Machine Learning By Andew Ng - Week 3

Classification and Representation

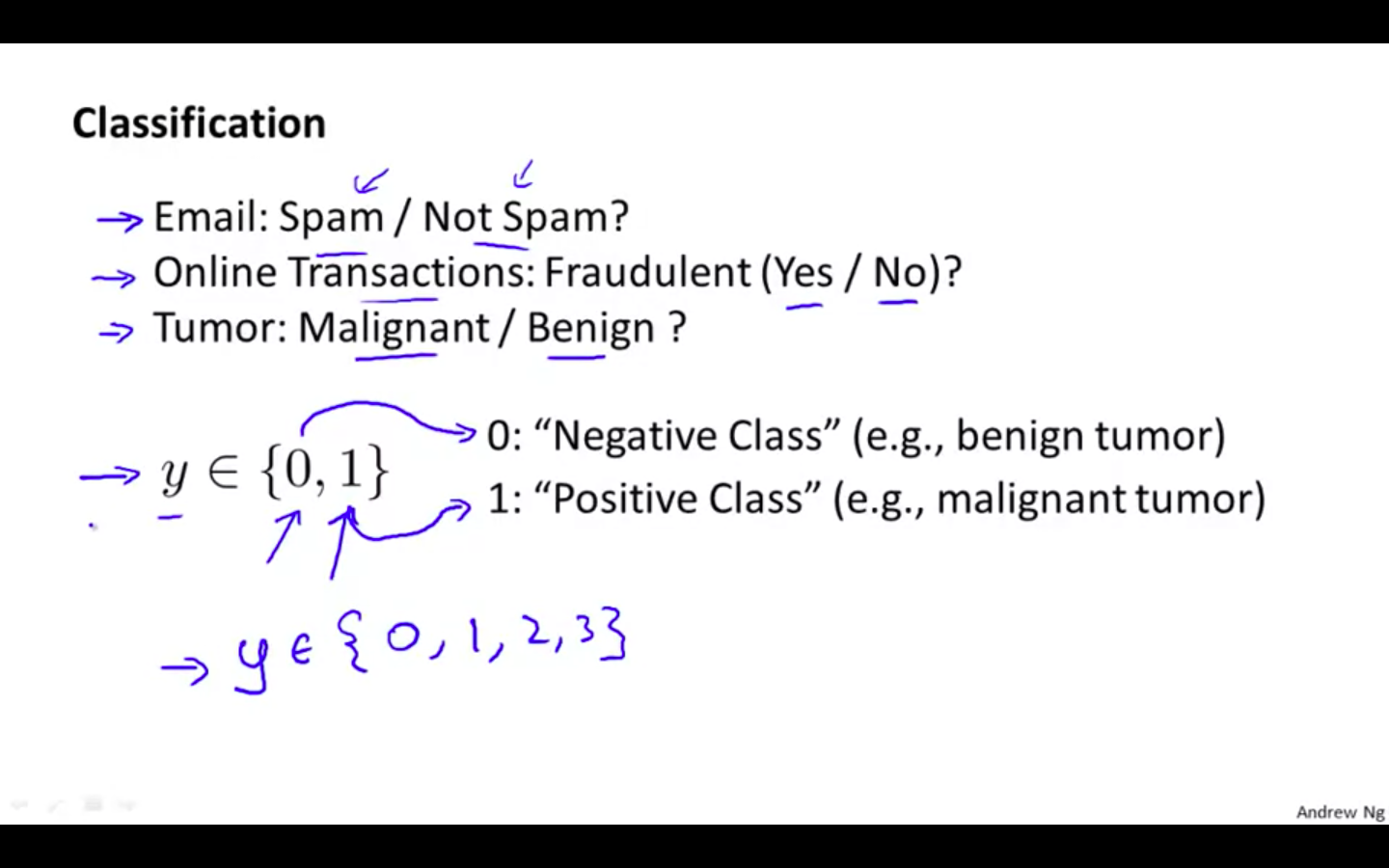

Classification

-

Use Cases

-

Email: Spam / Not Spam

-

Online Transactions: Fraudulent (Yes / No )?

-

Tumor: Malignant / Benign ?

-

-

Binary Classification

-

0 - Negative class

- conveys something is absent

-

1 - Positive class

- conveys something is present

-

-

Example:

-

Applying linear regression to a classification problem is not a good idea

-

To attempt classification, one method is to use linear regression and map all predictions greater than 0.5 as a 1 and all less than 0.5 as a 0.

-

This method doesn’t work well because classification is not actually a linear function.

-

-

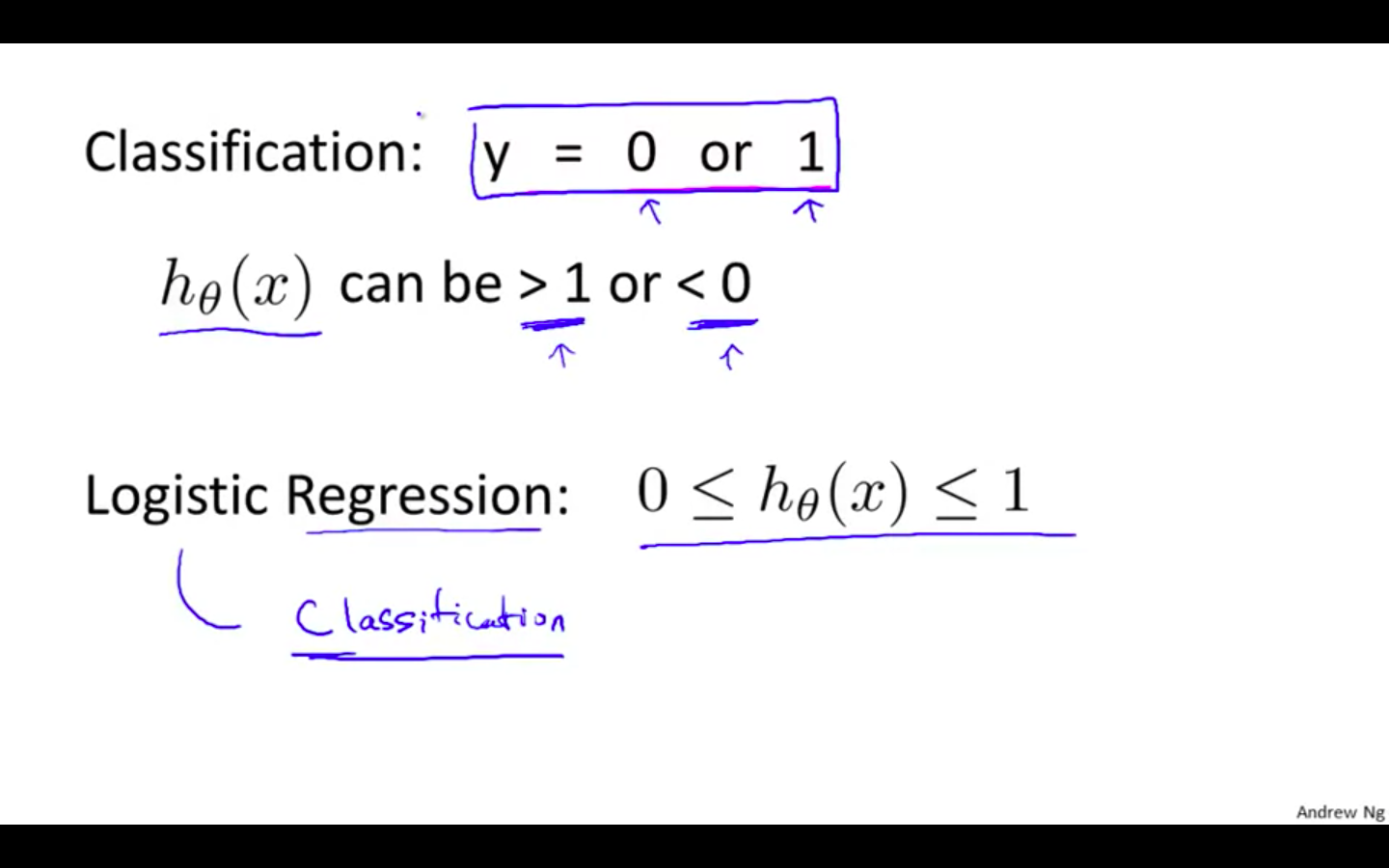

Classification

-

Linear regression can produce value larger than 1 or smaller than 0

-

In classification problem, label are either 1 or 0.

