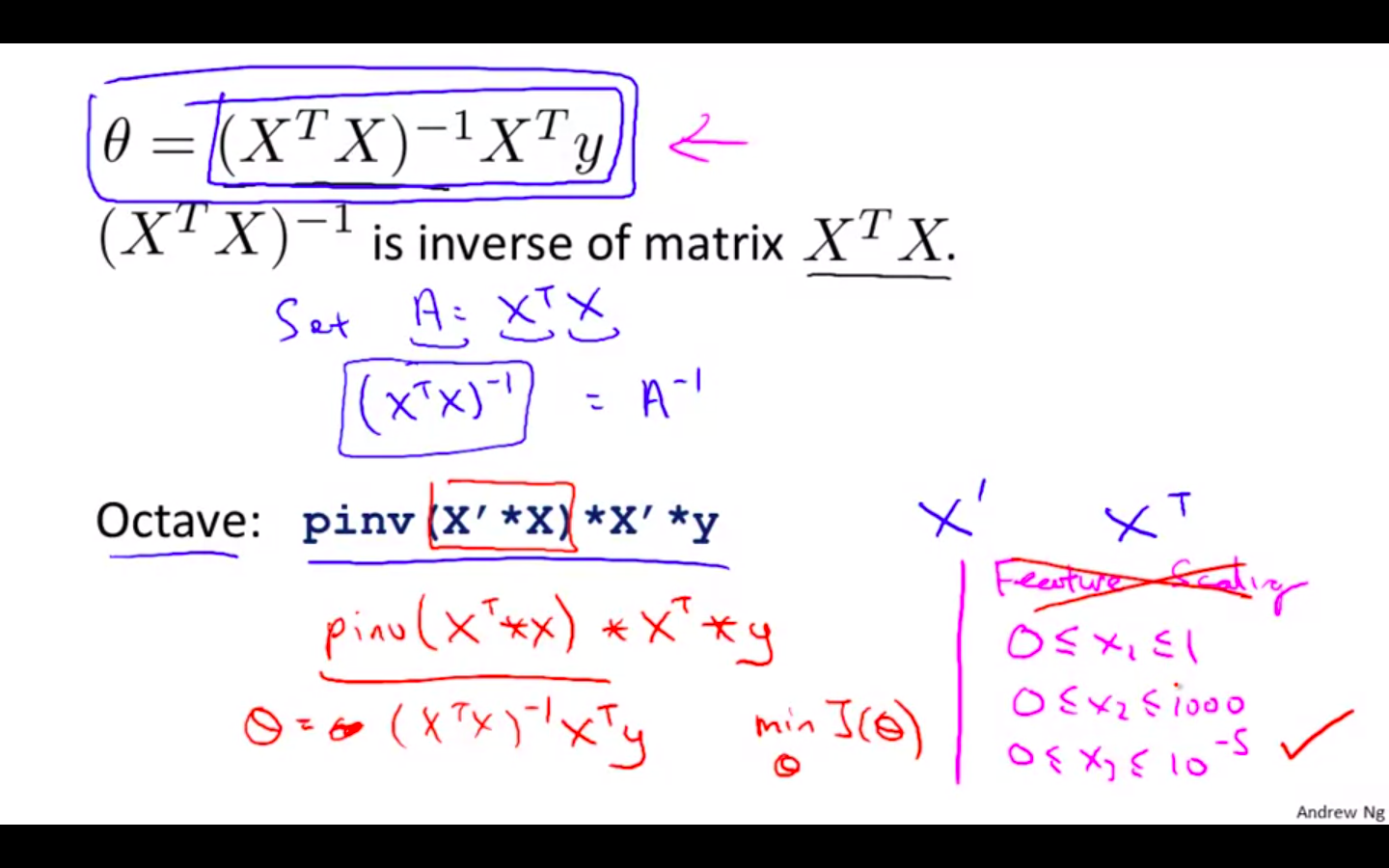

“Normal Equation” method, we will minimise J by explicitly taking its derivatives with respect to the θj ’s, and setting them to zero.

-

This allows us to find the optimum theta without iteration.