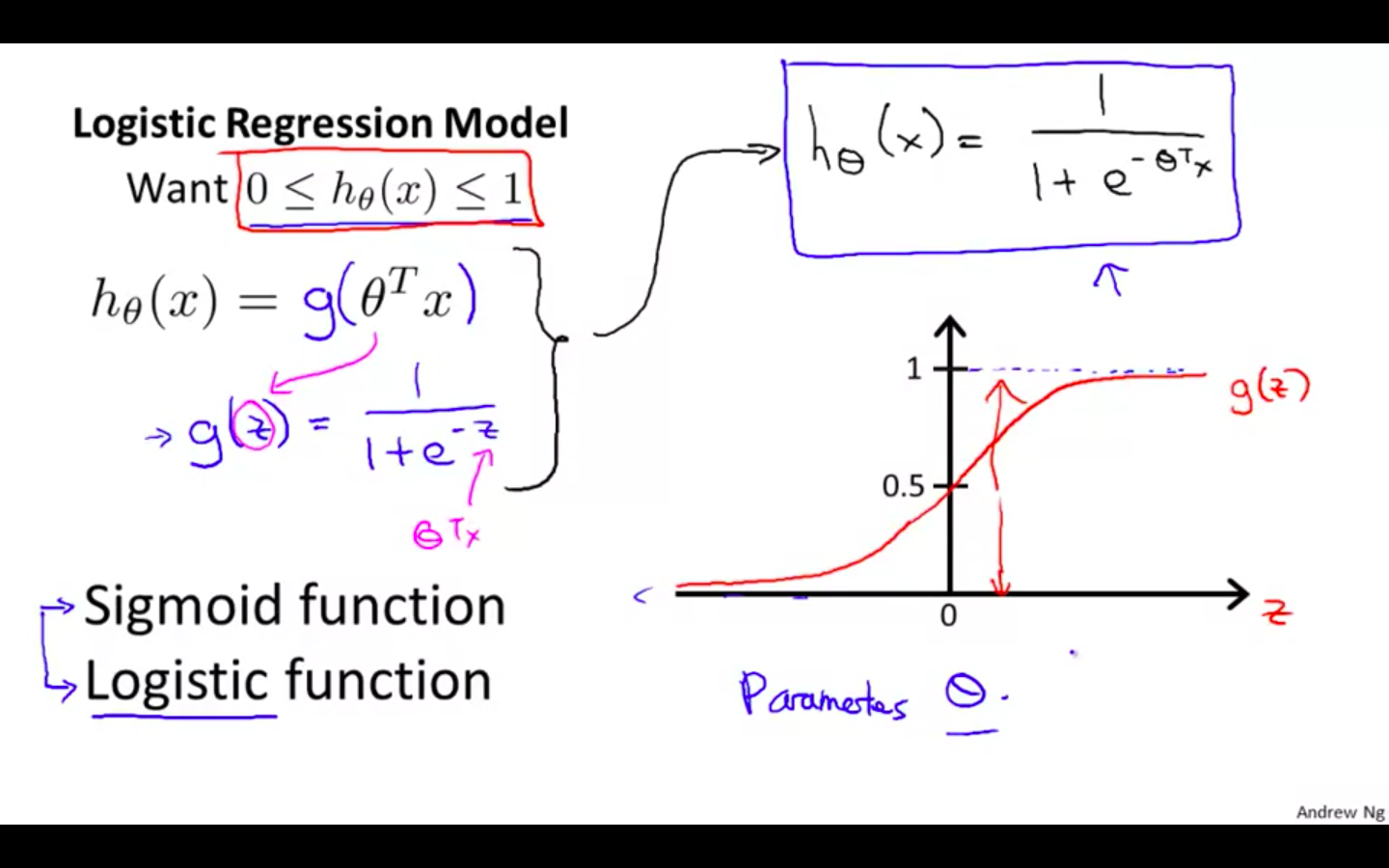

- Logistic Regression: 0 ≤ h(x) ≤ 1

-

-

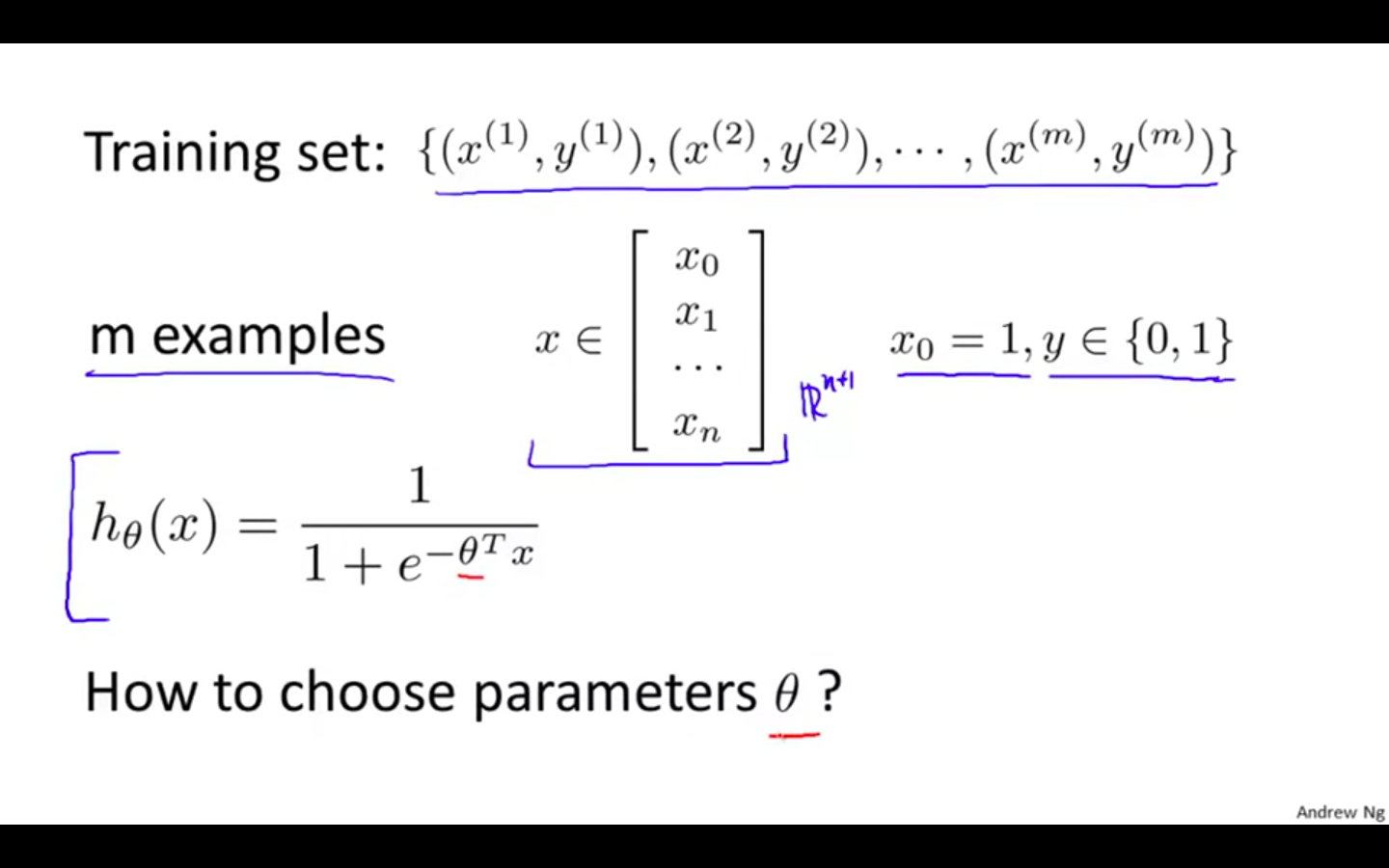

Hypothesis Representation

-

Sigmoid function is zero at negative infinity and 1 at positive infinity

- Sigmoid function == Logistic Function

-

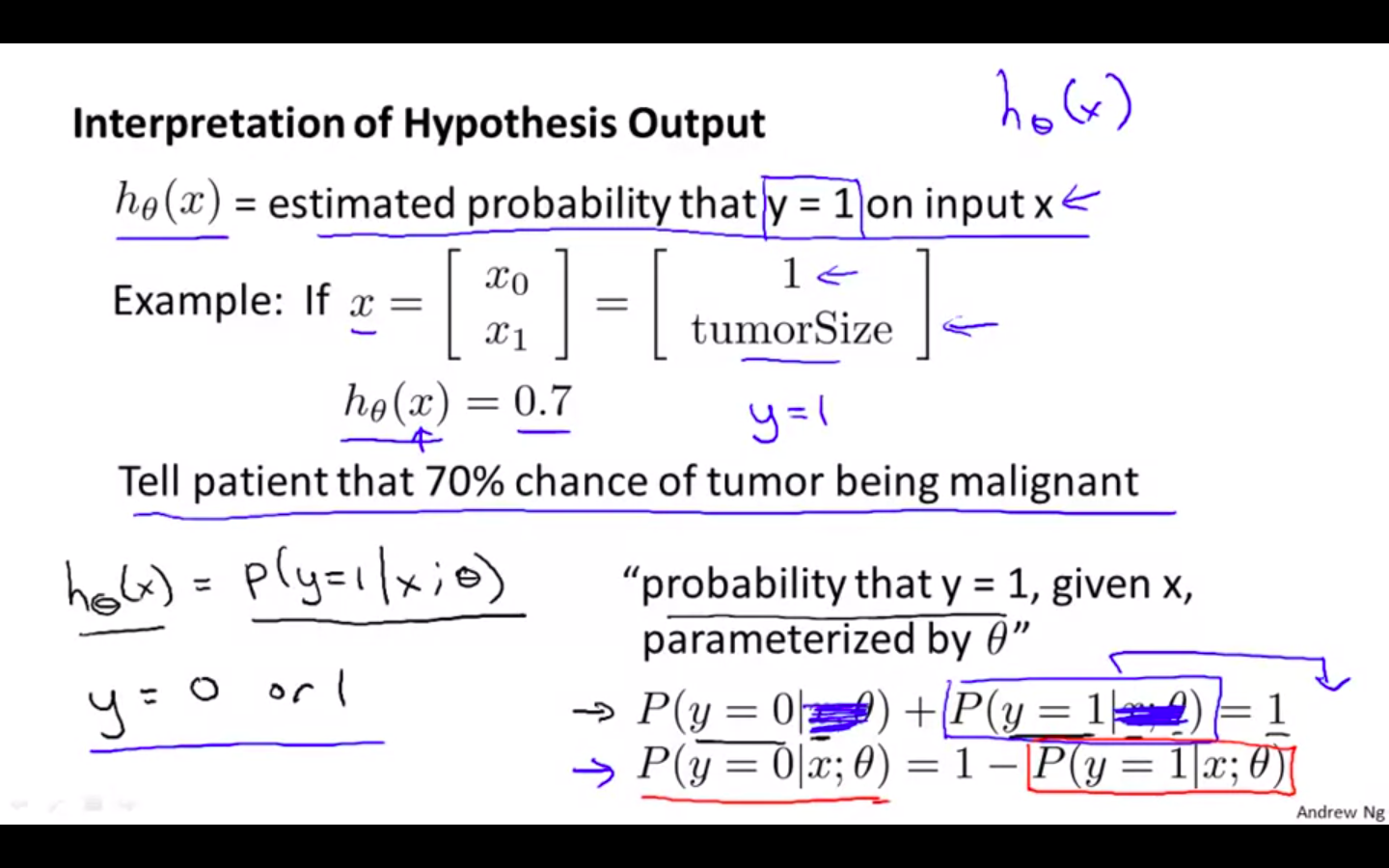

Interpretation Of Hypothesis

- h ( x ) = estimated probability that y = 1 on input

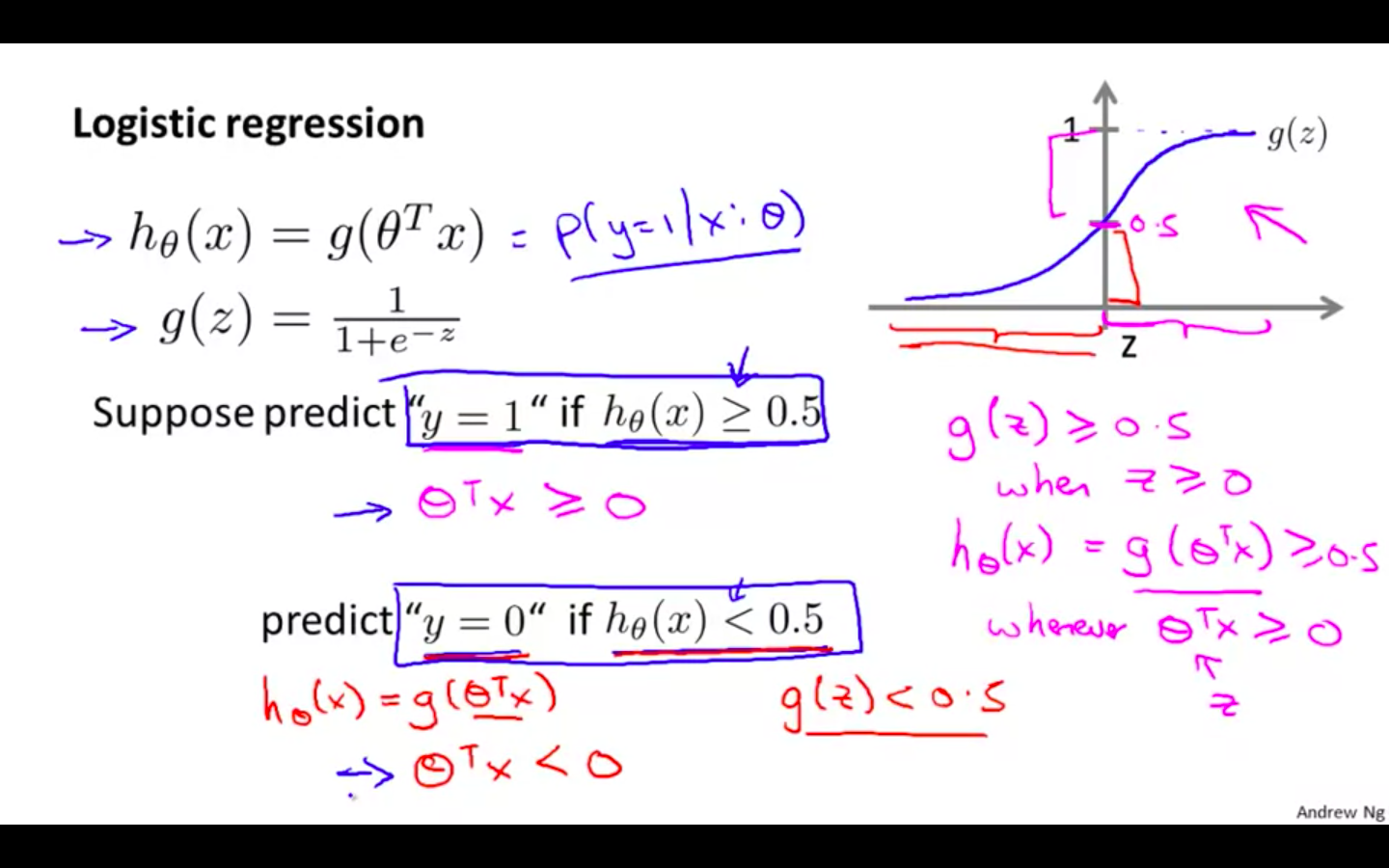

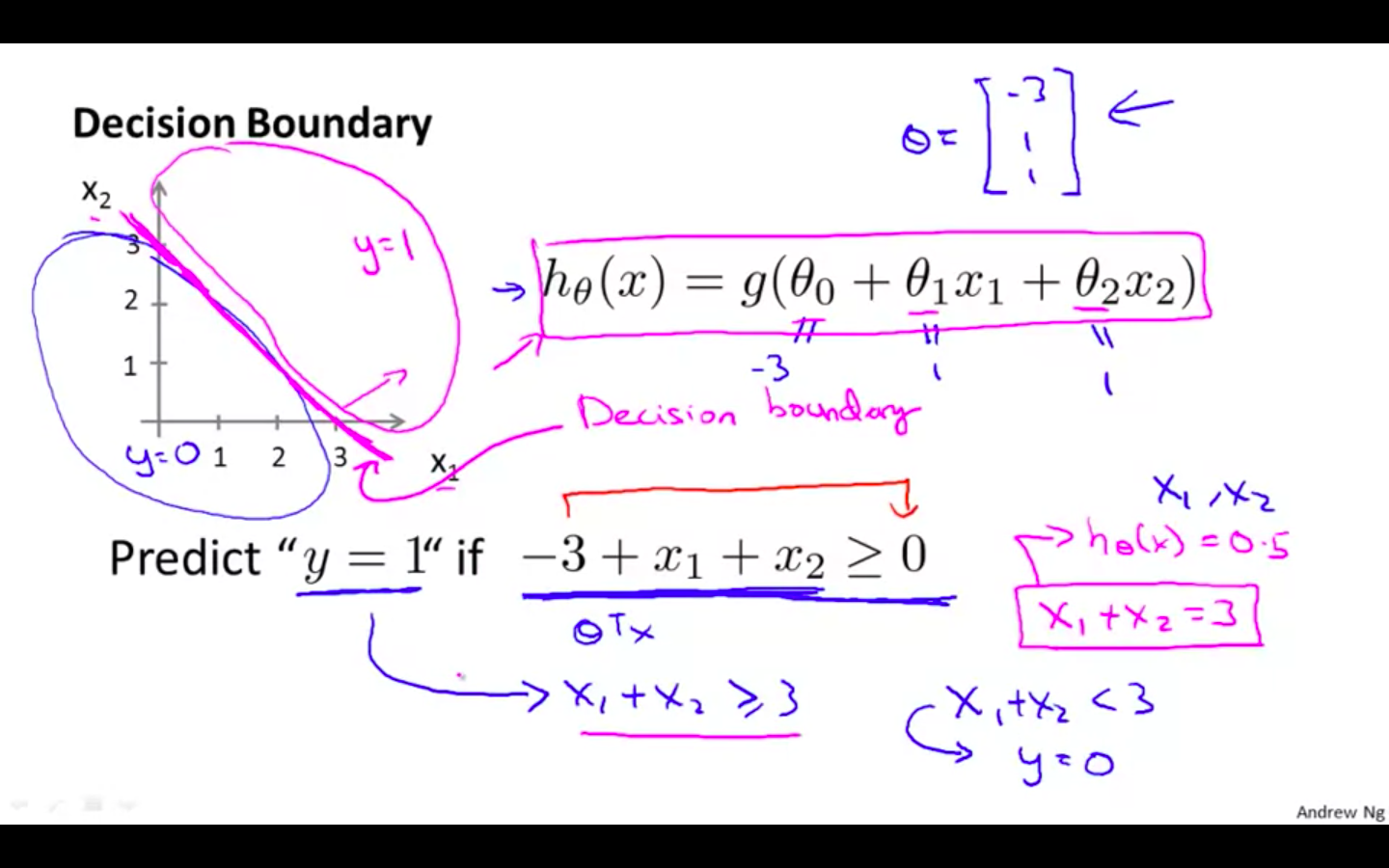

Decision Boundary

-

Predict y = 1

-

h ( x ) ≥ 0.5 : y = 1

-

thetha^T X ≥ 0

-

-

Predict y = 0

- h ( x )

-

Decision boundary

-

The decision boundary is the line that separates the area where y = 0 and where y = 1.

-

It is created by our hypothesis function.

-

This is the property of the hypothesis and not of the data

-

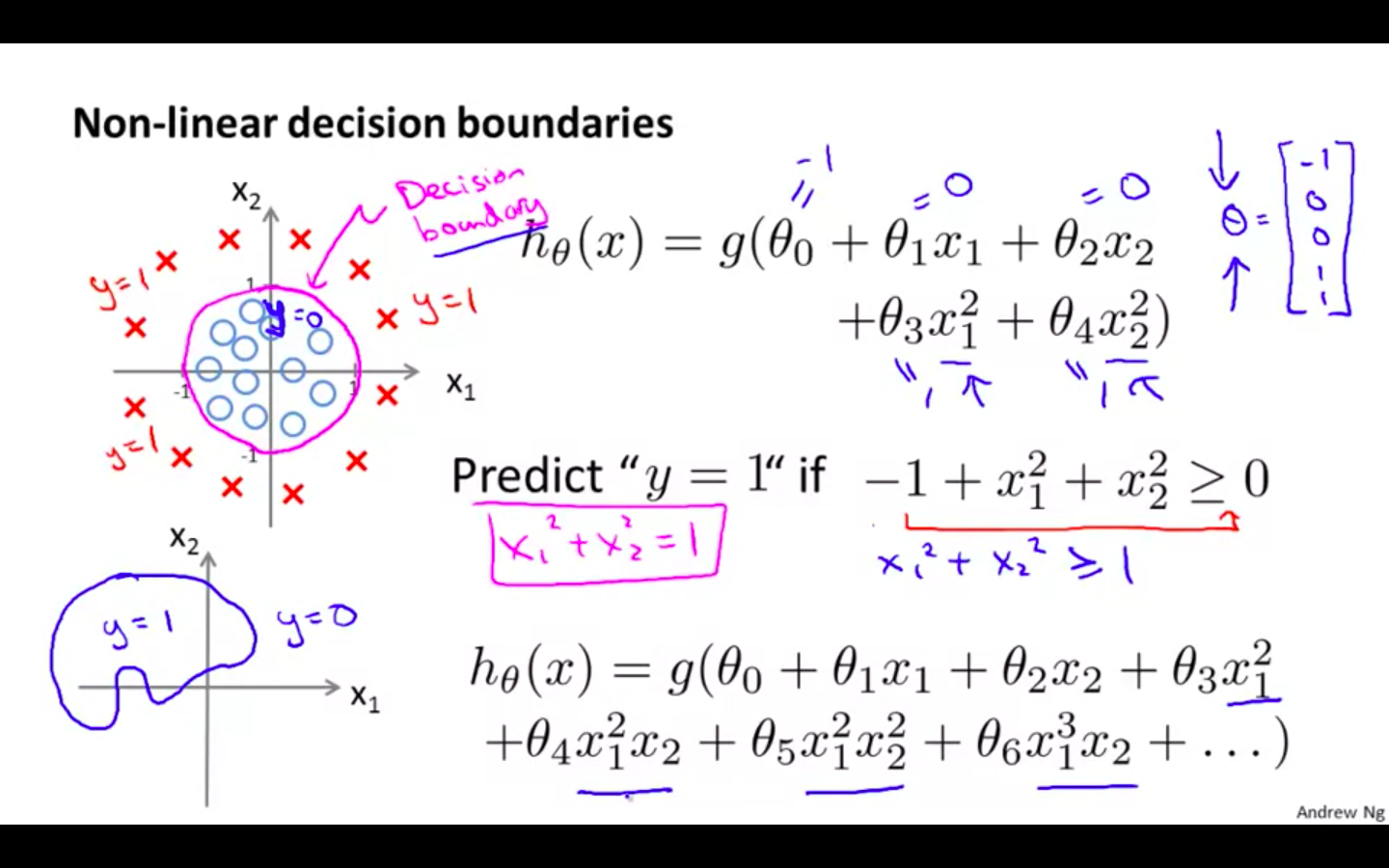

Non Linear Decision Boundary

-

Decision Boundary doesn’t need to be linear

-

High order polynomials can also be resulted in a complex decision boundary

-

-

Logistic Regression Model

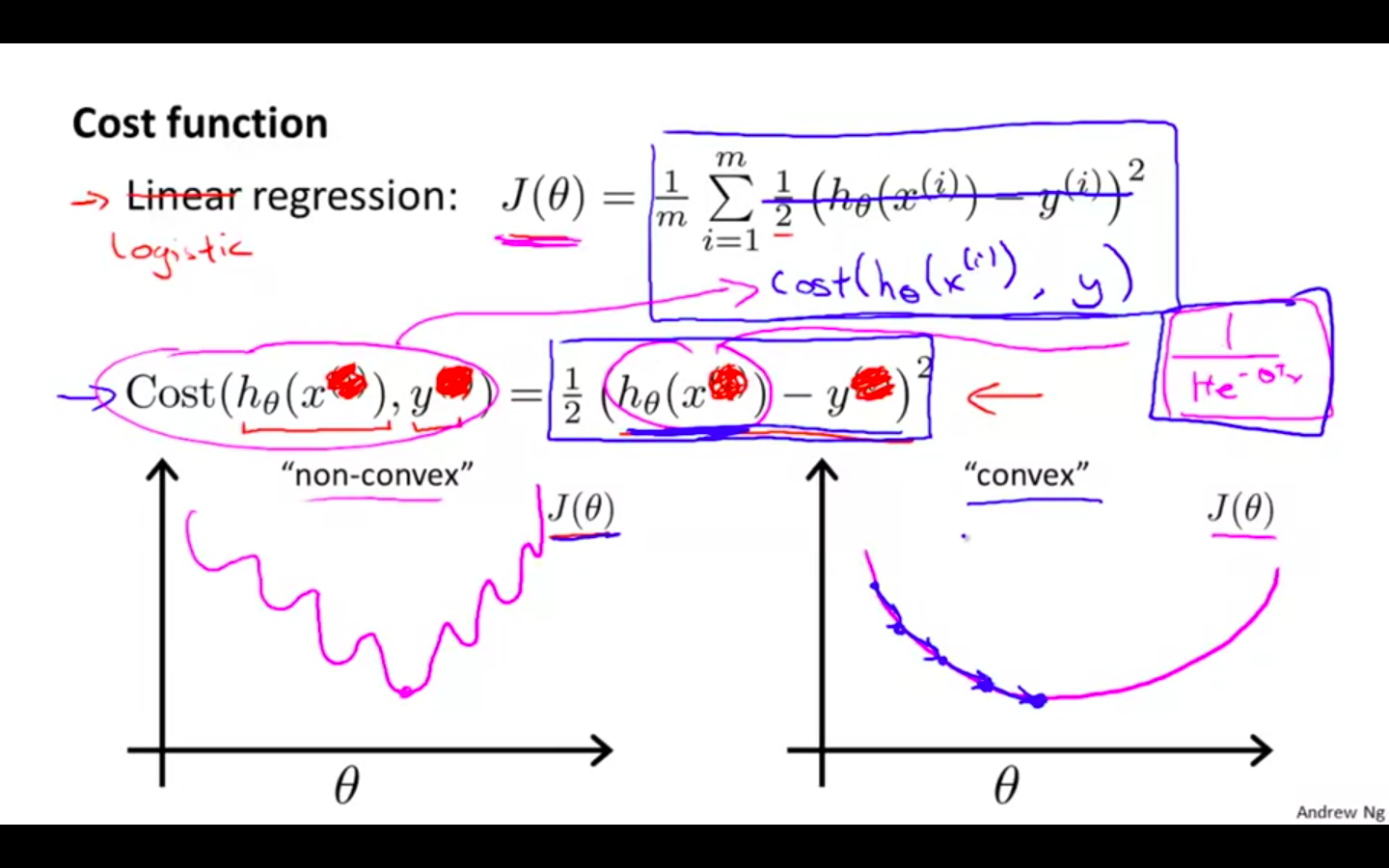

Cost Function

-

Concept

-

We cannot use the same cost function that we use for linear regression because the Logistic Function will cause the output to be wavy, causing many local optima.

-

In other words, it will not be a convex function.

-

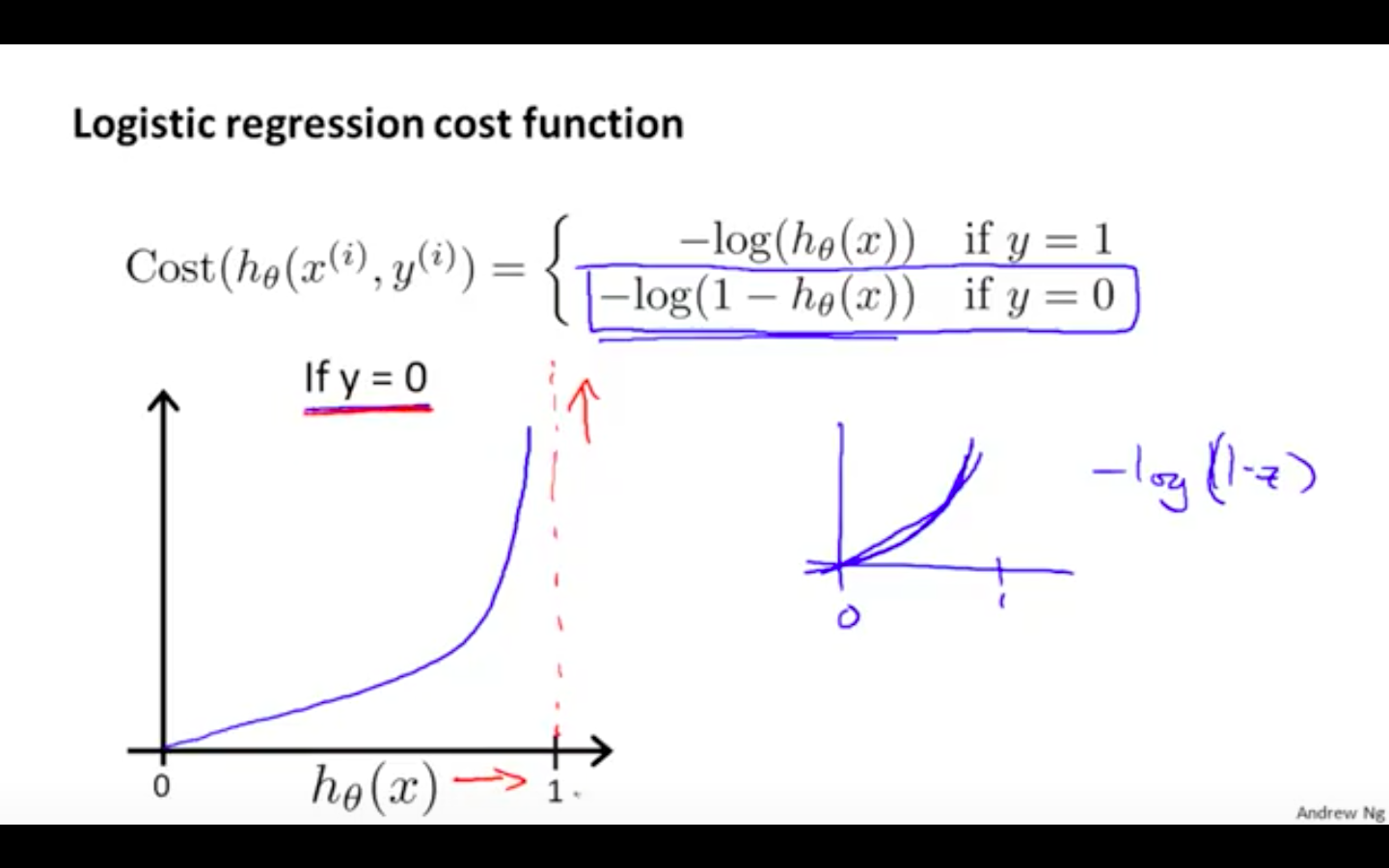

Case 1

-

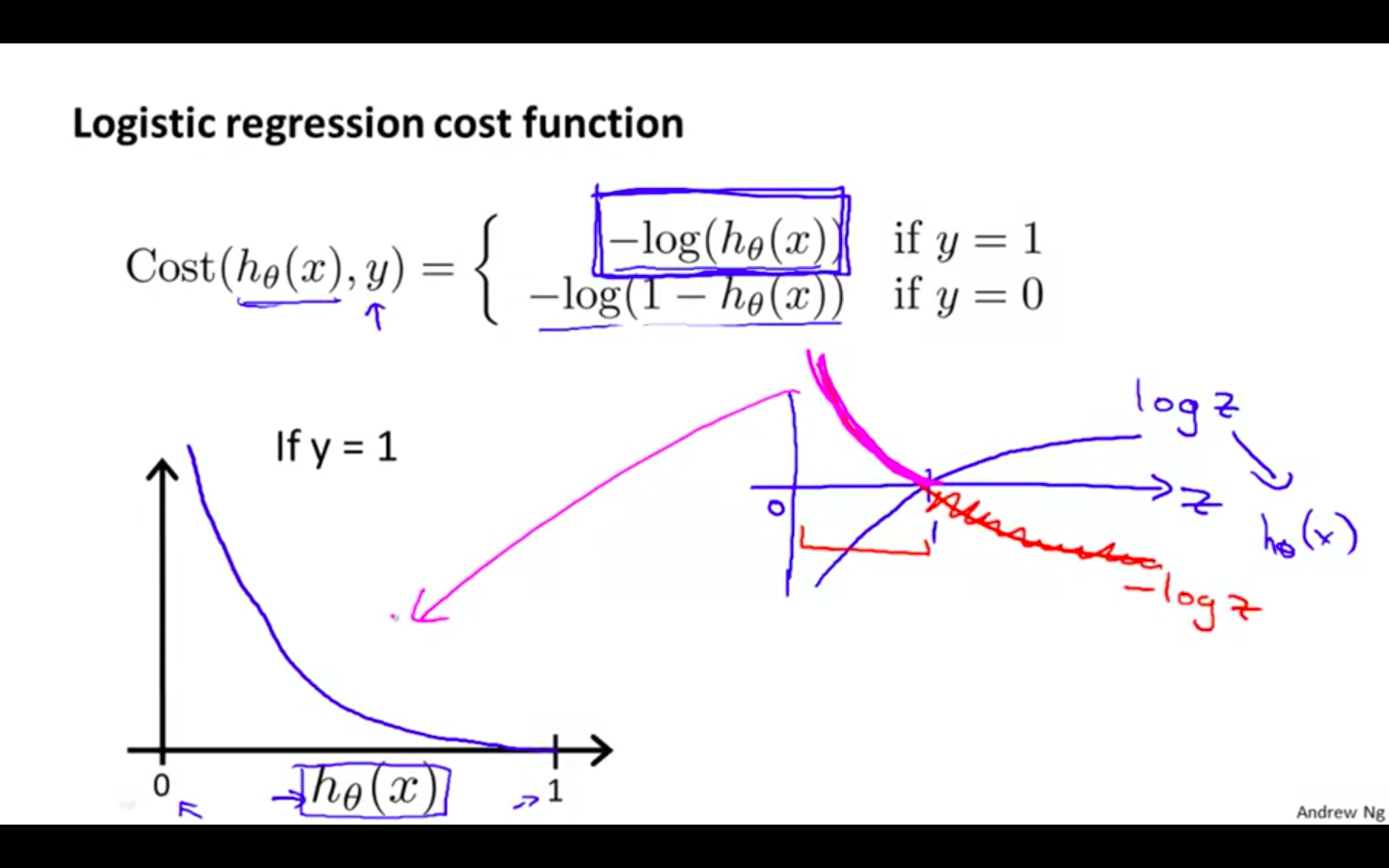

When y = 1, we get the following plot for J (theta) vs h ( x )

-

If our correct answer ‘y’ is 1, then the cost function will be 0 if our hypothesis function outputs 1.

-

If our hypothesis approaches 0, then the cost function will approach infinity.

-

-

-

Case 2

-

When y = 0, we get the following plot for J (theta) vs h ( x )

-

If our correct answer ‘y’ is 0, then the cost function will be 0 if our hypothesis function also outputs 0.

-

If our hypothesis approaches 1, then the cost function will approach infinity.

-

-

-

Note that writing the cost function in this way guarantees that J(θ) is convex for logistic regression.

Simplified Cost Function and Gradient Descent

-

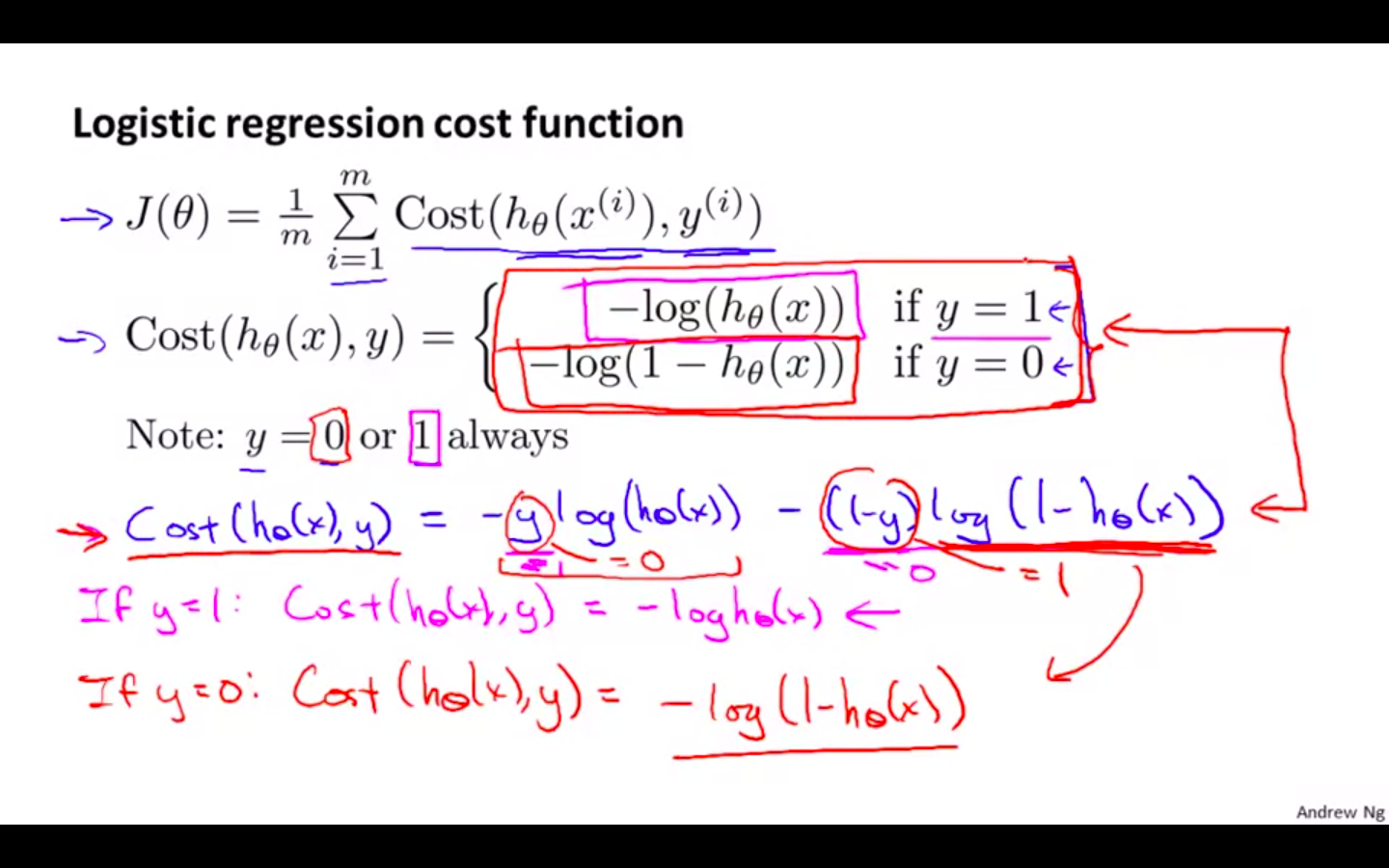

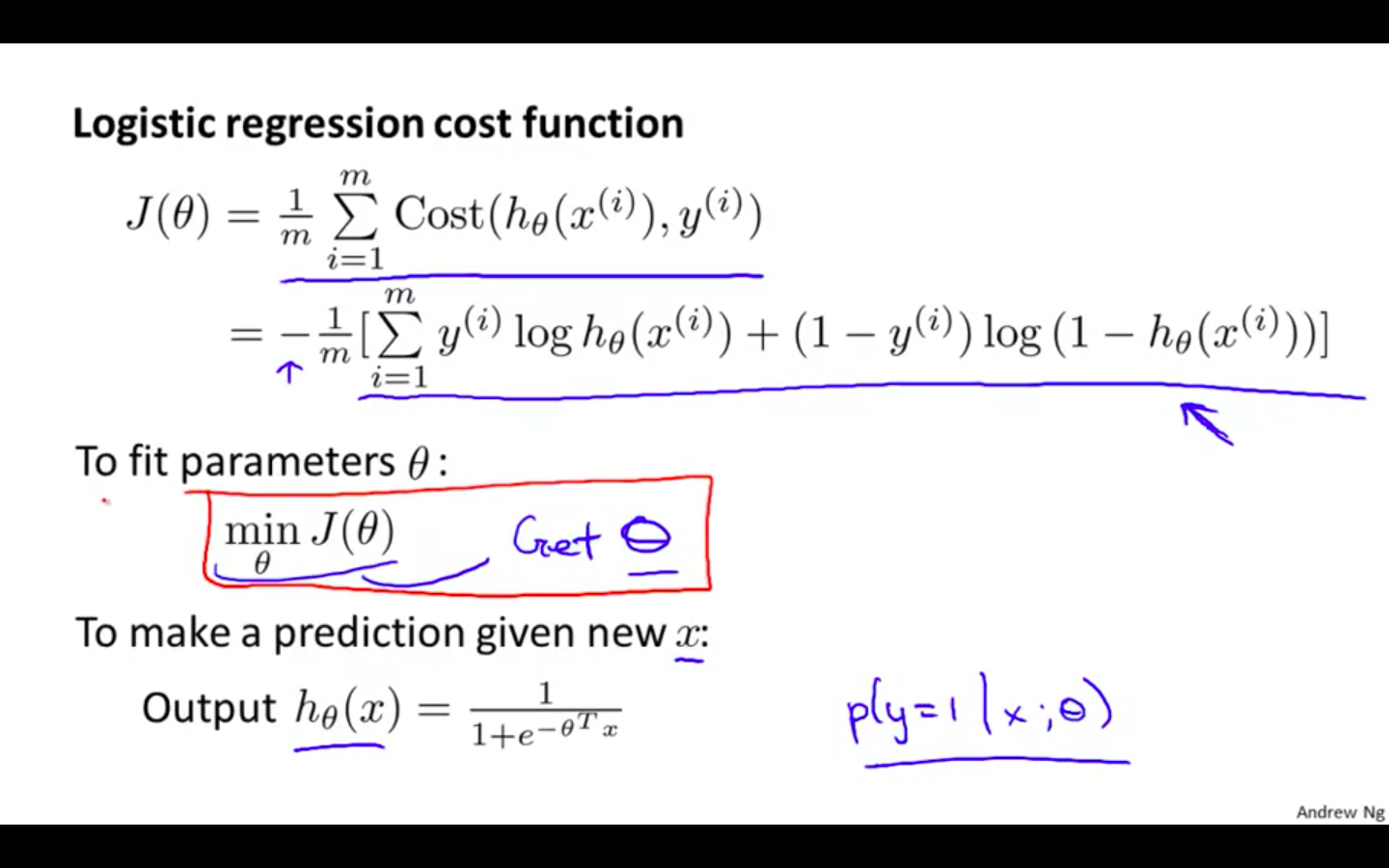

Modified Cost Function ( Simple )

- Compress our cost function’s two conditional cases into one case:

- We can fully write out our entire cost function as follows:

-

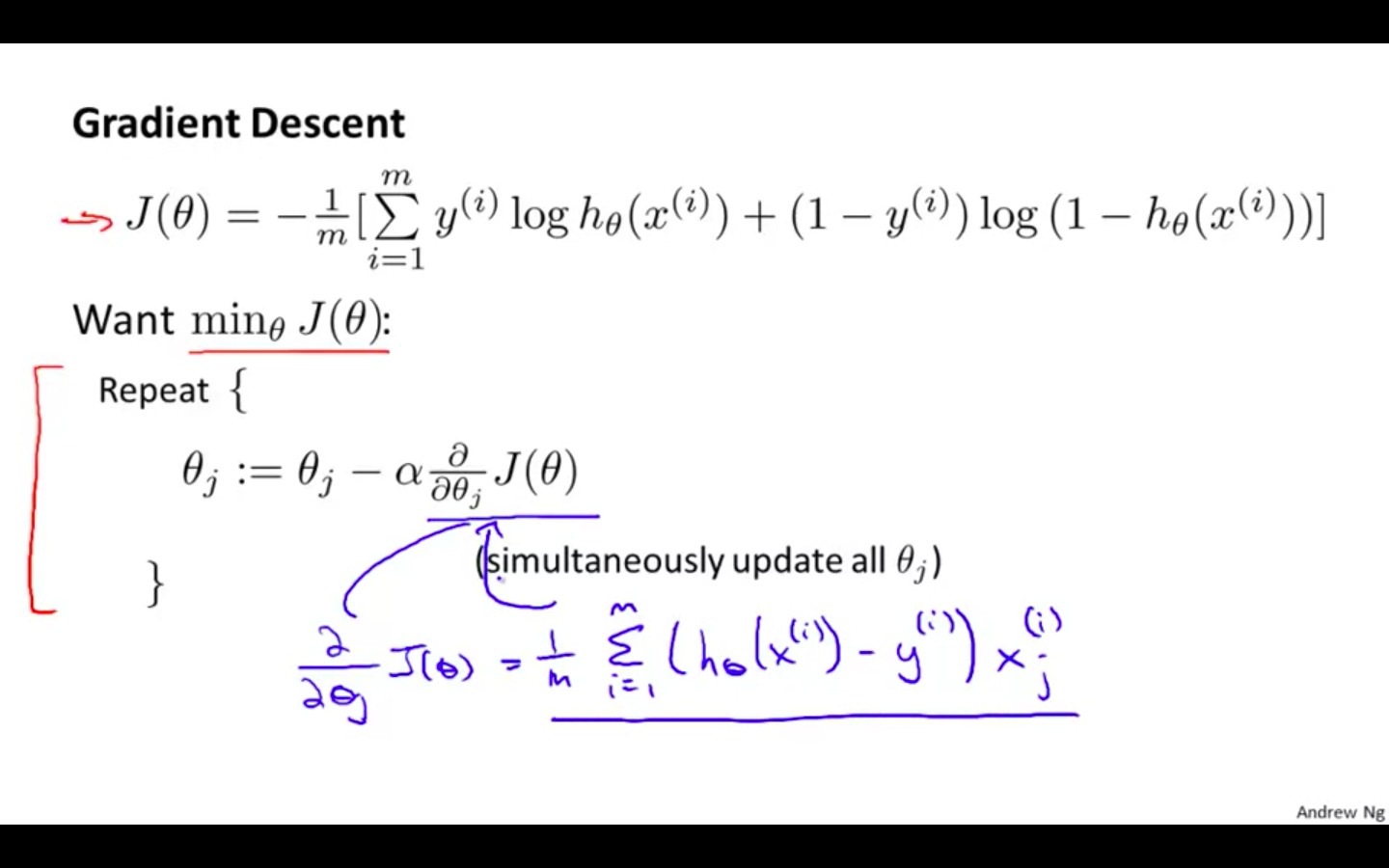

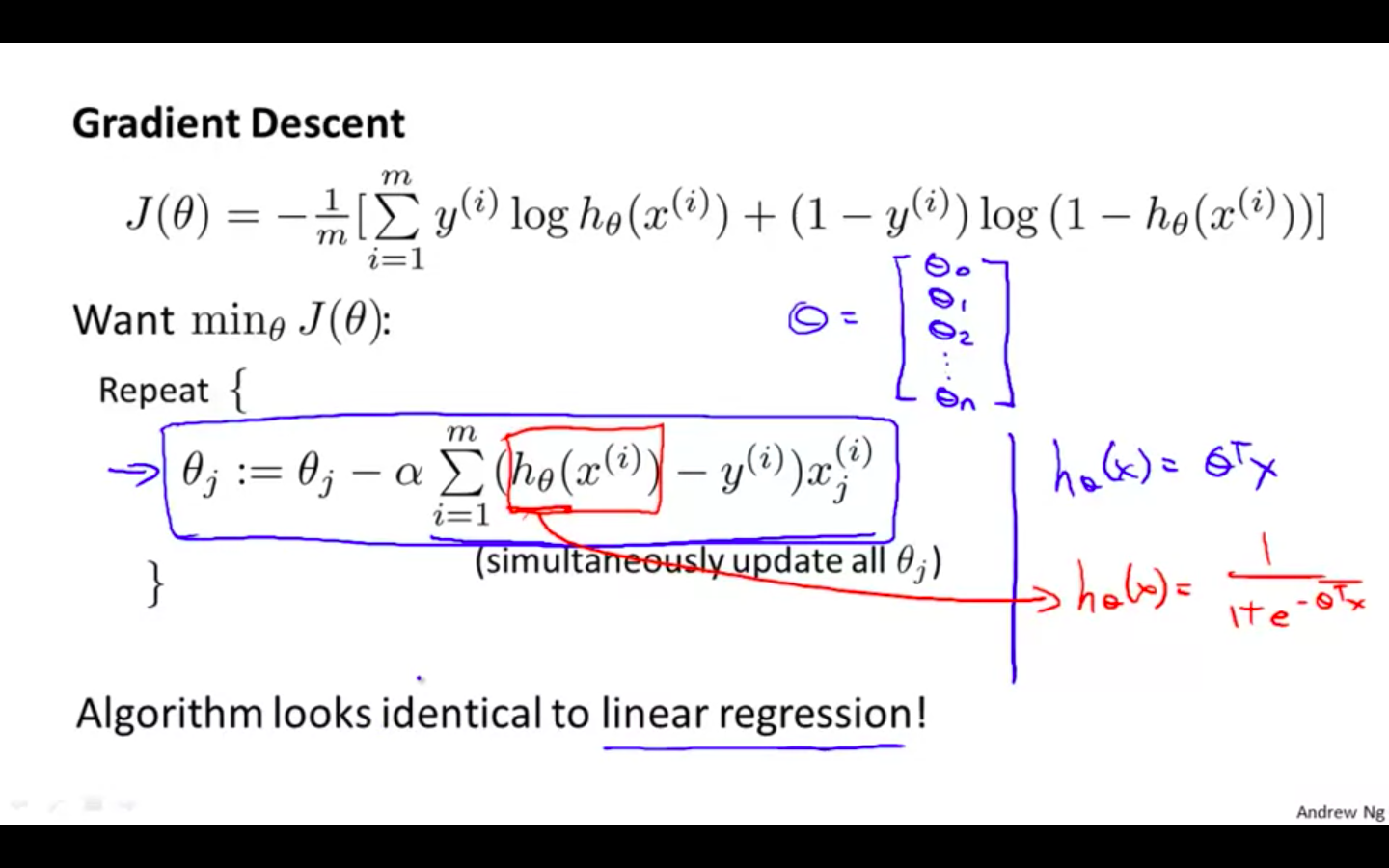

Gradient Descent

-

Notice that this algorithm is identical to the one we used in linear regression.

-

We still have to simultaneously update all values in theta.