-

Intuition

-

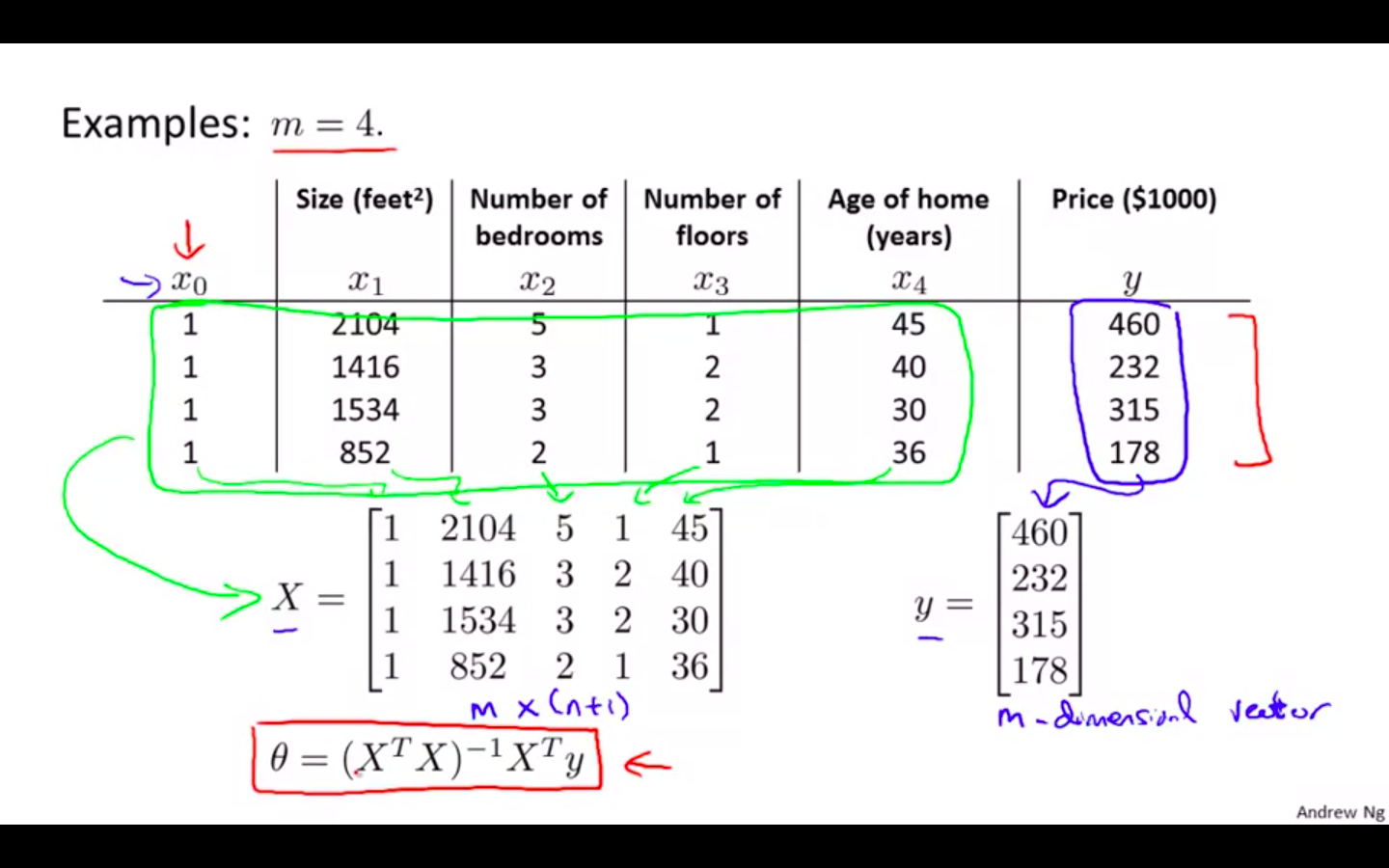

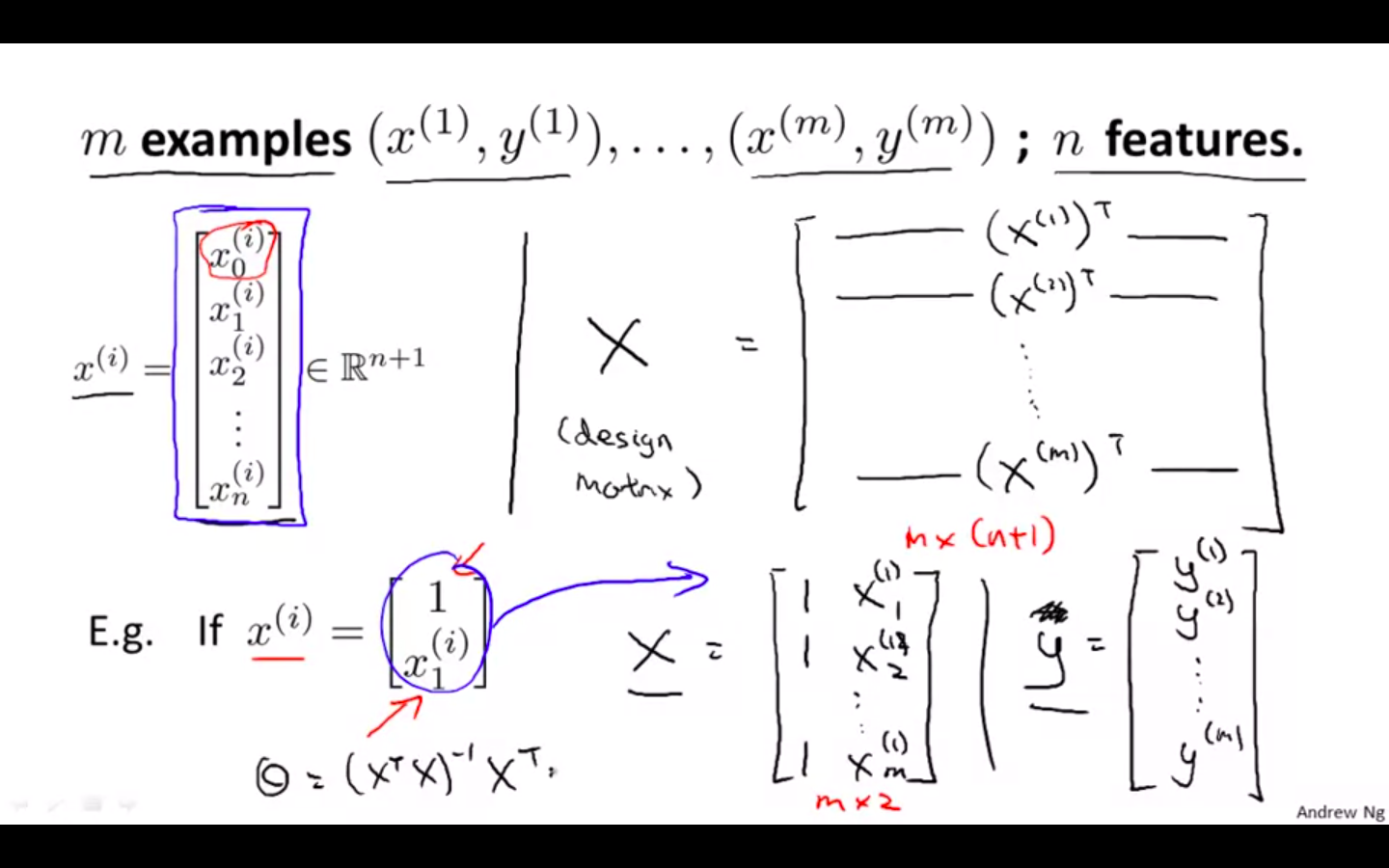

Example

-

X - features matrix

-

y - output matrix

-

m examples, n features

-

X - also called as design matrix

-