-

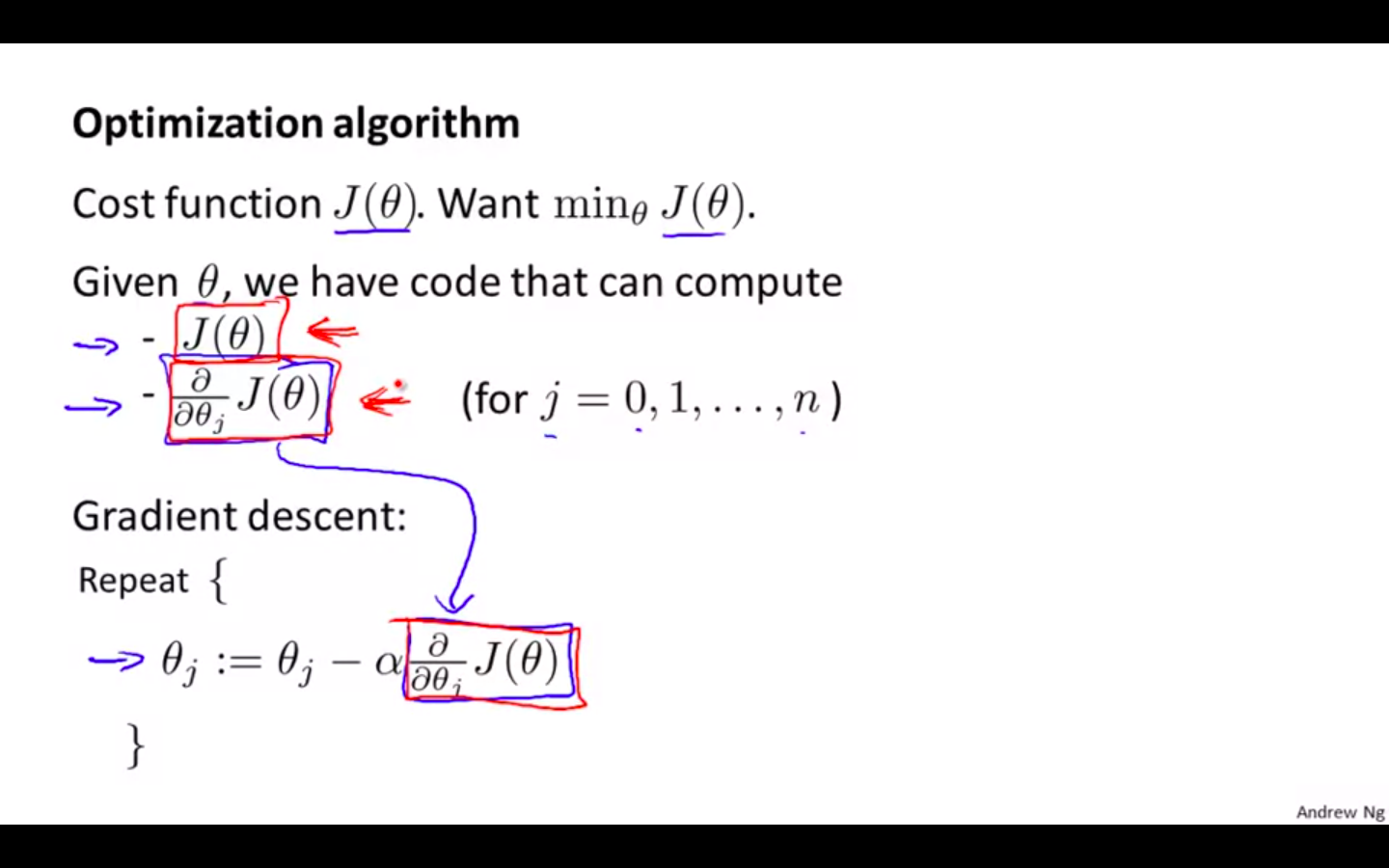

Advanced Optimisation

-

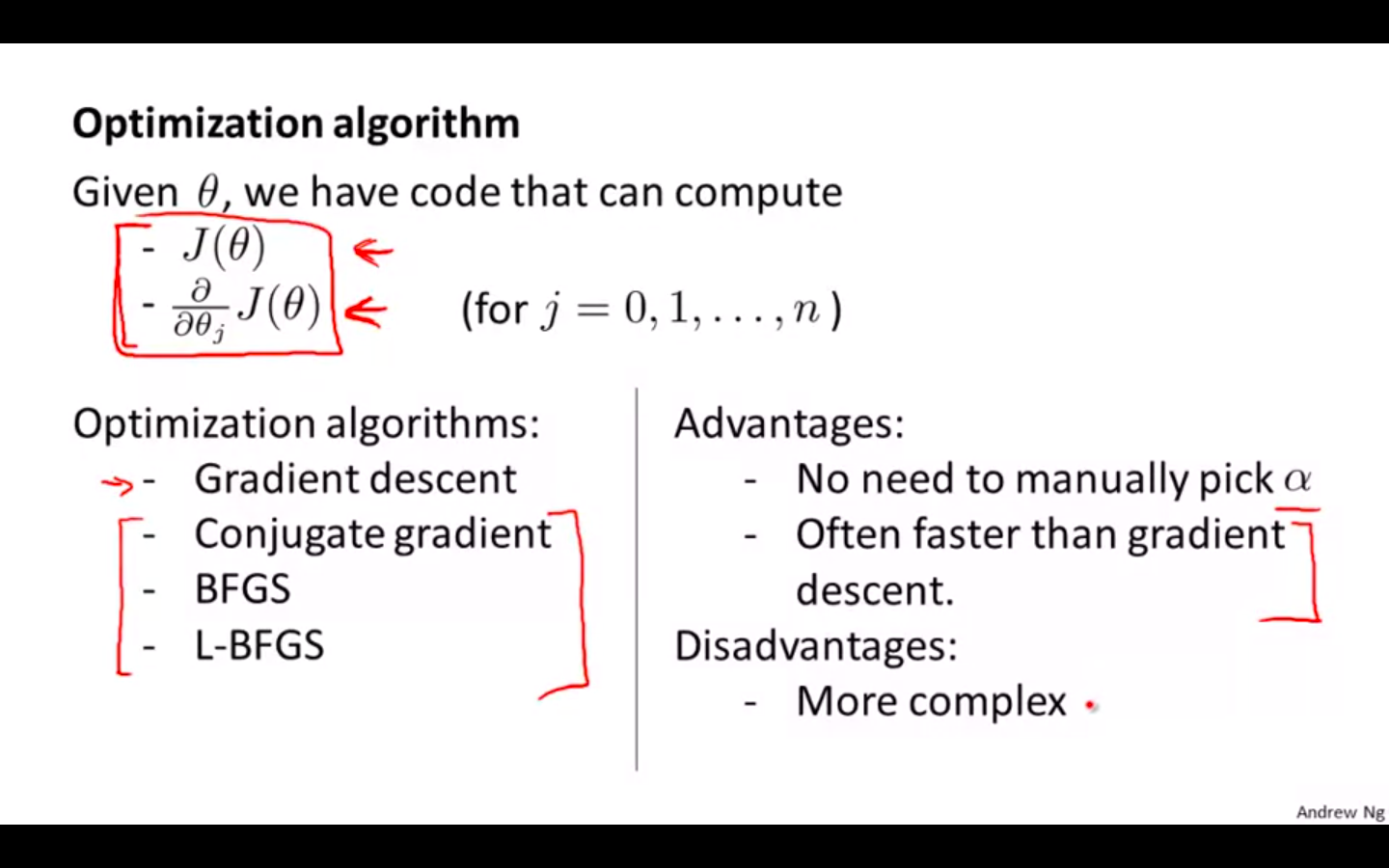

Optimisation Algorithm

- Minimising the cost function as efficient as possible

-

Advance Optimisation Algorithms

-

Algorithms

-

Gradient Descent

-

Conjugate Gradient

-

BFGS

-

L-BFGS

-

-

Advantages

-

No need to manually pick alpha

-

Often faster than gradient descent

-

-

Disadvantage

- More complex

-

-

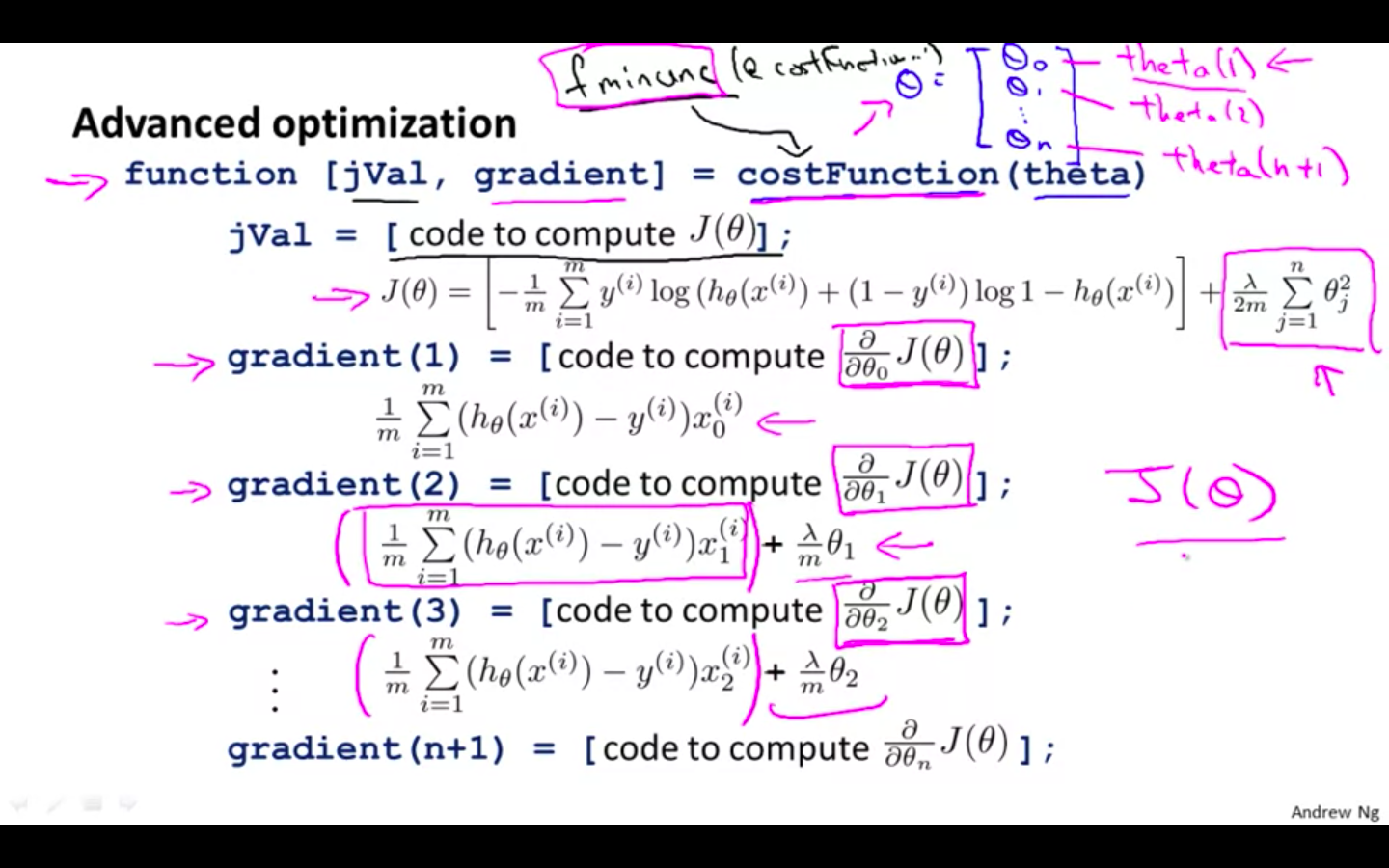

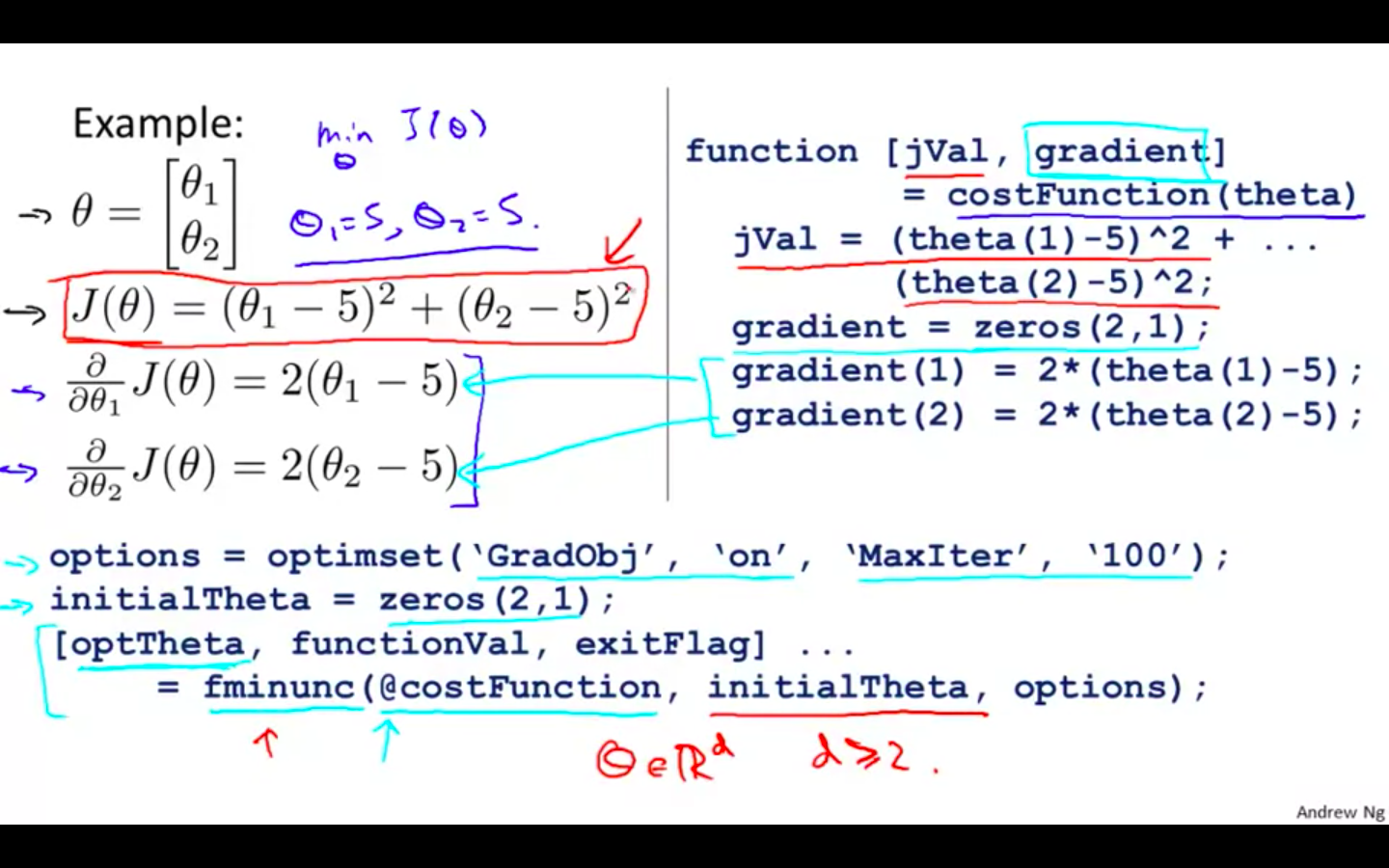

Example 1

-

Implementing function minimisation unconstrained

- fminunc() in octave programming

-

-

Example 2

-

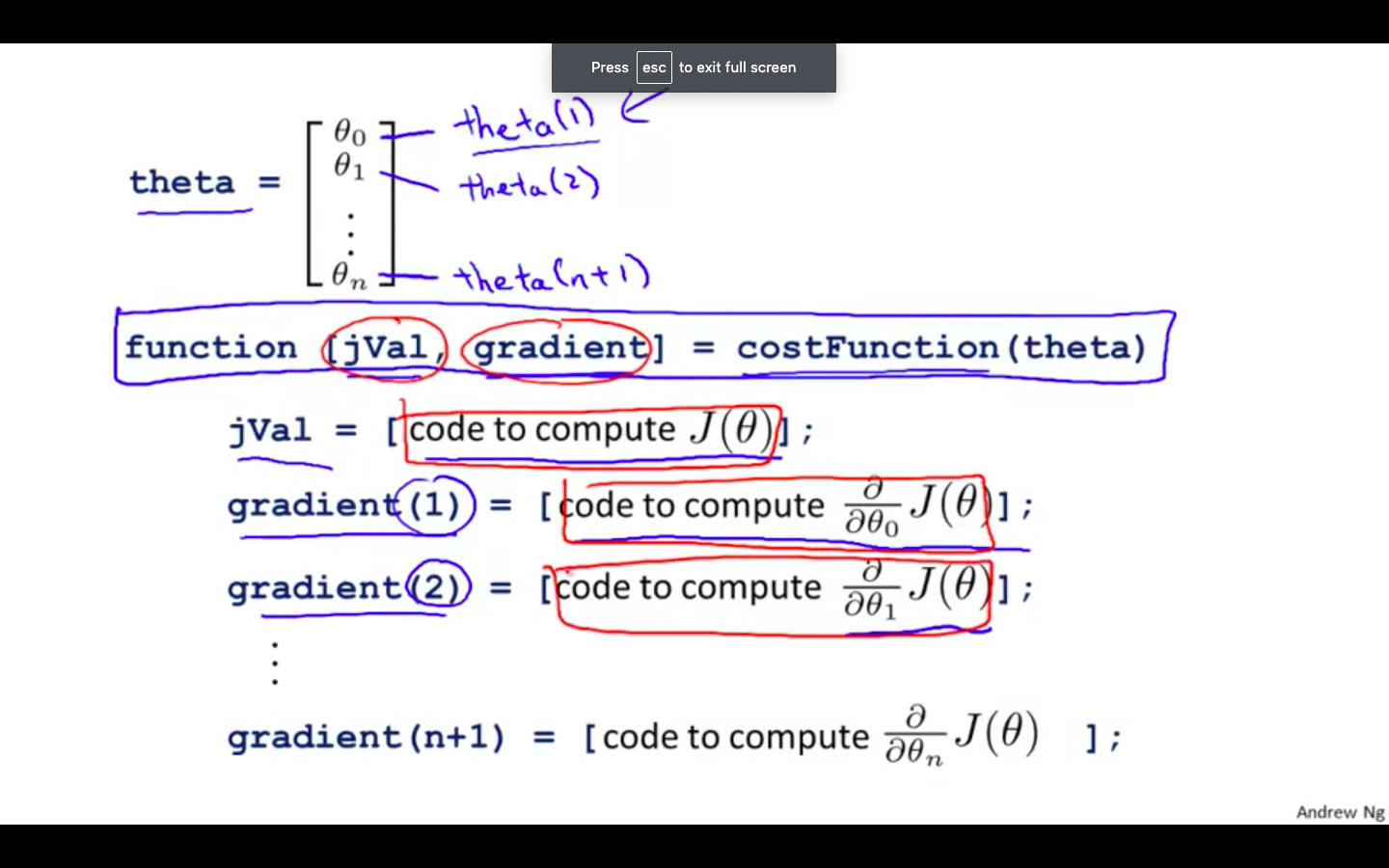

Octave / Matlab Snippets

- We can write a single function that returns both of these

function [jVal, gradient] = costFunction(theta)

jVal = [...code to compute J(theta)...];

gradient = [...code to compute derivative of J(theta)...];

end

- Then we can use octave's "fminunc()" optimization algorithm along with the "optimset()" function that creates an object containing the options we want to send to "fminunc()".

- We give to the function "fminunc()" our cost function, our initial vector of theta values, and the "options" object that we created beforehand.

options = optimset('GradObj', 'on', 'MaxIter', 100);

initialTheta = zeros(2,1);

[optTheta, functionVal, exitFlag] = fminunc(@costFunction, initialTheta, options);

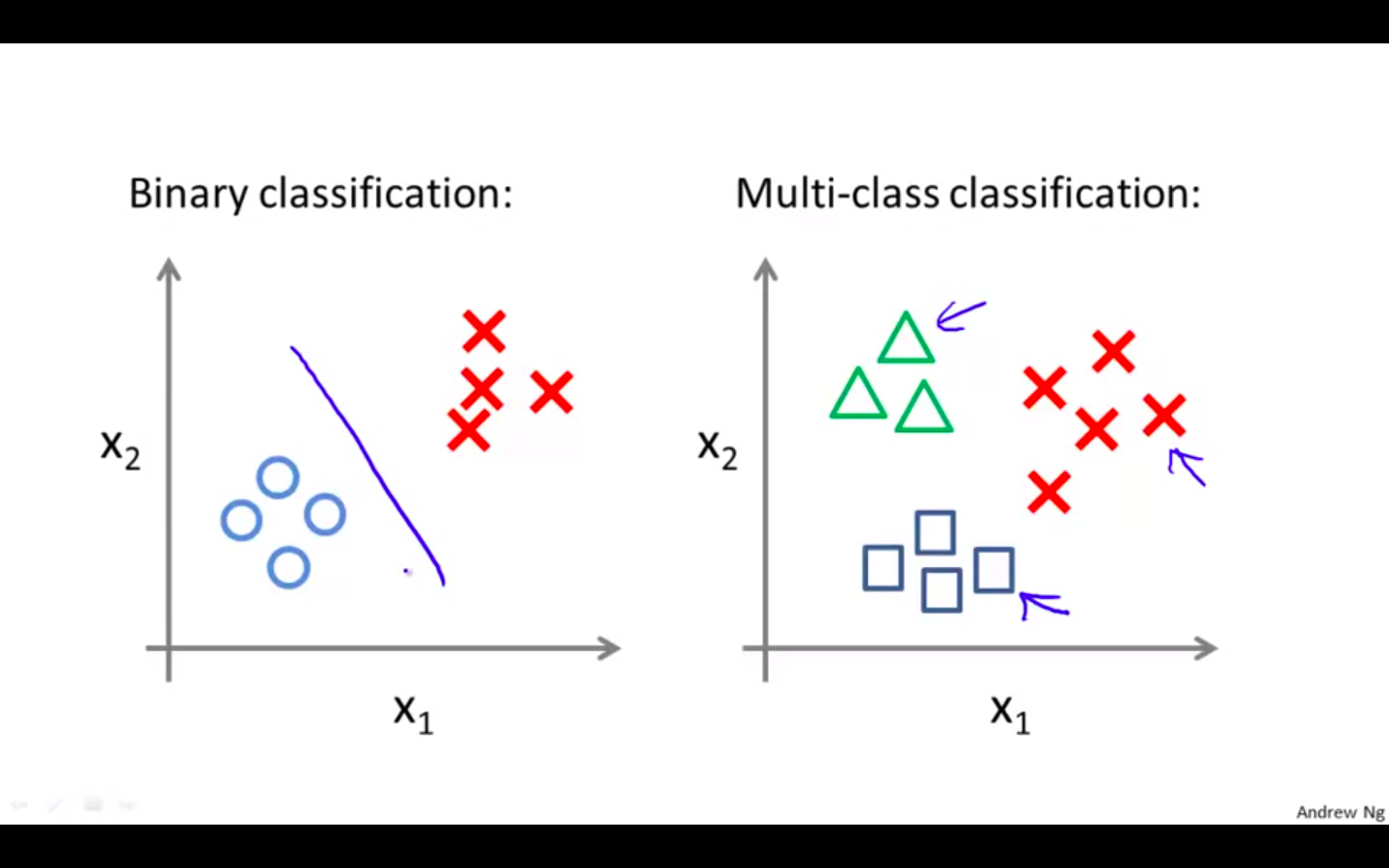

Multi-class Classification

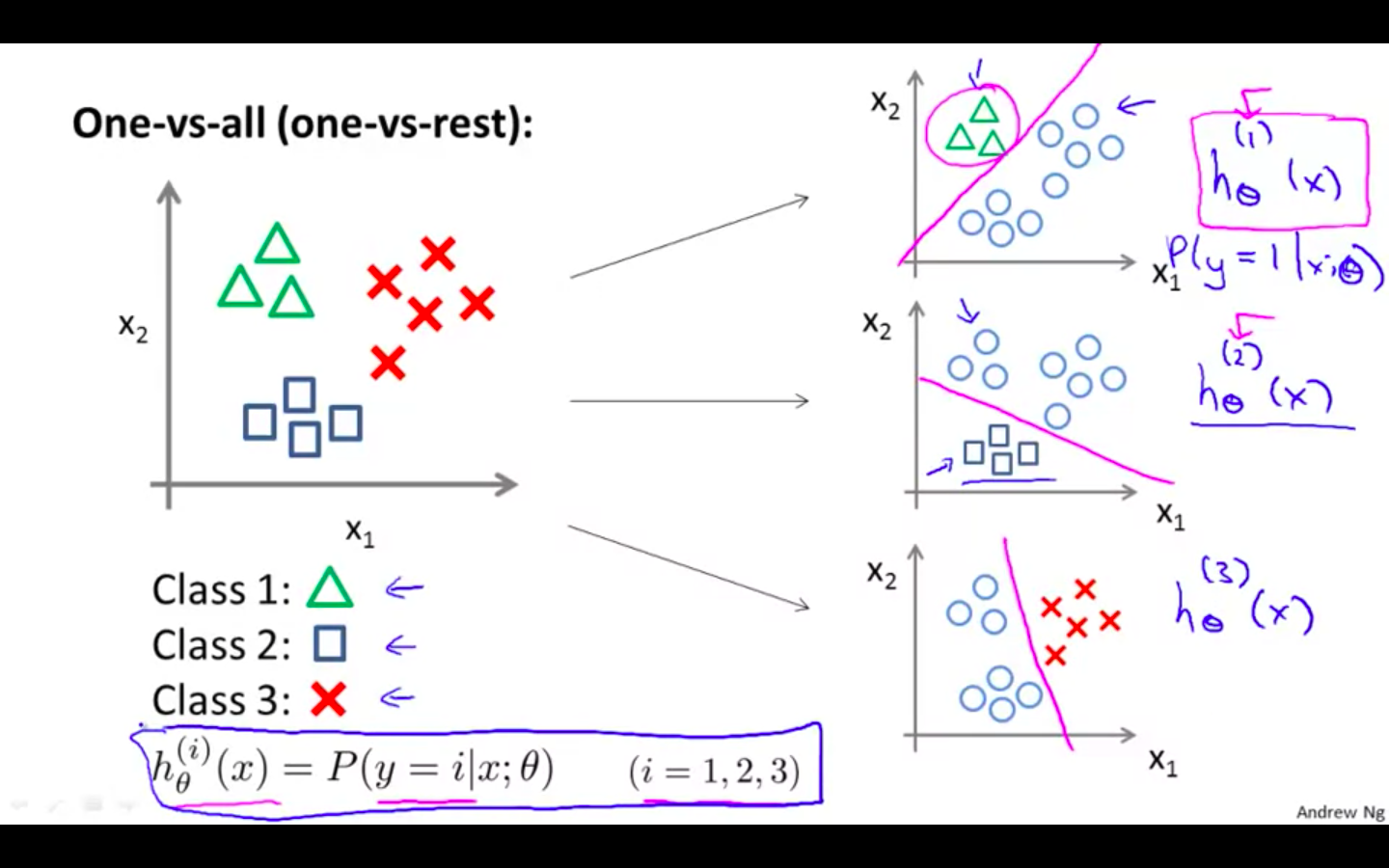

Multi-class Classification: One-vs-all

-

Instead of y = {0,1} we will expand our definition so that y = {0,1…n}.

-

Since y = {0,1…n}, we divide our problem into n+1 (+1 because the index starts at 0) binary classification problems; in each one, we predict the probability that ‘y’ is a member of one of our classes

-

Use Cases

-

Email sorting / tagging : Work, Family, Friends, Hobby

-

Medical diagrams: Not ill, Cold, Flu

-

Weather: Sunny, Cloud, Rain, Snow

-

-

Difference in data visualisation in binary classification and multi-class classification

-

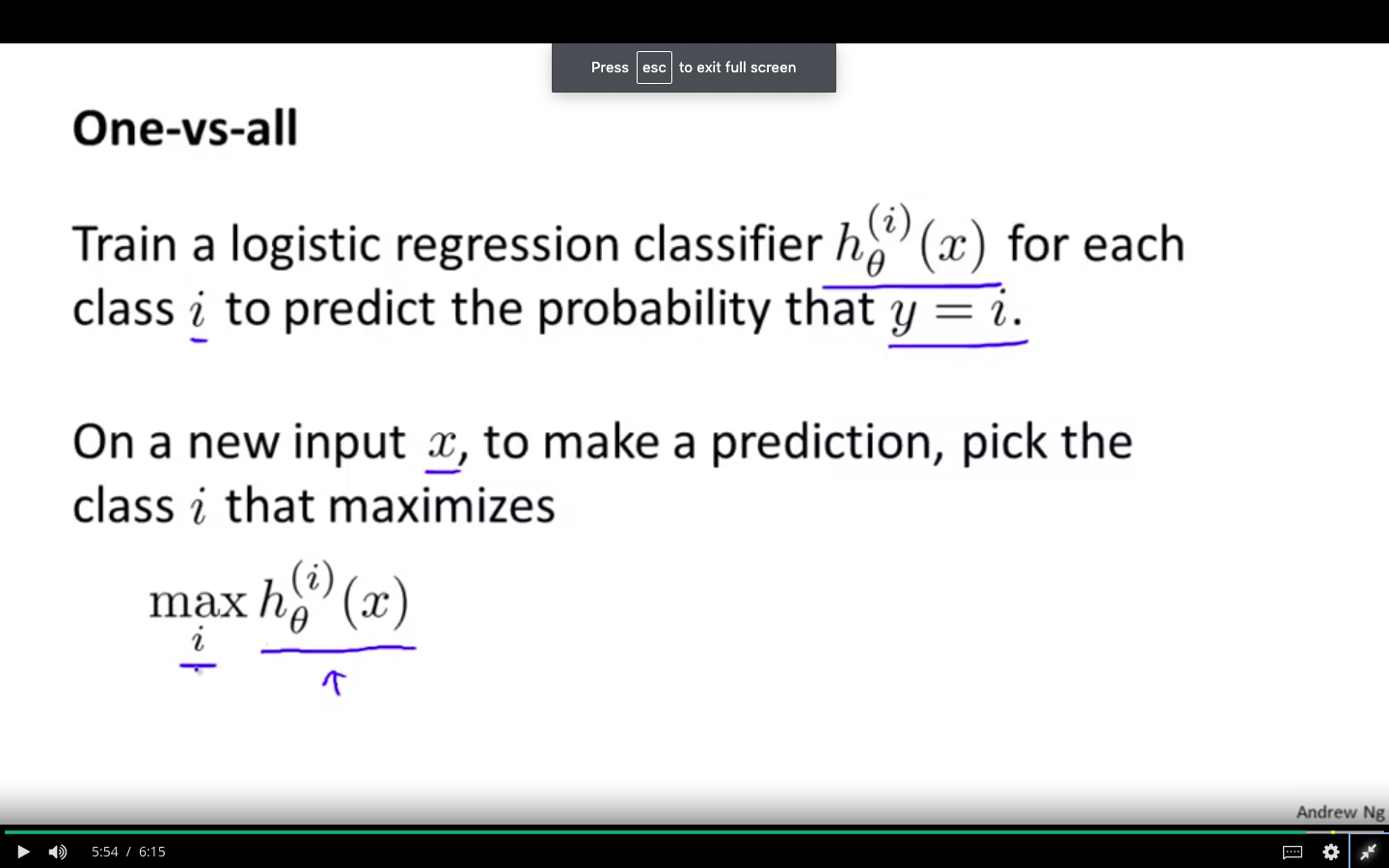

One vs All Algorithm

-

It chooses as first class and other classes as second class and does the Binary logistic regression among them.

-

It changes the active class and repeats until all the classes have been covered as the active class.