Feature Scaling is not needed while using normal equation method

-

Normal Equation Octave Representation

-

pinv( X' * X ) * X' * y

-

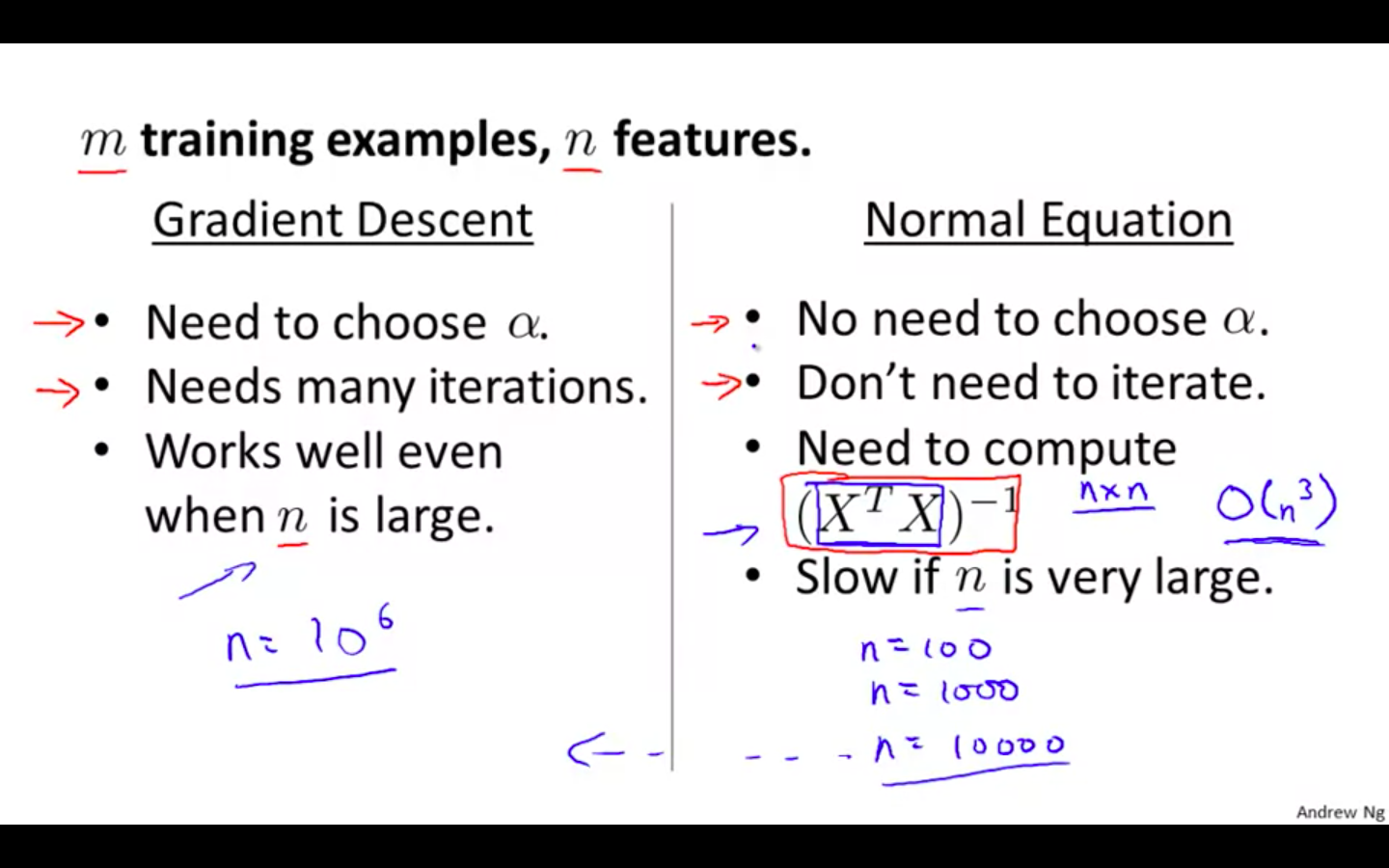

Comparison Between Gradient Descent & Normal Equation

-

n = Normal Equation Gradient Descent