-

-

Using the algorithm

- Select the i for which the hypothesis is the maximum as the prediction

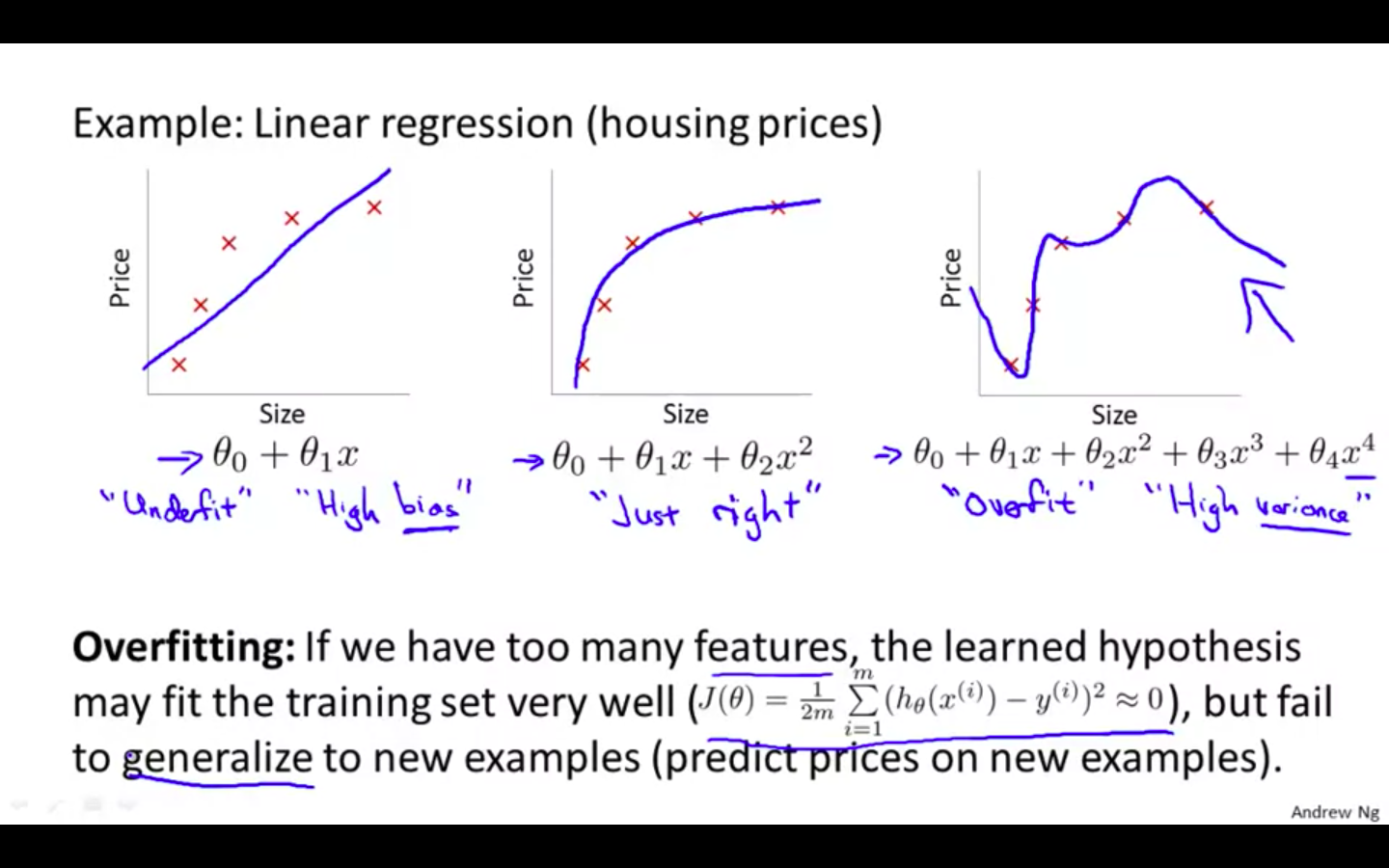

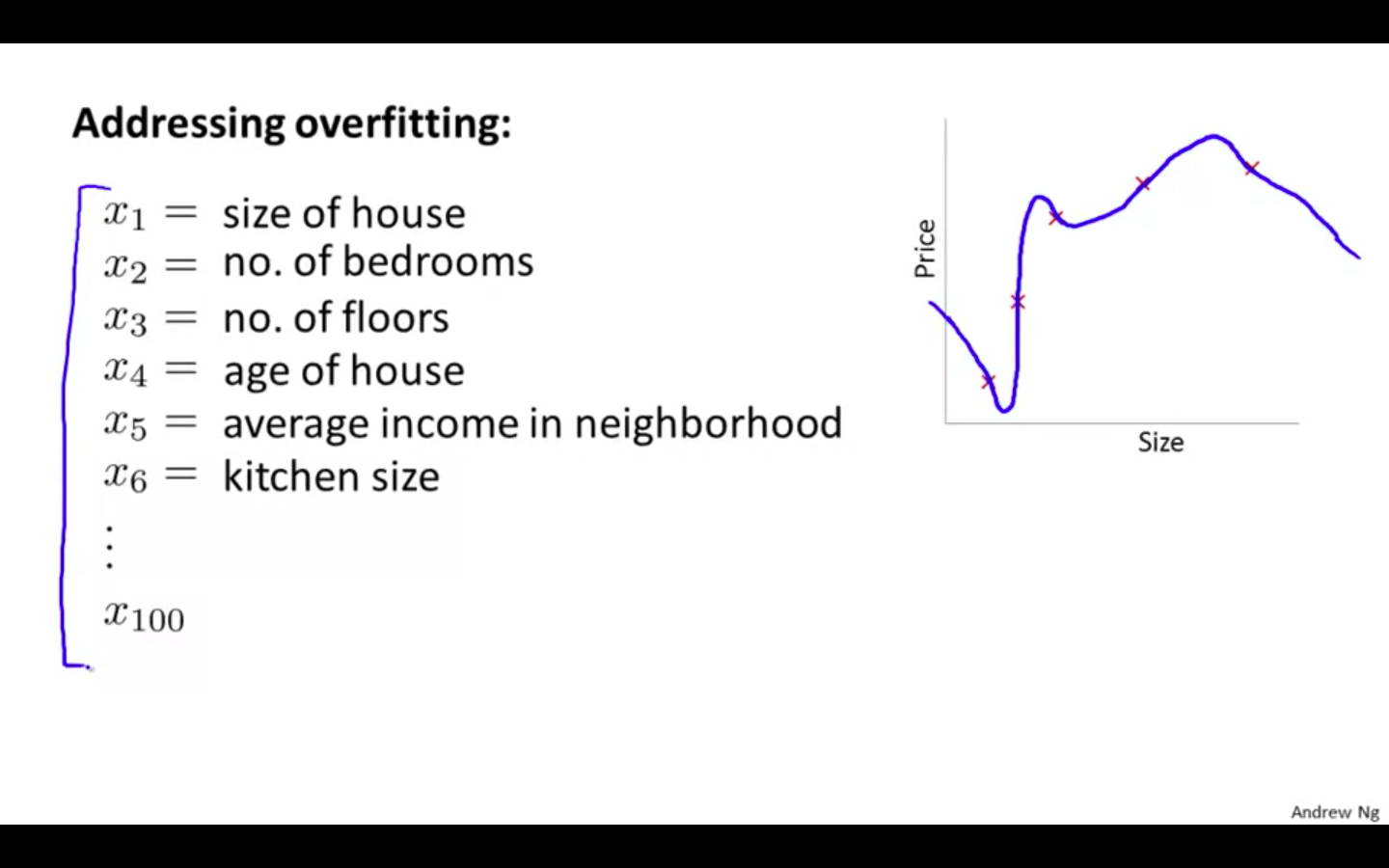

Solving the Problem of Overfitting

The Problem of Overfitting

-

If we have too many features, the learned hypothesis may fit the training set very well ( where cost function is similar to equal to 0 ), but fail to generalise to new examples ( predict prices on new examples )

-

Underfit or High bias

-

Underfitting, or high bias, is when the form of our hypothesis function h maps poorly to the trend of the data.

-

It is usually caused by a function that is too simple or uses too few features.

-

-

Overfit or High Variance

-

Overfitting, or high variance, is caused by a hypothesis function that fits the available data but does not generalize well to predict new data.

-

It is usually caused by a complicated function that creates a lot of unnecessary curves and angles unrelated to the data.

-

-

Overfitting in Linear Regression

-

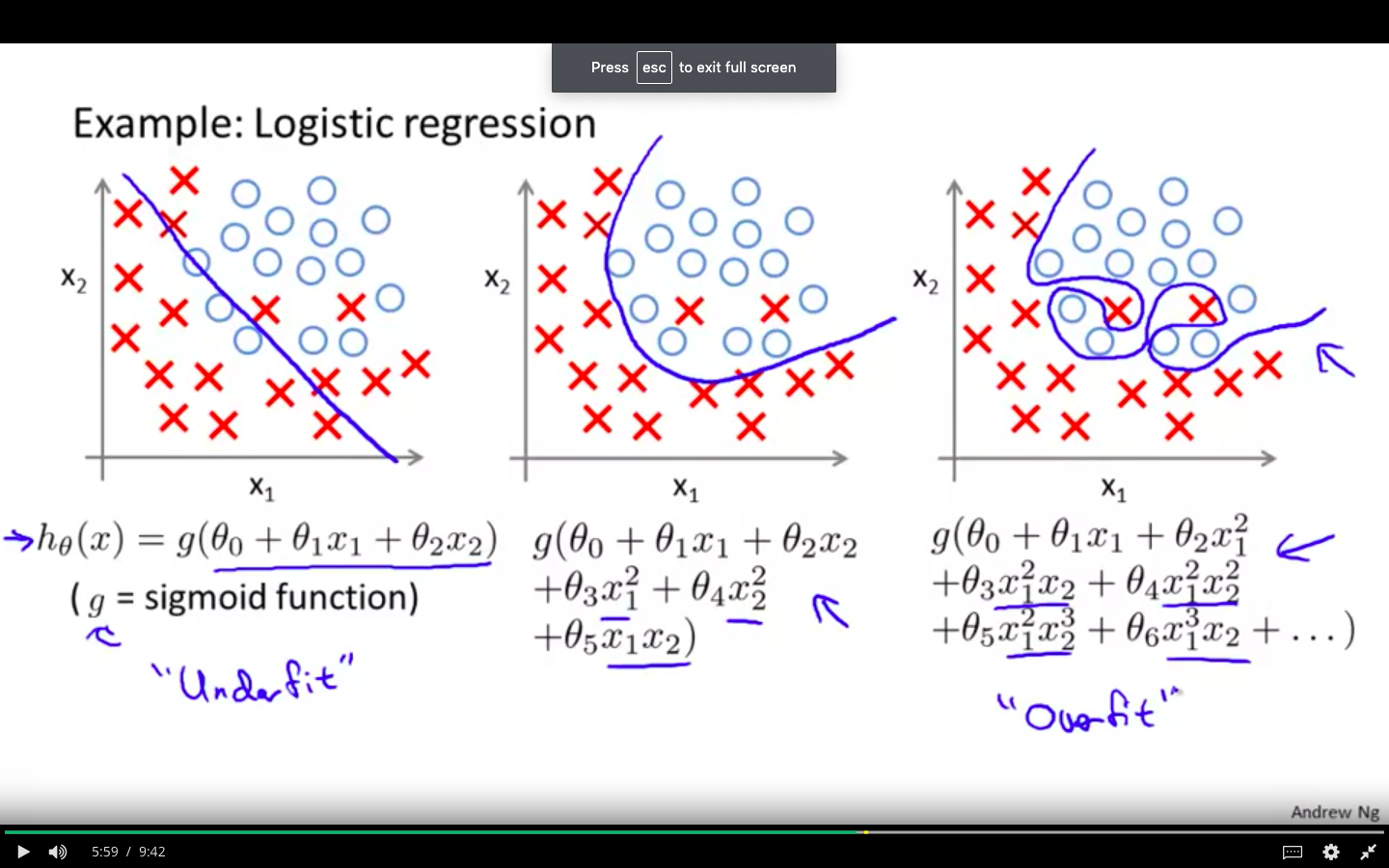

Overfitting in Logistic Regression

-

Causes of Overfitting

- Too many features & Small dataset

-

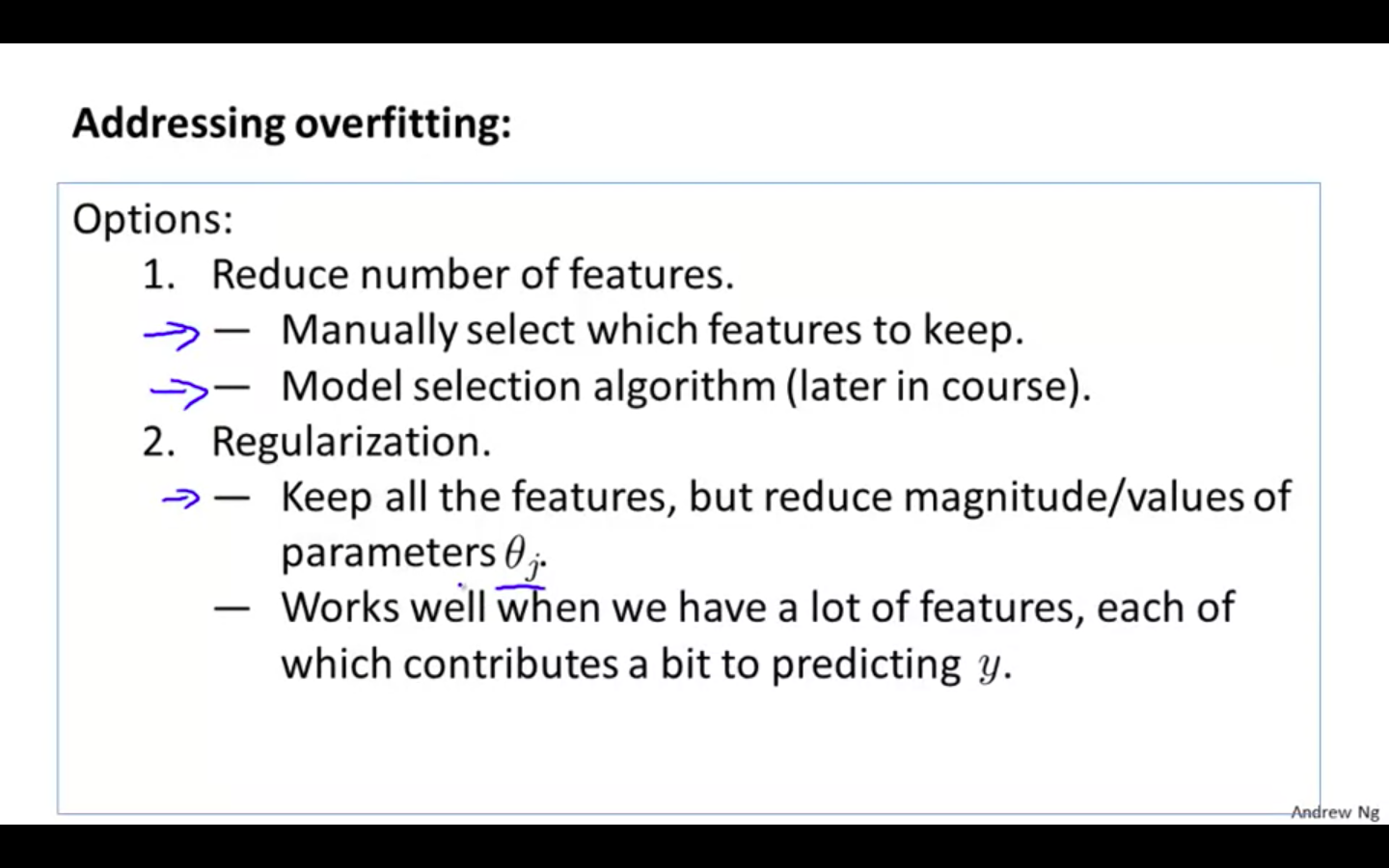

Solution to Overfitting

-

Reduce number of features

-

Manually select which features to keep

-

Model selection algorithm

-

-

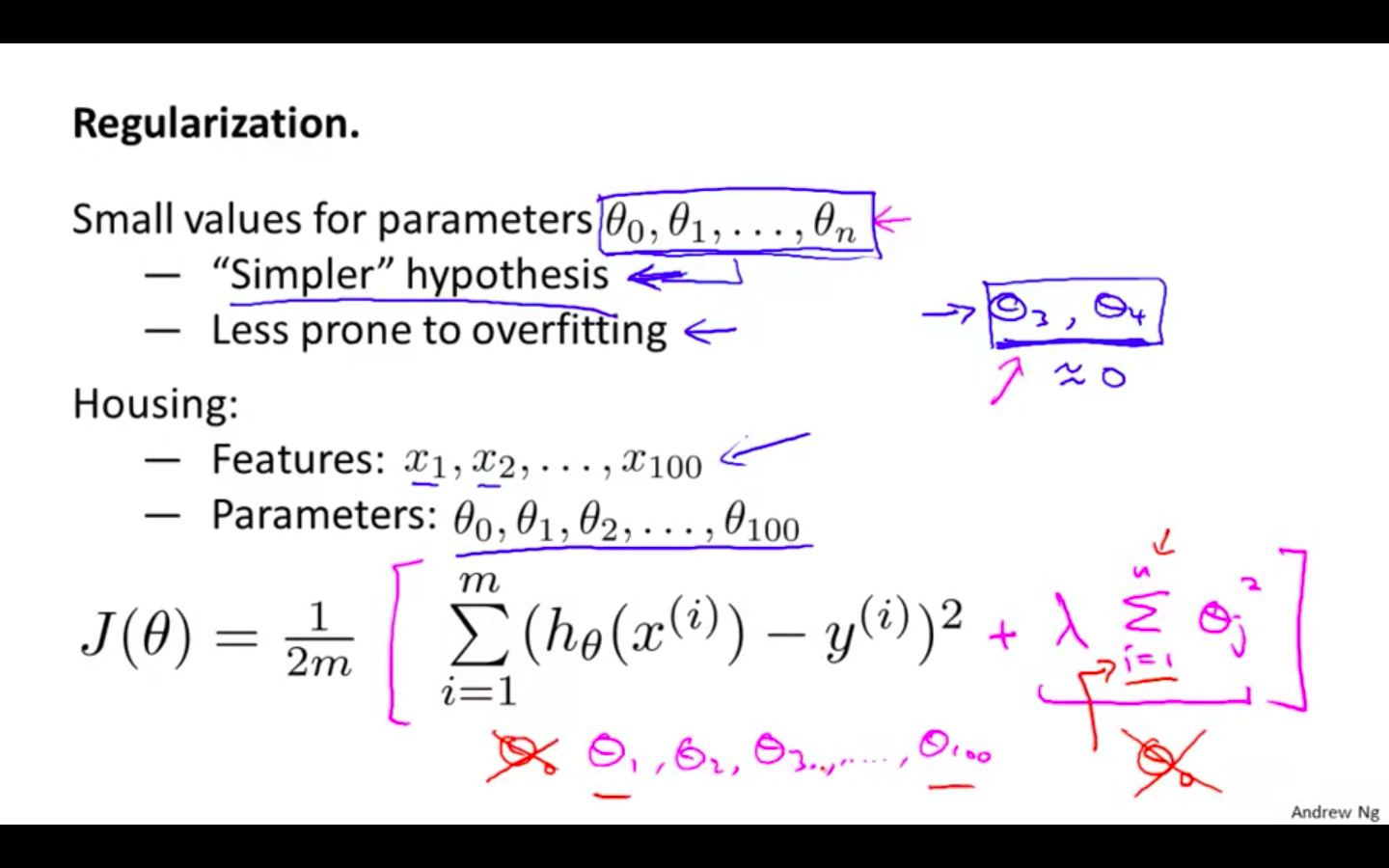

Regularisation

-

Keep all the features, but reduce magnitude / values of parameters

-

Works well when we have a lot of features, each of which contributes a bit to predicting y.

-

-

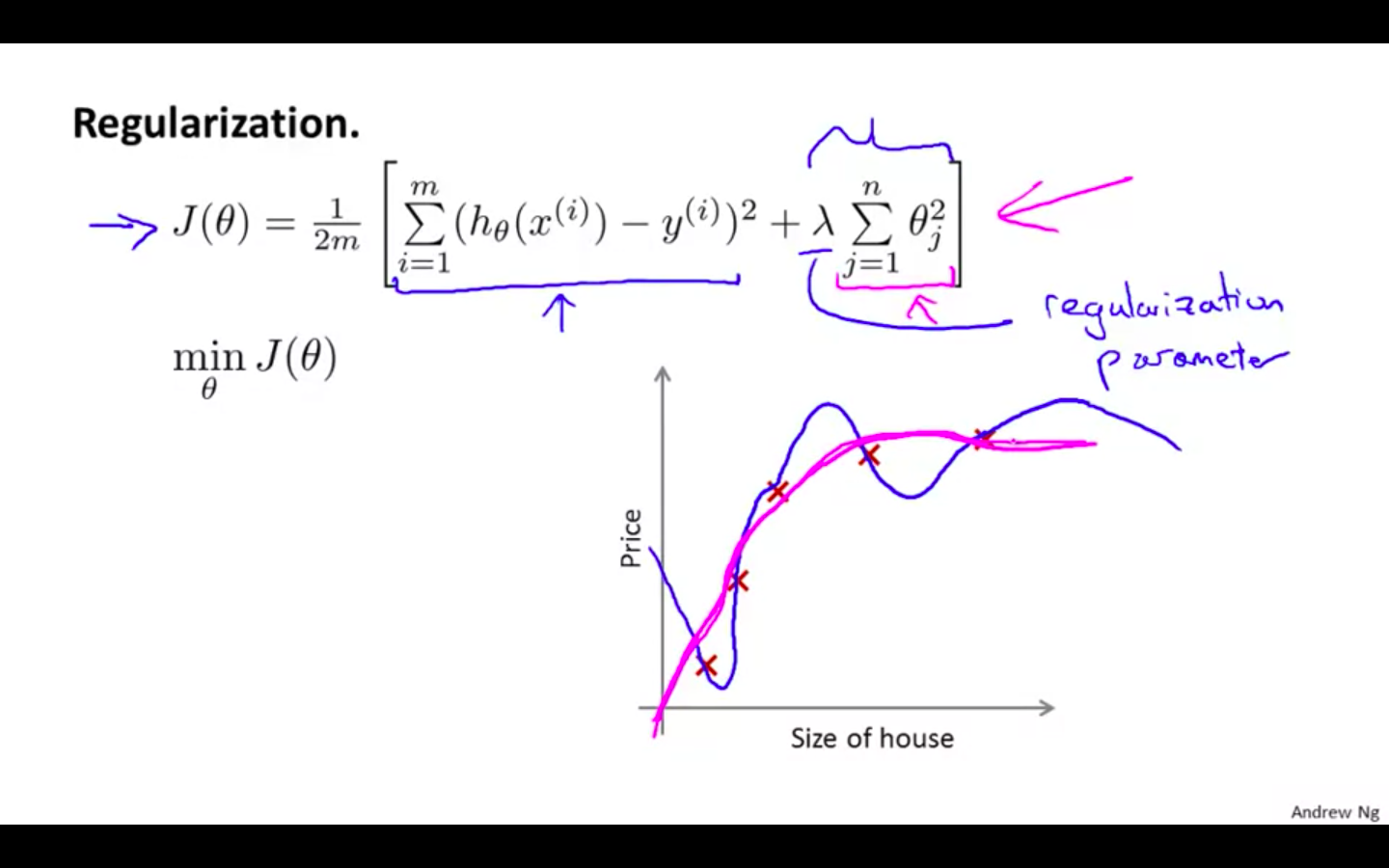

Cost Function

-

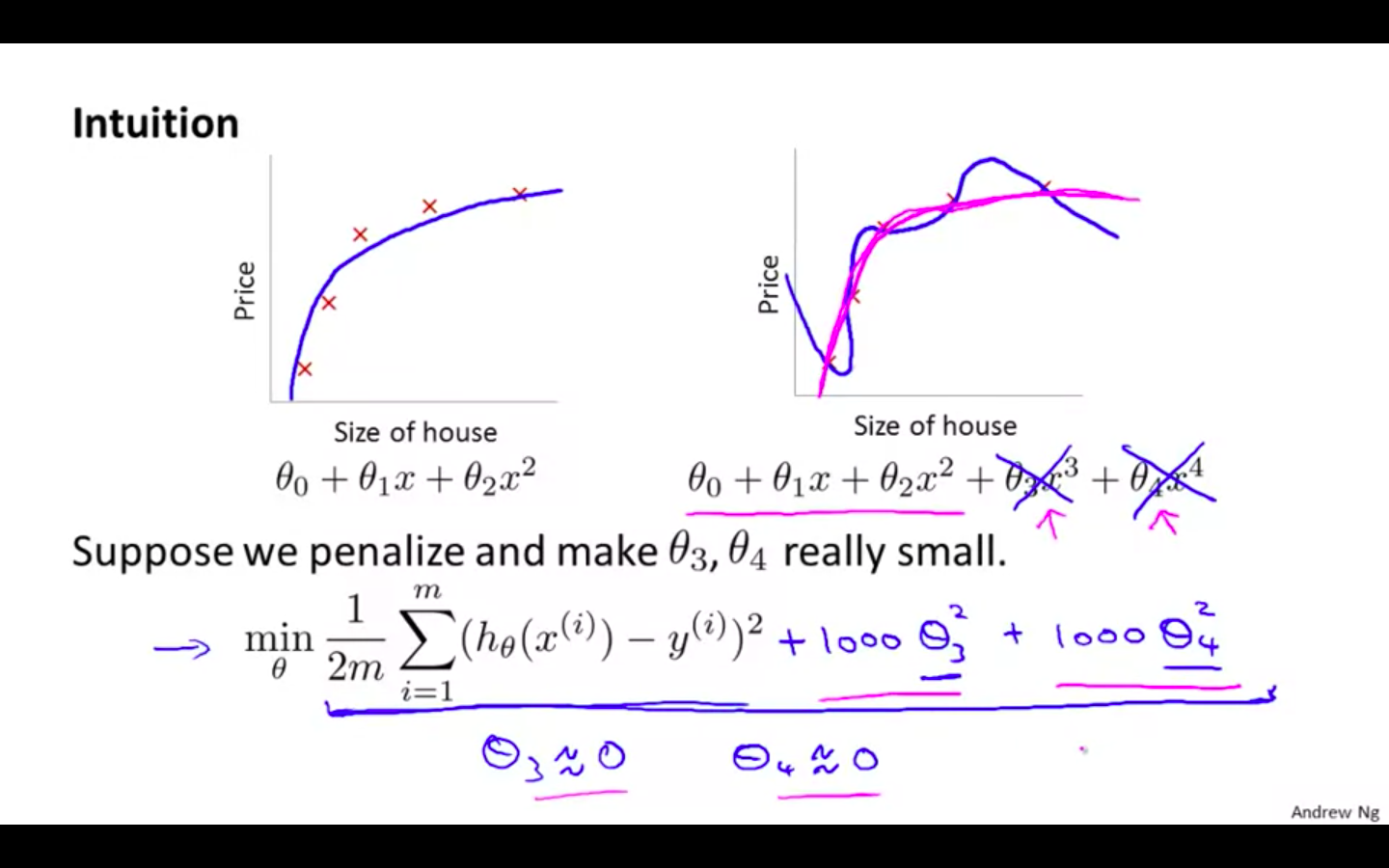

Intuition

-

If we have overfitting from our hypothesis function, we can reduce the weight that some of the terms in our function carry by increasing their cost.

-

Without actually getting rid of these features or changing the form of our hypothesis, we can instead modify our cost function:

-

If we reduce the features to near zero, will result in slight change in hypothesis

-

New hypothesis will fits the data better due to extra small terms

-

-

Regularisation

-

The λ, or lambda, is the regularization parameter.

-

It determines how much the costs of our theta parameters are inflated.

-

-

Example

-

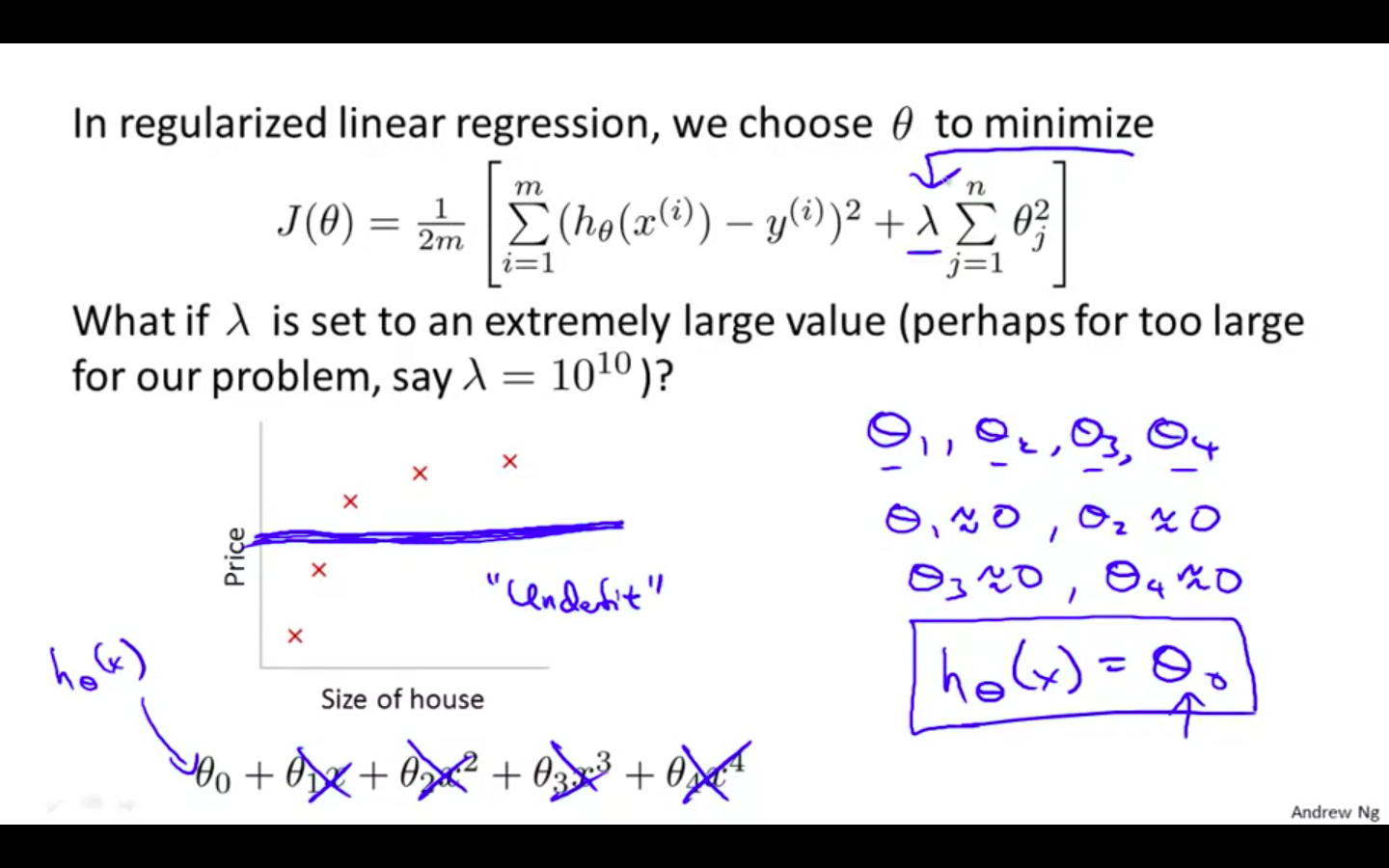

Regularisation Parameter

- If lambda is chosen to be too large, it may smooth out the function too much and cause underfitting.

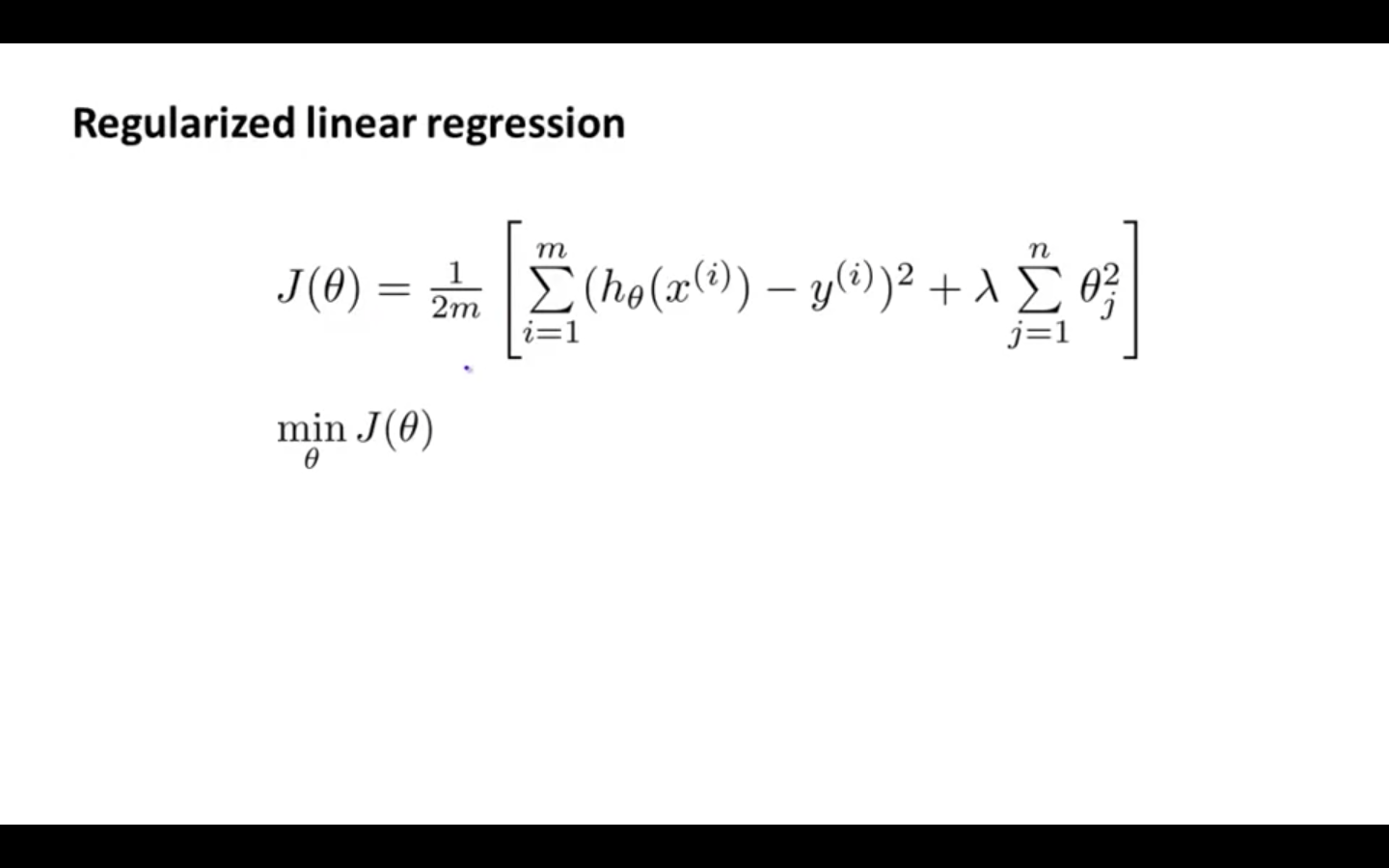

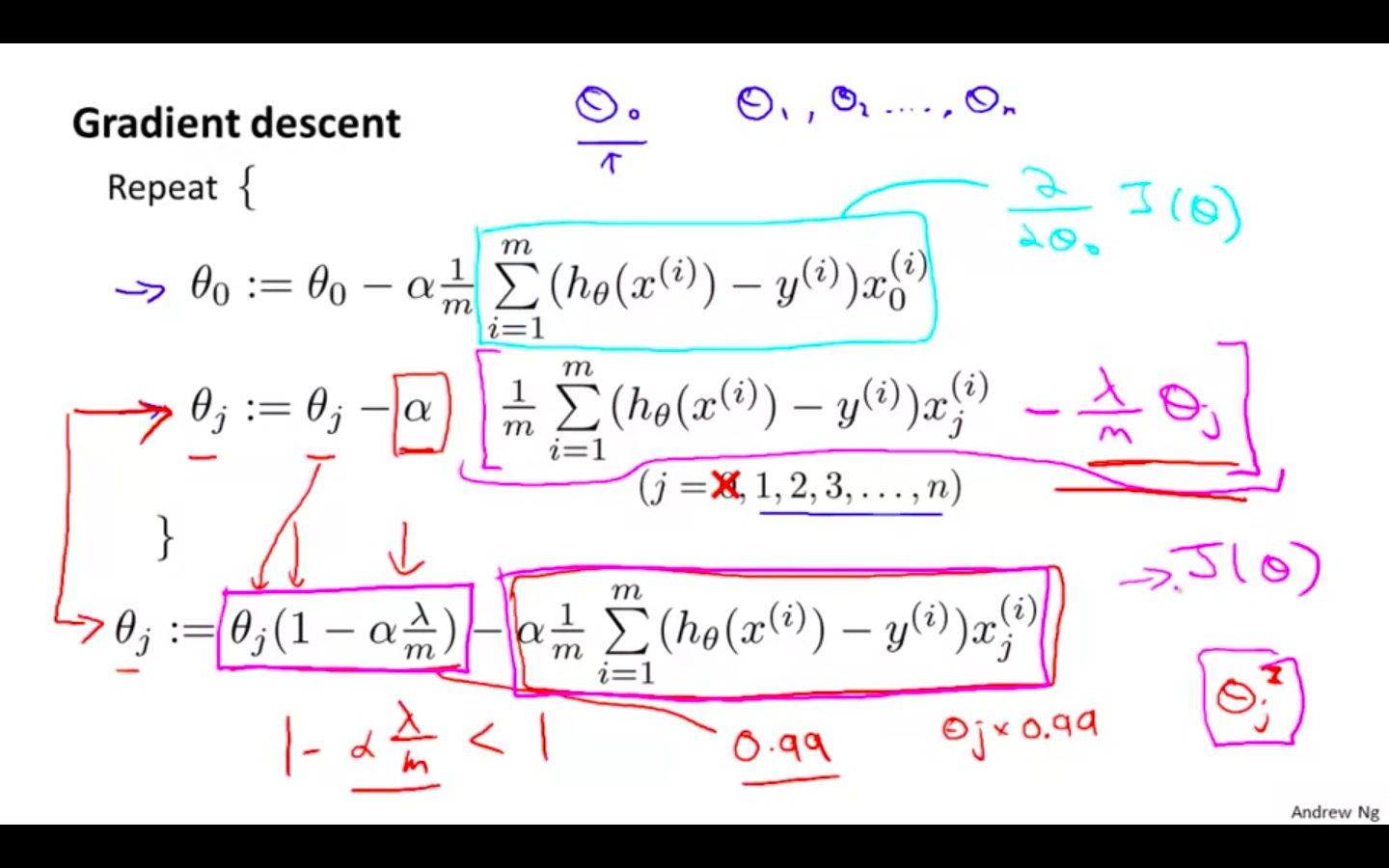

Regularised Linear Regression

-

Regularised Linear Regression

-

Regularised Gradient Descent

-

We will modify our gradient descent function to separate out theta_0 from the rest of the parameters because we do not want to penalise theta_0

-

Intuitively you can see it as reducing the value of theta_j by some amount on every update.