-

For some algorithms, normal equation method doesn’t work

-

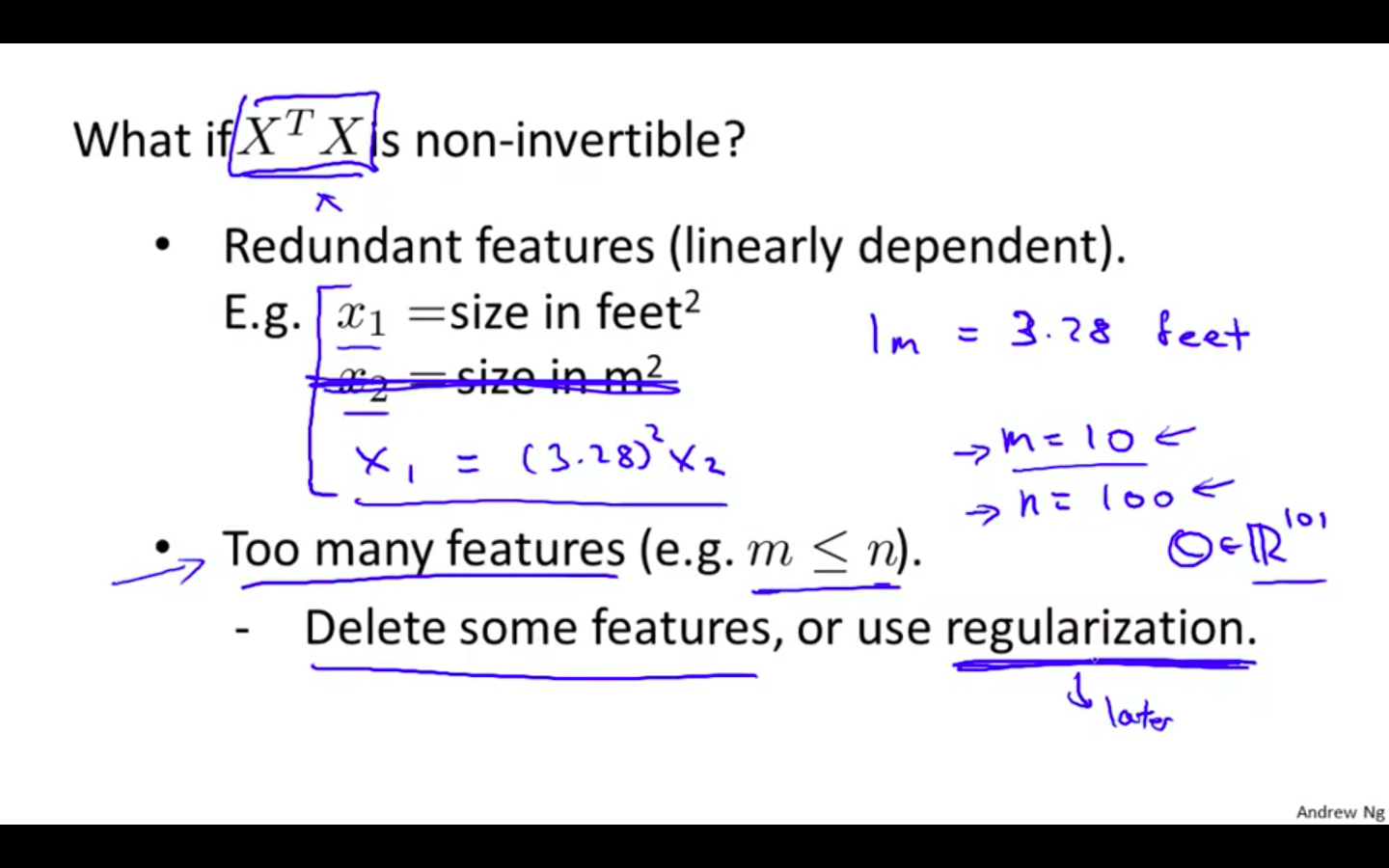

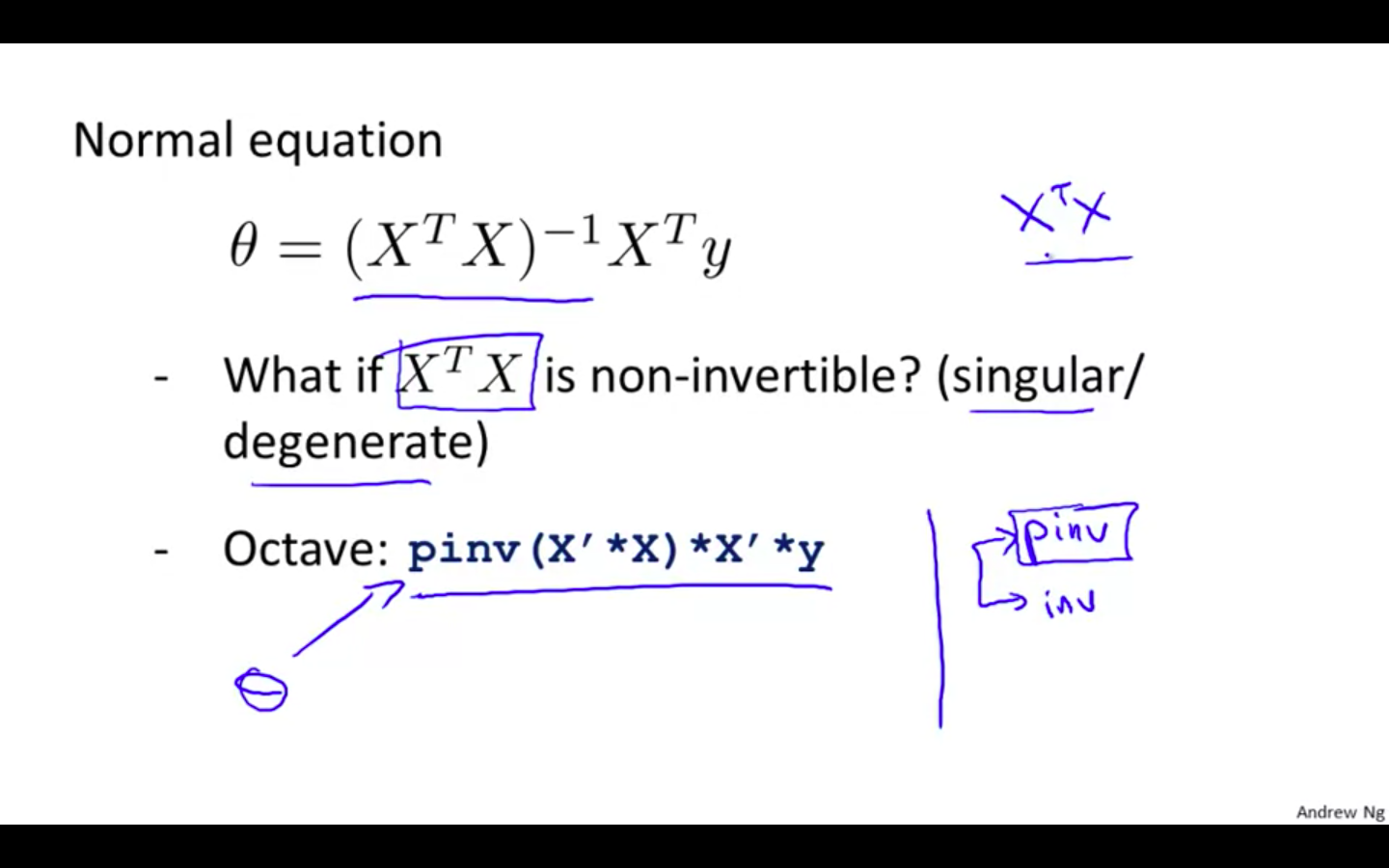

Normal Equation Noninvertibility

-

When implementing the normal equation in octave we want to use the ‘pinv’ function rather than ‘inv.’ The ‘pinv’ function will give you a value of θ even if X^T * X is not invertible.

-

Reasons for Noninvertibility

-

Redundant features, where two features are very closely related (i.e. they are linearly dependent)

-

Too many features (e.g. m ≤ n). In this case, delete some features or use “regularisation”.

-

-

Solution

- deleting a feature that is linearly dependent with another or deleting one or more features when there are too many features.