-

Notice that the second term is now exactly the same as it was before.

-

theta_0 is not regularised

-

-

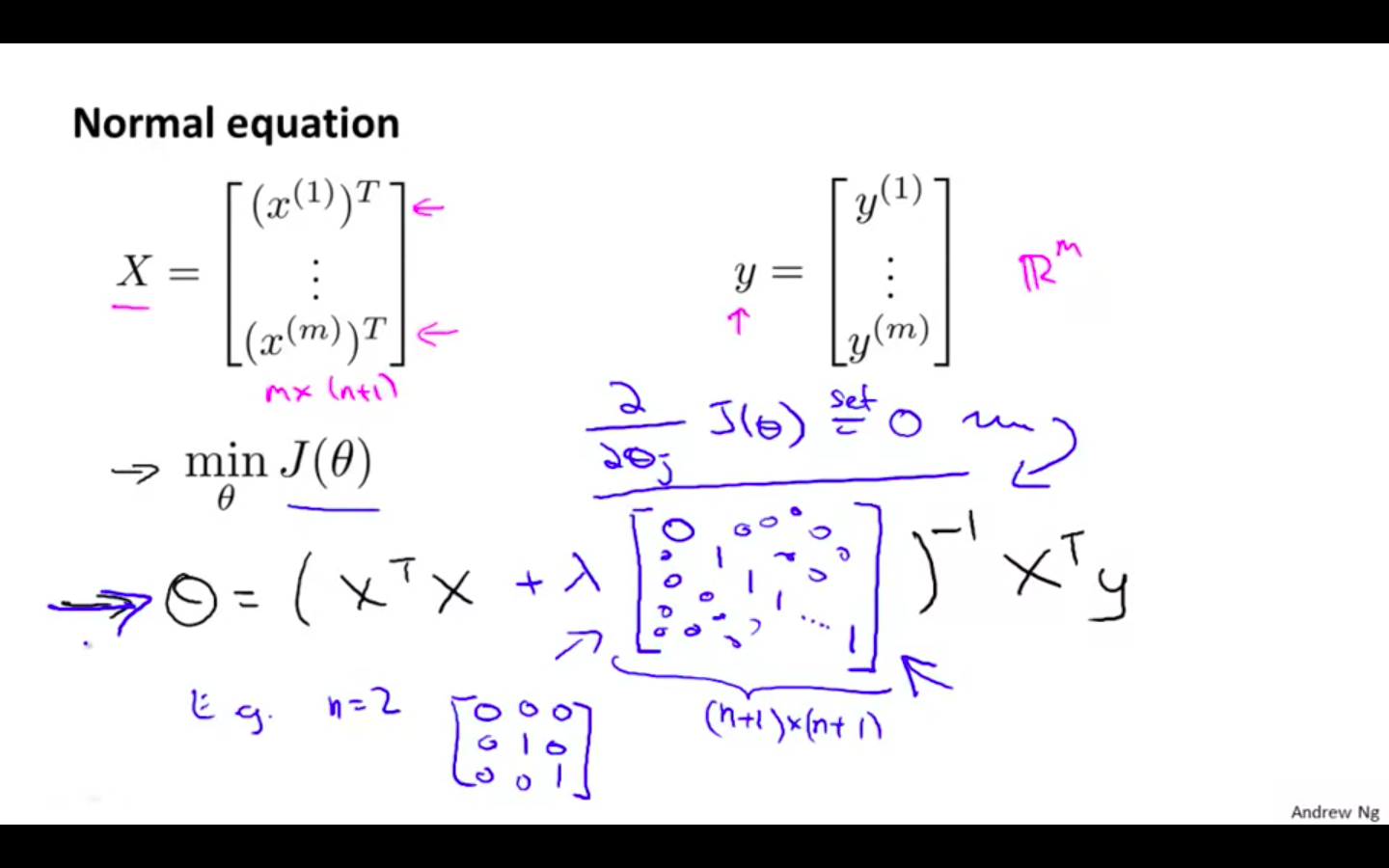

Regularised Normal Equation

- To add in regularisation, the equation is the same as our original, except that we add another term inside the parentheses:

-

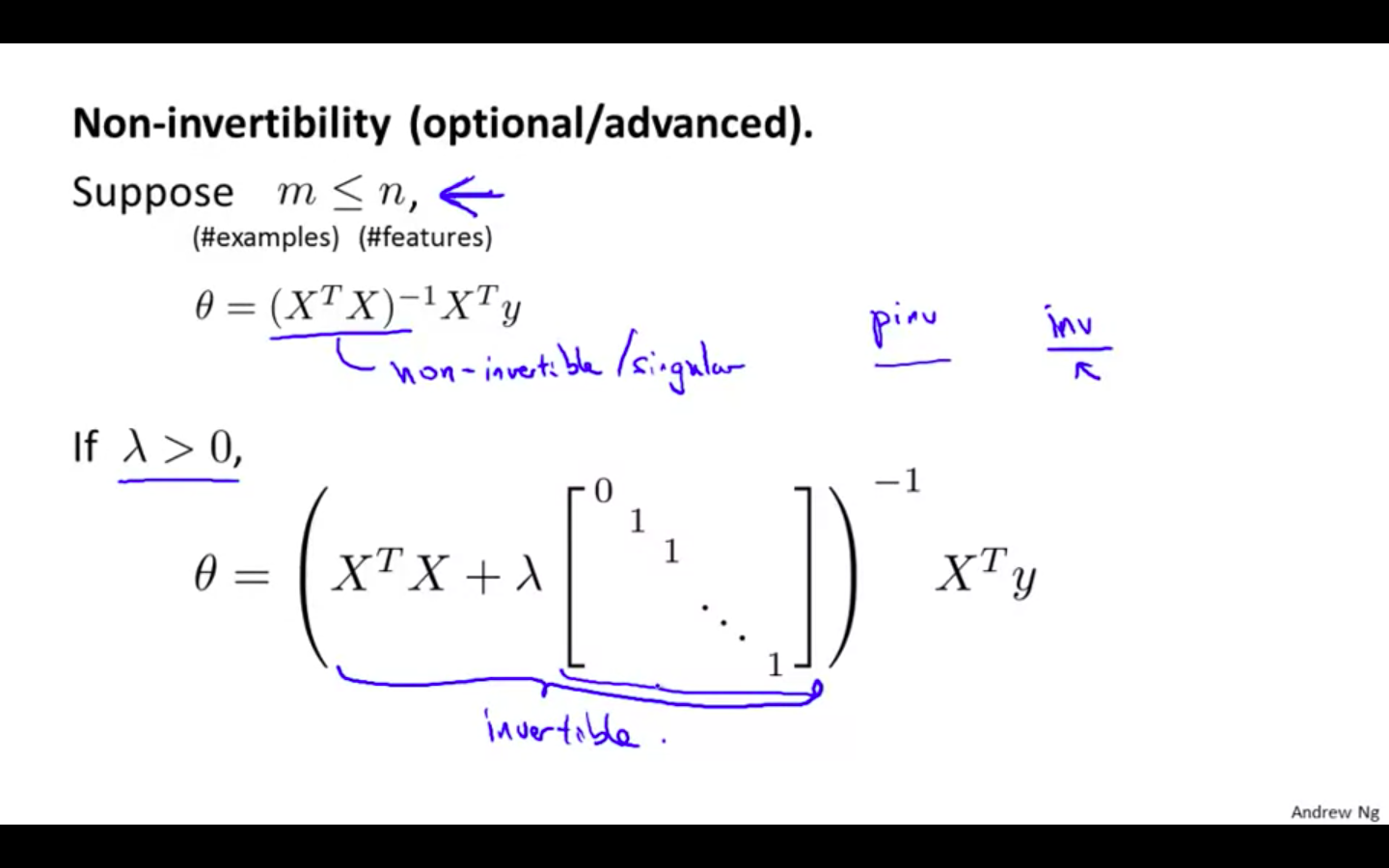

Regularisation in Non-Invertibility

- Recall that if m < n, then X^T _ X is non-invertible. However, when we add the term λ⋅L, then X^T _ X + λ⋅L becomes invertible.

- Recall that if m < n, then X^T _ X is non-invertible. However, when we add the term λ⋅L, then X^T _ X + λ⋅L becomes invertible.

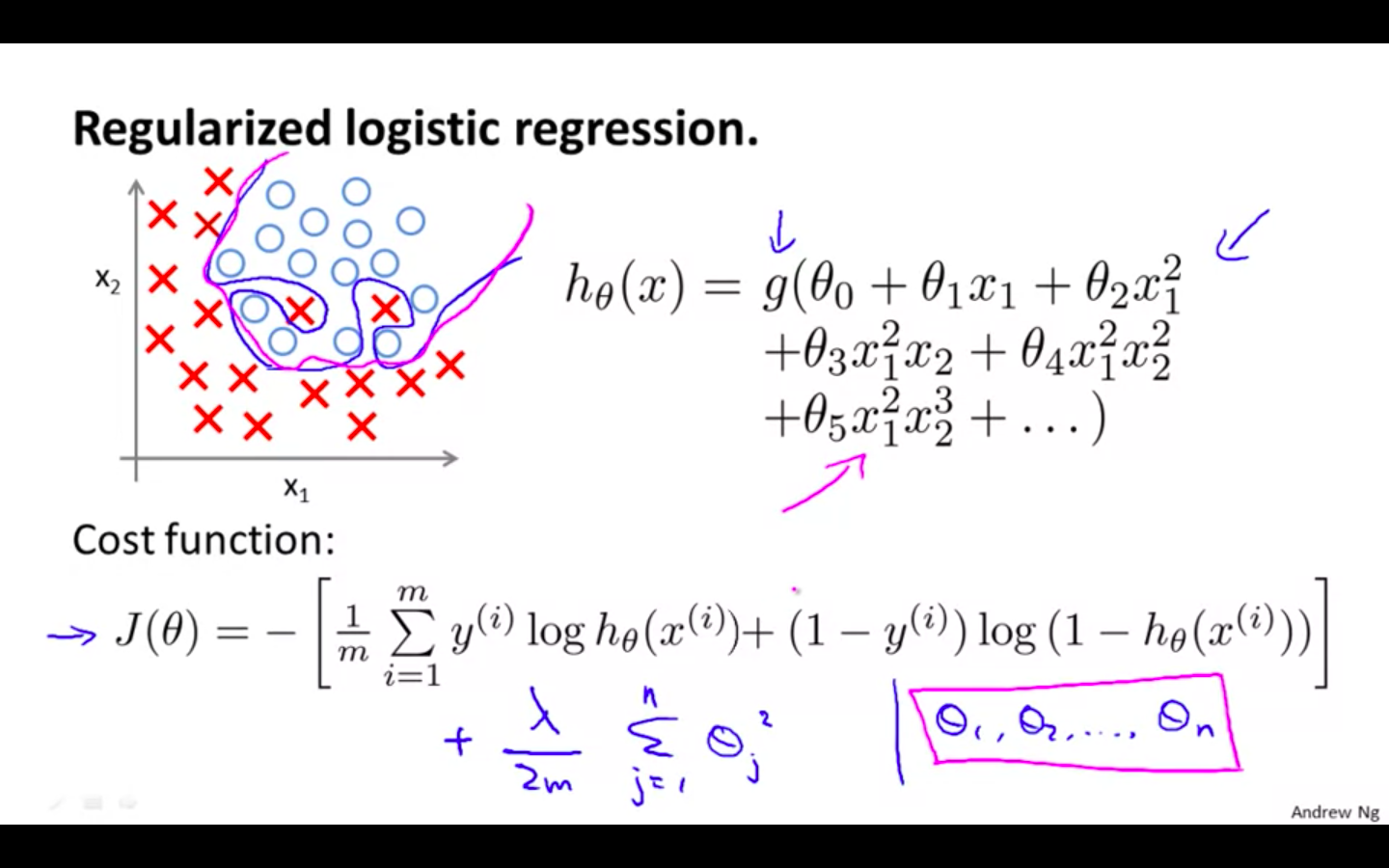

Regularised Logistic Regression

-

Regularised Logistic Regression

-

image shows how the regularised function, displayed by the pink line, is less likely to overfit than the non-regularised function represented by the blue line:

-

We can regularise this equation by adding a term to the end

-

-

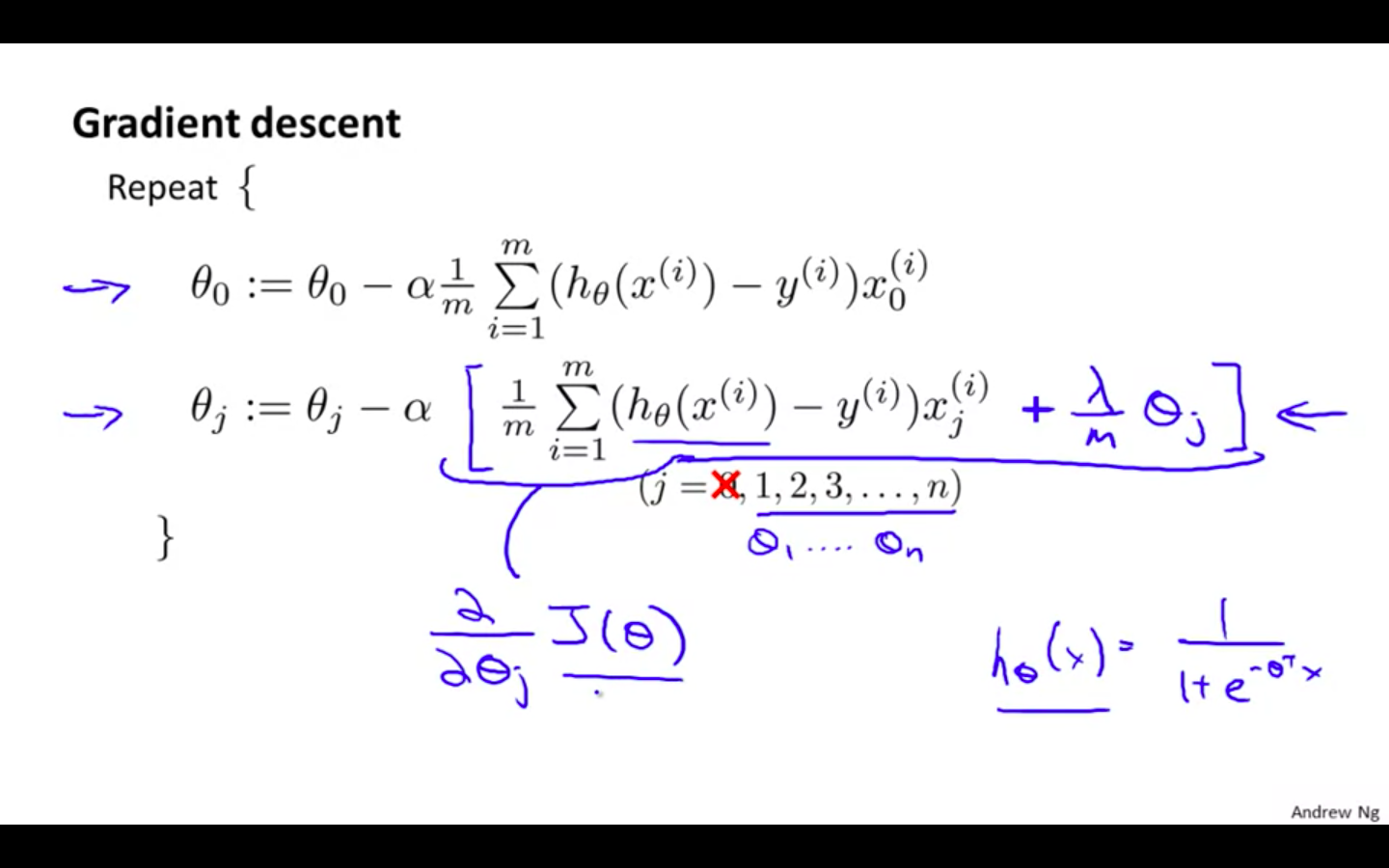

Regularised Gradient Descent

-

Equation seems identical with regularised gradient descent of linear regression

- Hypothesis is different in both regression

-

theta_0 is not regularised

-

computing the equation, we should continuously update the two following equations:

-

-

Regularised Advanced Optimisation